Reports

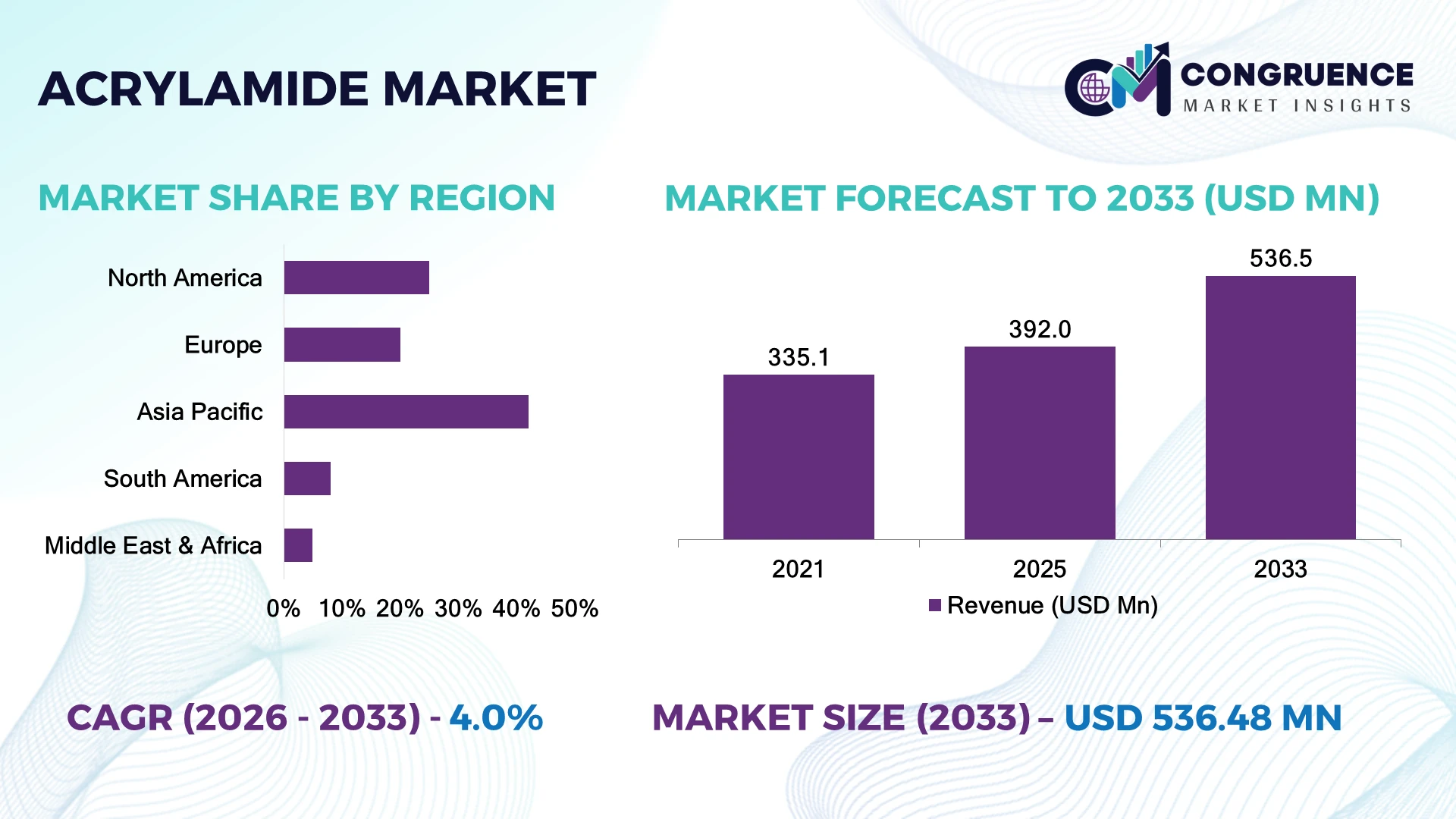

The Global Arcylamide Market was valued at USD 392.0 Million in 2025 and is anticipated to reach a value of USD 536.5 Million by 2033 expanding at a CAGR of 4.0% between 2026 and 2033. Rising wastewater treatment investments and expanding polyacrylamide consumption across mining, paper, and municipal infrastructure continue to accelerate market expansion.

China remains the dominant country, accounting for nearly 38% of global production capacity, supported by large-scale chemical manufacturing clusters and sustained industrial investments exceeding 12% in recent capacity upgrades. Compared with the United States, China benefits from broader integration across paper, mining, and water treatment industries, while over 70% of major wastewater facilities utilize acrylamide-derived flocculants, reinforcing its leadership amid evolving industrial and environmental policies.

Companies strengthening regional manufacturing footprints and application-specific product portfolios are expected to secure stronger long-term competitive positioning.

Market Size & Growth: USD 392.0 Million in 2025, projected to reach USD 536.5 Million by 2033 at 4.0% CAGR, driven by expanding advanced wastewater treatment infrastructure.

Top Growth Drivers: Water treatment demand (+35%), mining chemical consumption (+22%), paper processing modernization (+18%).

Short-Term Forecast: By 2028, process efficiency is expected to improve by nearly 15% through production optimization and digital plant monitoring.

Emerging Technologies: AI-enabled process control, automated continuous polymerization, and advanced catalyst technologies improve manufacturing consistency.

Regional Leaders: Asia Pacific (~USD 220 Million), North America (~USD 88 Million), Europe (~USD 74 Million), supported by industrial modernization and regional capacity expansion.

Consumer/End-User Trends: More than 70% of municipal water treatment facilities rely on high-performance polymer flocculants for operational efficiency.

Pilot/Case Example: In 2024, advanced digital chemical dosing systems reduced treatment chemical consumption by approximately 12% at industrial facilities.

Competitive Landscape: Top manufacturers collectively control about 45% of global supply, led by SNF Group, BASF, Kemira, Solenis, and Mitsubishi Chemical.

Regulatory & ESG Impact: Industrial discharge regulations have increased demand for efficient treatment chemicals by approximately 20% across major manufacturing economies.

Investment & Funding: More than USD 500 Million has been directed toward production expansion, strategic partnerships, and sustainable manufacturing upgrades.

Arcylamide remains essential across municipal water treatment, mining, oil recovery, and paper manufacturing as operators prioritize higher process efficiency and tighter environmental compliance. Automated polymer production technologies improve product consistency while reducing manufacturing variability by nearly 15%. Ongoing industrial supply-chain diversification across Asia and regional regulatory tightening continue encouraging localized production and advanced formulation development, setting the stage for broader strategic market evolution.

The Arcylamide Market is becoming increasingly strategic as governments and industries prioritize resilient water infrastructure, efficient mineral processing, and sustainable industrial operations. Growing environmental regulations and supply-chain restructuring are encouraging manufacturers to diversify production locations while strengthening regional raw material sourcing. This shift is enhancing supply security and improving responsiveness to rapidly changing industrial demand.

Modern automated polymerization systems deliver approximately 12% lower energy consumption and around 18% higher production consistency than conventional batch manufacturing, providing measurable operational advantages. Asia Pacific continues to lead large-scale production and downstream consumption, while North America emphasizes specialty formulations, process innovation, and regulatory compliance. Over the next two to three years, digital monitoring systems are expected to be integrated into more than 30% of newly upgraded production facilities.

Leading producers are expanding manufacturing capacity, establishing regional partnerships, and investing in advanced application laboratories to support customized industrial solutions. For example, integrated production sites serving municipal water treatment operations enable faster product qualification and improved logistics performance. Organizations combining manufacturing efficiency, regulatory readiness, and application-specific innovation will establish stronger competitive positioning and long-term operational resilience in the evolving global Arcylamide Market.

Growing environmental compliance requirements and industrial water reuse programs are accelerating acrylamide-based polyacrylamide adoption across municipal and industrial applications. China, India, and the United States are expanding wastewater infrastructure, with industrial water treatment demand contributing more than 30% of acrylamide derivative consumption. Mining operations using enhanced separation technologies have increased polymer utilization by nearly 20% in recent years. Regulatory tightening on industrial discharge standards is pushing companies to invest in high-performance flocculant formulations, automated dosing systems, and localized production facilities to improve treatment efficiency and secure supply continuity.

Acrylamide production remains affected by fluctuations in raw material availability, particularly acrylonitrile supply constraints and energy-intensive manufacturing requirements. Feedstock price variations of approximately 10–15% create margin pressure for producers, while strict chemical safety regulations increase compliance costs across manufacturing facilities. European producers face additional operational challenges due to tighter chemical handling requirements and sustainability standards. Companies are reducing exposure through long-term supply agreements, diversified sourcing strategies, and process optimization investments. The key operational challenge is maintaining cost competitiveness while meeting increasingly stringent safety and environmental compliance obligations.

Opportunities are expanding through advanced polyacrylamide formulations, digital chemical management systems, and increasing adoption in emerging industrial applications. India’s wastewater infrastructure modernization programs and mining sector expansion are creating new demand channels, with industrial polymer applications growing by more than 15% in targeted sectors. Manufacturers are developing low-residual acrylamide solutions and customized polymer grades to address stricter environmental requirements. Automation-driven dosing technologies are improving chemical efficiency by nearly 20% in treatment operations. Companies investing in application laboratories, regional production hubs, and strategic partnerships are positioned to capture specialized demand beyond traditional water treatment markets.

Scaling acrylamide production while maintaining safety, quality consistency, and environmental performance remains a critical industry challenge. Manufacturing facilities require advanced process controls due to acrylamide’s toxicity profile, with compliance monitoring increasing operational complexity by nearly 20% in regulated markets. Countries such as Germany and Japan are enforcing stricter chemical management frameworks, requiring producers to upgrade containment and monitoring systems. Limited availability of skilled chemical process specialists also affects expansion timelines. Companies must prioritize cleaner production technologies, workforce development, and advanced automation systems to maintain competitive positioning while ensuring reliable long-term supply and sustainable manufacturing practices.

Digital Process Optimization Chemical producers are accelerating digital transformation in acrylamide manufacturing through automated monitoring, predictive analytics, and process-control systems. Adoption of industrial automation has increased by nearly 25% across large chemical facilities, improving batch consistency and reducing operational downtime by approximately 15%. Companies in China and Japan are integrating smart manufacturing platforms to optimize polymer quality, energy usage, and safety compliance while restructuring production workflows for higher reliability.

Low-Residual Formulation Shift Environmental compliance requirements are driving adoption of low-residual acrylamide formulations, particularly for water treatment and industrial processing applications. Regulatory pressure has increased formulation upgrades by nearly 20% among major suppliers, while demand for safer polymer grades has expanded by over 12% in developed markets. Companies are investing in research partnerships and advanced purification technologies to improve product safety and strengthen customer retention.

Localized Supply Networks Supply-chain restructuring is encouraging producers to develop regional manufacturing and distribution networks to reduce dependency on imported chemical intermediates. Around 30% of major chemical companies have expanded local sourcing strategies since recent logistics disruptions, improving delivery reliability by nearly 18%. Manufacturers are establishing partnerships with domestic suppliers and increasing inventory planning capabilities to manage raw material uncertainty.

Sustainable Production Practices Chemical manufacturers are adopting energy-efficient production methods and waste-reduction initiatives as sustainability expectations increase. Several facilities have achieved approximately 10–15% reductions in energy intensity through improved reactor systems and resource management. Companies are prioritizing cleaner processing technologies and ESG-aligned investments to meet evolving industrial procurement standards and maintain competitiveness.

Polyacrylamide represents the leading type segment in the Arcylamide Market, accounting for approximately 78% of total demand due to its extensive use in wastewater treatment, mineral processing, and enhanced oil recovery applications. Its scalability, high flocculation efficiency, and compatibility with automated treatment systems make it the preferred solution for large industrial operators. Conventional acrylamide-based formulations maintain strong adoption, while specialty grades capture niche demand through improved performance and reduced environmental impact. Modified polyacrylamide variants are the fastest-growing type, expanding as industries seek customized solutions for complex water treatment and mining operations. Demand for advanced formulations has increased by nearly 18% as companies focus on higher efficiency and regulatory compliance. Producers are expanding specialty product portfolios, investing in application research, and developing region-specific formulations to improve competitiveness.

Water treatment remains the dominant application segment, contributing approximately 55% of acrylamide demand due to rising municipal infrastructure upgrades and industrial wastewater management requirements. Mining, paper processing, and oil recovery applications continue supporting steady consumption, with companies deploying polymer-based separation technologies to improve operational efficiency. Growing environmental compliance requirements have strengthened demand for high-performance flocculants. Enhanced oil recovery is emerging as the fastest-growing application area, supported by increasing investments in mature oilfield optimization technologies. Adoption in specialized recovery operations has increased by nearly 15%, while advanced polymer injection systems improve resource extraction efficiency by approximately 10%. Companies are expanding technical partnerships and developing application-specific formulations to address changing industrial requirements.

Industrial end-users represent the leading segment, accounting for nearly 65% of acrylamide consumption due to extensive deployment across water treatment plants, mining operations, and manufacturing facilities. These users require consistent chemical performance, supply reliability, and scalable treatment solutions. Large enterprises are increasingly adopting automated dosing systems, improving operational control by approximately 20% while reducing chemical wastage. Municipal utilities are the fastest-growing end-user group as governments expand wastewater infrastructure and environmental compliance programs. Public-sector investment in treatment modernization has increased adoption rates by nearly 15%, creating new opportunities for specialized polymer suppliers. Companies are strengthening partnerships with utilities, expanding technical support networks, and customizing solutions for different infrastructure requirements.

Asia-Pacific accounted for the largest market share at 42% in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 5.2% between 2026 and 2033.

North America accounted for approximately 25% of the global Arcylamide Market in 2025, supported by advanced wastewater treatment infrastructure, mature oil recovery operations, and strong chemical manufacturing capabilities. The United States represents the majority of regional consumption, driven by municipal water management and industrial processing applications. Increasing adoption of automated polymer dosing systems has improved treatment efficiency by nearly 15% across large-scale facilities. Chemical producers are strengthening domestic supply chains through capacity optimization, strategic partnerships, and customized polymer solutions to meet evolving environmental requirements.

United States Market Outlook: The United States remains the leading country in North America due to extensive industrial water treatment networks and advanced chemical production capabilities. More than 70% of major wastewater facilities utilize polymer-based treatment solutions, supporting continued demand for acrylamide derivatives. Investments in infrastructure upgrades and stricter discharge regulations are encouraging suppliers to expand technical services and application-focused product development.

Europe accounted for nearly 20% of the global Arcylamide Market in 2025, supported by stringent water quality regulations, advanced industrial wastewater systems, and established chemical manufacturing infrastructure. Germany, France, and the United Kingdom represent major demand centers due to strong industrial processing and environmental compliance frameworks. Sustainability initiatives are accelerating adoption of optimized polymer formulations, with manufacturers improving production efficiency by approximately 10–15% through advanced processing technologies. European suppliers are prioritizing cleaner manufacturing, regional partnerships, and specialty formulations to address increasing safety and environmental requirements.

Germany Market Outlook: Germany is the most strategically significant European market due to its strong chemical industry base, industrial automation capabilities, and strict environmental standards. The country contributes substantially to regional demand through manufacturing, wastewater treatment, and process industries. More than 60% of industrial facilities operate under advanced wastewater management frameworks, creating consistent demand for high-performance treatment chemicals.

Asia-Pacific dominated the Arcylamide Market with approximately 42% share in 2025, supported by large-scale chemical manufacturing, expanding wastewater infrastructure, and growing industrial activity. China, India, and Japan are key contributors, with China accounting for the highest production capacity due to integrated chemical supply chains. Regional producers are increasing investments in specialty polymer manufacturing, while industrial wastewater treatment adoption has expanded by more than 20% in developing economies. Companies are strengthening domestic production networks and improving application-specific formulations to support mining, paper, and municipal treatment demand.

China Market Outlook: China remains the largest country-level market due to extensive chemical production capacity and strong downstream industries. The country contributes nearly 38% of global acrylamide production capacity, supported by integrated manufacturing clusters and high demand from water treatment and industrial processing sectors. Government-led environmental modernization programs continue encouraging investment in advanced treatment technologies and efficient polymer solutions.

South America accounted for approximately 8% of the global Arcylamide Market in 2025, driven primarily by mining operations, industrial wastewater treatment, and resource-processing activities. Brazil and Chile represent key demand centers due to large mining industries and expanding environmental management requirements. Mining applications contribute nearly 40% of regional acrylamide derivative consumption, particularly for mineral separation and processing operations. Companies are improving regional distribution networks and forming partnerships with industrial operators to overcome logistics limitations and strengthen supply reliability.

Brazil Market Outlook: Brazil leads the South American market due to its large mining sector, industrial base, and growing wastewater infrastructure requirements. The country represents more than 45% of regional demand, supported by mineral processing operations and municipal treatment expansion. Increasing environmental monitoring requirements are encouraging industries to adopt more efficient polymer-based treatment solutions and improve operational performance.

Middle East & Africa accounted for nearly 5% of the global Arcylamide Market in 2025, supported by water scarcity management, oilfield operations, and industrial infrastructure development. Gulf countries are increasing investments in advanced water treatment systems and industrial process optimization, while African mining economies are expanding chemical usage for mineral processing applications. Desalination and wastewater reuse projects have increased polymer demand by approximately 15% in selected markets. Companies are developing localized supply partnerships and strengthening technical support networks to address infrastructure gaps and improve deployment efficiency.

Saudi Arabia Market Outlook: Saudi Arabia represents the most strategically important market in the region due to major investments in water infrastructure, oilfield optimization, and industrial diversification programs. The country operates one of the world’s largest desalination networks, supporting demand for advanced water treatment chemicals. Increasing industrial modernization initiatives are encouraging suppliers to establish partnerships and provide customized polymer solutions for large-scale applications.

The Arcylamide Market features competition between global chemical producers, specialty polymer suppliers, and regional manufacturers. Major players such as SNF Group, BASF, and Kemira compete with cost-focused Asian producers and application-specific suppliers through technology, capacity, and supply reliability. The top five companies collectively control approximately 45% of market supply, creating a moderately consolidated structure. Competition centers on formulation performance, pricing efficiency, customized polymer grades, and distribution strength, with premium suppliers achieving 15–20% higher customer retention through technical support. Companies are expanding production facilities, forming water-treatment partnerships, and integrating upstream raw material capabilities to secure supply chains. The market is shifting toward sustainable formulations and localized manufacturing due to regulatory pressure and logistics disruptions. High capital requirements, chemical expertise, and compliance standards create entry barriers. Winning players will combine scalable production, innovation capability, and application-focused solutions to outperform established suppliers.

BASF SE

Kemira Oyj

Solenis LLC

Mitsubishi Chemical Group Corporation

Anhui Jucheng Fine Chemicals Co., Ltd.

Beijing Hengju Chemical Group Corporation

Ashland Global Holdings Inc.

Ecolab Inc.

Gelita AG

Mitsui Chemicals, Inc.

Dia-Nitrix Co., Ltd.

Advanced polymerization technologies are transforming acrylamide production through automated reactors, digital monitoring, and precision process controls. Modern continuous polymerization systems improve production consistency by approximately 15% compared with traditional batch methods while reducing process variability. Adoption of industrial automation is expanding across major chemical facilities as manufacturers seek improved safety, quality control, and operational efficiency.

Emerging technologies include AI-enabled process optimization, low-residual acrylamide formulations, and energy-efficient manufacturing systems. Artificial intelligence-based monitoring improves predictive maintenance accuracy by nearly 20%, helping producers reduce downtime and optimize resource utilization. Companies investing in these solutions gain advantages through faster production cycles, improved compliance, and customized polymer development.

Between 2026 and 2028, sustainable production technologies and integrated digital platforms will become critical competitive differentiators. New-generation systems provide approximately 10–15% efficiency improvements over conventional operations, benefiting large chemical producers with scalable infrastructure. Technology leaders and vertically integrated suppliers are positioned to strengthen market influence as customers increasingly prioritize performance, reliability, and environmentally responsible chemical solutions.

July 2025Kemira announced a nearly EUR 20 million investment to expand its Tarragona, Spain facility with a new production line supporting advanced water treatment solutions. The expansion strengthens chemical supply capabilities and supports growing demand for high-performance treatment polymers and related solutions. Source: www.kemira.com

September 2025Kemira signed an agreement to acquire Water Engineering, Inc. in the United States for approximately USD 150 million, expanding industrial water treatment services. The move enhances application expertise, customer integration, and downstream solution capabilities across manufacturing and wastewater industries. Source: www.kemira.com

March 2025Kemira and IFF advanced a EUR 130 million joint venture focused on commercial-scale renewable biobased materials production. The partnership supports sustainable chemical innovation and strengthens future opportunities for bio-based alternatives within water treatment and industrial applications. Source: www.kemira.com

October 2025Solenis opened a 100,000-square-foot Global Research Center in Delaware, USA, featuring advanced laboratories and pilot-scale testing capabilities. The facility accelerates product development, customer collaboration, and innovation for water and process treatment applications.

The Arcylamide Market Report provides comprehensive coverage of market dynamics across types, applications, end-users, and major geographical markets. The analysis evaluates polyacrylamide variants, water treatment, mining, paper processing, oil recovery applications, and industrial end-user adoption patterns. It examines competitive positioning across established manufacturers, regional suppliers, and emerging technology-focused companies.

The report includes regional assessments covering Asia Pacific, North America, Europe, and developing industrial markets, along with insights into automation, sustainable formulations, and advanced production technologies. Covering strategic trends between 2026 and 2033, the report supports investment planning, expansion decisions, partnership evaluation, and competitive strategy development by identifying demand shifts, operational priorities, and future market opportunities.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 392.0 Million |

| Market Revenue (2033) | USD 536.5 Million |

| CAGR (2026–2033) | 4.0% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Companies Profiled | SNF Group; BASF SE; Kemira Oyj; Solenis LLC; Mitsubishi Chemical Group Corporation; Anhui Jucheng Fine Chemicals Co., Ltd.; Beijing Hengju Chemical Group Corporation; Ashland Global Holdings Inc.; Ecolab Inc.; Gelita AG; Mitsui Chemicals, Inc.; Dia-Nitrix Co., Ltd. |

| Customization & Pricing | Available on Request (10% Customization Free) |