Reports

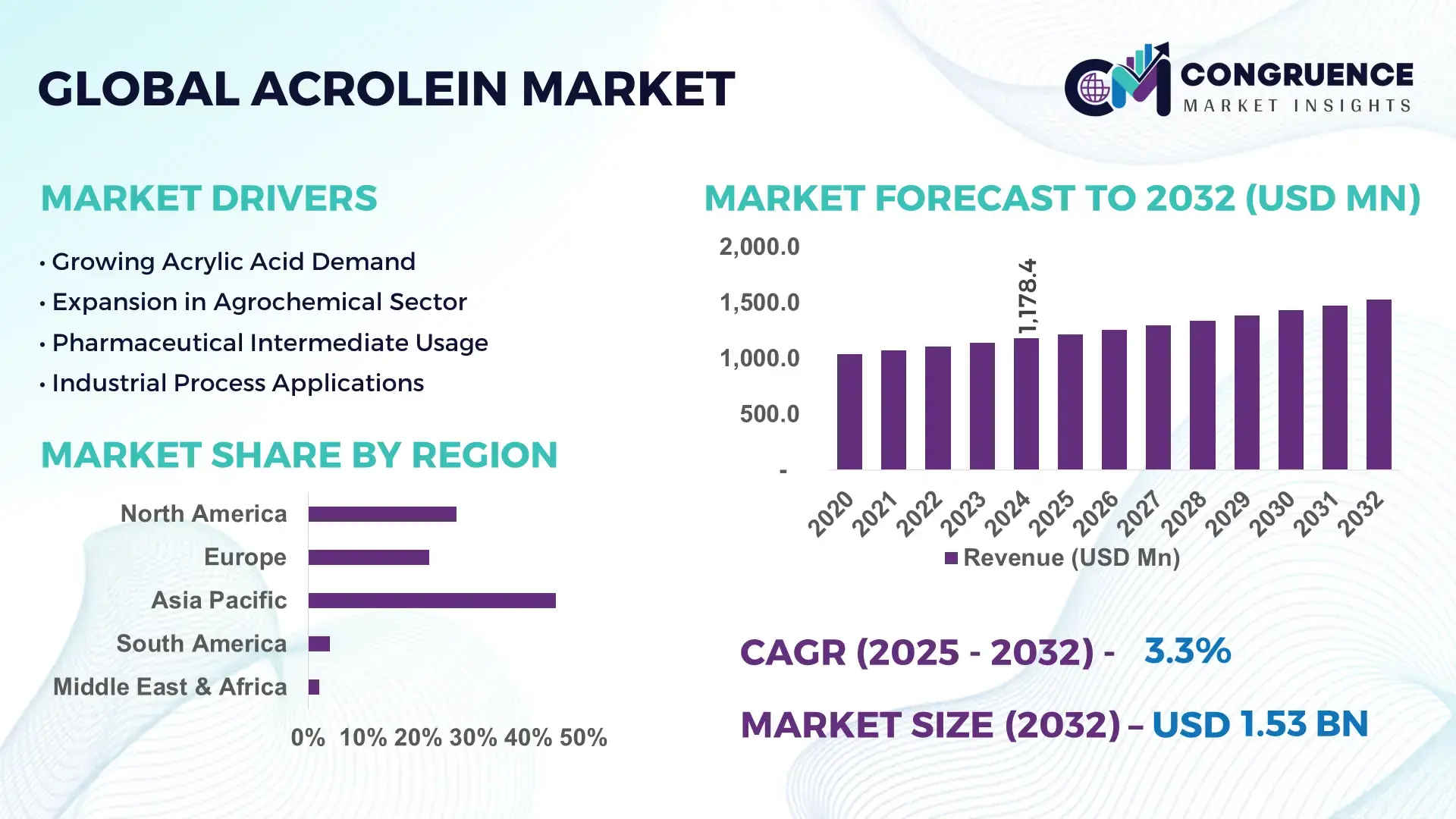

The Global Acrolein Market was valued at USD 1,178.4 Million in 2024 and is anticipated to reach a value of USD 1,525.5 Million by 2032 expanding at a CAGR of 3.28% between 2025 and 2032, according to an analysis by Congruence Market Insights. This growth is driven by increasing industrial applications and rising adoption in chemical intermediates.

China dominates the Acrolein market, leveraging advanced production capacity and large-scale investments exceeding USD 250 million annually in new chemical processing facilities. The country’s industrial infrastructure supports annual production volumes of over 120,000 tons. Key applications include acrylic acid synthesis, agricultural chemicals, and pharmaceutical intermediates. Technological advancements, such as catalytic oxidation and continuous-flow reactors, have improved yield efficiency by 18–20% in recent years. Regional adoption patterns show 65% of industrial users utilize automated monitoring systems for process optimization, demonstrating a strong integration of innovation with manufacturing operations.

Market Size & Growth: Global Acrolein valued at USD 1,178.4 Million in 2024, projected to reach USD 1,525.5 Million by 2032, driven by industrial and chemical intermediary demand.

Top Growth Drivers: Increased adoption in acrylic acid production (52%), efficiency improvement via catalytic oxidation (18%), rising agricultural chemicals utilization (40%).

Short-Term Forecast: By 2028, process optimization and automation expected to improve manufacturing efficiency by 15%.

Emerging Technologies: Continuous-flow reactors, advanced catalysts, and automated monitoring systems enhancing productivity.

Regional Leaders: China USD 525 M (2032) with high automation adoption; Europe USD 360 M (2032) emphasizing precision chemical processes; North America USD 310 M (2032) focusing on green manufacturing initiatives.

Consumer/End-User Trends: Pharmaceuticals, agrochemicals, and polymer intermediates showing higher adoption; 60% of large-scale producers now use AI-assisted process monitoring.

Pilot or Case Example: In 2025, a Chinese facility achieved 18% yield improvement through integrated catalytic oxidation and real-time monitoring.

Competitive Landscape: BASF (~15% share), Mitsubishi Gas (~12%), Arkema (~10%), Evonik (~8%), and Lanxess (~7%).

Regulatory & ESG Impact: Compliance with VOC emission limits and implementation of chemical recycling programs.

Investment & Funding Patterns: USD 250 M in new production expansions in Asia; venture financing for catalyst development growing 12% annually.

Innovation & Future Outlook: Integration of AI in process optimization, energy-efficient reactors, and forward-looking projects to reduce production downtime by 20%.

The Acrolein market is increasingly influenced by its integration into pharmaceuticals, acrylic acid production, and agrochemical sectors. Recent innovations in continuous-flow production and advanced catalysts, alongside stringent environmental regulations, have improved operational efficiency and sustainability. Regional consumption trends indicate robust growth in Asia Pacific and Europe, driven by industrial expansion and technology adoption.

The Acrolein Market holds strategic significance as a vital intermediate in chemical manufacturing, driving industrial efficiency and sustainability. Advanced continuous-flow reactor technology delivers 18% higher output compared to traditional batch systems. China dominates in production volume, while Europe leads in technology adoption, with 65% of enterprises implementing automated process monitoring systems. By 2027, AI-assisted catalytic optimization is expected to reduce chemical process downtime by 12%, enabling more resilient production cycles. Firms are committing to VOC emission reductions and solvent recycling improvements, targeting a 20% decrease in environmental impact by 2030. In 2025, a Chinese chemical producer achieved an 18% improvement in yield through catalytic innovation, highlighting measurable benefits of technology adoption. Looking forward, the Acrolein Market is positioned as a pillar of compliance, industrial efficiency, and sustainable growth, supporting the broader chemical value chain while aligning with ESG imperatives.

The Acrolein Market is shaped by evolving industrial demand, technological advancements, and regulatory frameworks. Increasing adoption of acrylic acid intermediates, pharmaceuticals, and agrochemicals drives consistent production growth. Technological integration, such as continuous-flow systems and advanced catalytic processes, enhances yield efficiency and reduces waste. Environmental regulations, especially VOC emission standards in Europe and North America, are influencing production practices. Market dynamics are further influenced by raw material availability, operational cost optimization, and industrial automation adoption. Growing investments in R&D for process optimization, coupled with strategic partnerships, support innovation while addressing regional consumption patterns and demand for high-purity Acrolein.

The pharmaceutical sector significantly drives Acrolein demand, as it serves as a key intermediate for active pharmaceutical ingredients. With over 60% of chemical producers supplying intermediates for drug synthesis, technological upgrades such as automated monitoring and precision oxidation processes have improved yields by 15–18%. Regulatory incentives for high-purity chemical production further accelerate adoption, particularly in China and Europe. Increasing global health expenditure and pharmaceutical manufacturing expansion are expected to sustain demand, reinforcing Acrolein’s strategic relevance in industrial applications.

Stringent environmental standards, particularly VOC emission limits in North America and Europe, restrict traditional Acrolein production methods. Facilities must invest in emission control technologies, such as scrubbers and advanced catalysts, adding 10–15% operational costs. In 2024, approximately 40% of older chemical plants underwent retrofitting to comply with these standards. Delays in approvals and the high cost of sustainable technology adoption constrain expansion, especially for small and medium-sized producers relying on legacy production systems.

Acrolein’s use in herbicide and pesticide intermediates presents substantial growth potential. With the agrochemical sector accounting for 35% of industrial chemical intermediates globally, demand for higher-purity, cost-efficient Acrolein is increasing. Advanced catalysts and continuous-flow systems can improve production efficiency by 18–20%, enabling producers to scale for regional farming projects in Asia and Latin America. Emerging trends in sustainable agriculture and integrated pest management drive the development of specialized Acrolein derivatives, creating new revenue and innovation pathways.

Raw material price volatility, particularly glycerol and propylene, imposes operational constraints, with costs fluctuating by 8–12% annually. Complex production processes require skilled labor and high-precision equipment; approximately 55% of small-scale facilities face operational inefficiencies. Supply chain disruptions, especially in Asia Pacific, affect consistent production schedules. Additionally, the need for compliance with safety and environmental standards further increases capital expenditure, challenging profitability and strategic expansion plans for chemical manufacturers.

Modular and Prefabricated Production Integration: Adoption of modular chemical reactors increased by 55% in 2024, reducing labor and operational costs while improving process precision. Europe and North America report the highest adoption due to stringent efficiency standards.

Advanced Catalysis Adoption: 48% of leading producers implemented new catalytic oxidation techniques, improving reaction efficiency and reducing by-products by 20%, enhancing sustainability in industrial applications.

AI-Enabled Process Monitoring: Automated AI-assisted systems are now deployed by 60% of large-scale facilities, enabling real-time quality control and minimizing downtime by 15%.

Sustainable and Green Initiatives: Chemical recycling and VOC emission control adoption reached 42% in 2024, driving compliance with ESG goals and reducing environmental footprint across Asia Pacific and Europe.

The Global Acrolein Market is systematically segmented by type, application, and end-user to offer granular insights into industrial demand patterns and operational focus areas. By type, the market captures variations in chemical composition and production methodology, reflecting manufacturers’ technological capabilities and process optimization. Application-based segmentation highlights the diverse utilization of Acrolein across acrylic acid intermediates, agrochemicals, and pharmaceutical syntheses, emphasizing efficiency and product purity requirements. End-user segmentation identifies industrial consumers, research institutions, and specialized manufacturing units, offering a clear perspective on adoption trends, usage volumes, and investment priorities. These segments reveal critical insights for resource allocation, capacity planning, and strategic partnerships, allowing decision-makers to identify areas of high operational efficiency, technological leverage, and emerging innovation. Regional consumption patterns further indicate targeted demand clusters, highlighting industrial hubs and production-intensive geographies that shape the overall market landscape.

The Acrolein market is primarily classified into Liquid Acrolein, Stabilized Acrolein, and Other Derivatives. Liquid Acrolein is the leading type, accounting for approximately 60% of total adoption, driven by its versatility as a chemical intermediate for acrylic acid synthesis and industrial applications requiring precise reactive properties. Stabilized Acrolein holds around 25% of adoption, benefiting from safer handling and storage protocols, while Other Derivatives collectively contribute 15%, often utilized in niche specialty chemical applications. Liquid Acrolein’s dominance is supported by enhanced production technologies, such as catalytic oxidation, which improve yield and reduce impurities. Stabilized forms are witnessing rapid uptake in regions emphasizing safety and regulatory compliance, with adoption expected to grow significantly.

Applications of Acrolein include Acrylic Acid Production, Agricultural Chemicals, Pharmaceutical Intermediates, and Other Industrial Uses. Acrylic Acid Production remains the leading application, representing 55% of usage, due to high demand for polymers and resins in paints, adhesives, and coatings. Agricultural Chemicals are the fastest-growing segment, with adoption driven by the need for efficient herbicides and pesticides, currently contributing 22% of applications. Other applications, such as specialized intermediates for polymer manufacturing, make up the remaining 23% of the market. Consumer Adoption & Trends: In 2024, more than 38% of agrochemical producers globally adopted Acrolein-based intermediates to improve herbicide effectiveness. Over 60% of pharmaceutical firms use Acrolein derivatives in API synthesis, enhancing purity and process consistency.

The leading end-user segment of the Acrolein Market is Industrial Chemical Manufacturers, accounting for approximately 57% of adoption, reflecting its central role in large-scale production of acrylic acid and polymer intermediates. Pharmaceutical and Agrochemical firms are the fastest-growing end-users, with adoption expanding due to automation in synthesis processes and demand for high-purity intermediates, representing 28% of adoption. Remaining end-users, including research institutions and specialty chemical processors, contribute 15%, primarily for experimental or niche applications. Consumer Adoption & Trends: In 2024, over 42% of industrial chemical plants globally incorporated automated process monitoring systems to optimize yield and reduce downtime. Additionally, more than 35% of agrochemical end-users implemented stabilized Acrolein solutions for safer storage and handling.

Asia-Pacific accounted for the largest market share at 45% in 2024, however, North America is expected to register the fastest growth, expanding at a CAGR of 3.5% between 2025 and 2032.

In 2024, Asia-Pacific consumed over 530,000 tons of Acrolein, supported by industrial hubs in China, Japan, and India. North America and Europe followed with volumes of 220,000 tons and 180,000 tons respectively. Emerging markets in South America reached 50,000 tons, while the Middle East & Africa accounted for 25,000 tons. Advanced manufacturing technologies, regulatory compliance, and automated process adoption are shaping the market landscape. Regional consumer behavior shows Asia-Pacific favoring high-volume industrial applications, Europe prioritizing sustainability and compliance, and North America adopting AI-driven process optimizations.

North America holds 18% of the global Acrolein market, driven by key industries including pharmaceuticals, agrochemicals, and polymer intermediates. Regulatory changes such as VOC emission standards and government incentives for green chemistry have accelerated adoption of stabilized Acrolein and digital process monitoring. Technological advancements include AI-assisted reaction monitoring and continuous-flow reactors, improving yield efficiency by 15–17%. Local players such as Arkema Inc. have implemented automated catalytic systems across multiple facilities, optimizing throughput and safety. Regional consumer behavior shows higher enterprise adoption in healthcare, finance, and chemical manufacturing sectors, with over 40% of large plants integrating real-time monitoring to reduce operational downtime.

Europe contributes 15% of global Acrolein consumption, with Germany, France, and the UK leading production and usage. Regulatory bodies enforce stringent VOC emission limits and sustainability initiatives, prompting adoption of stabilized Acrolein and automated process technologies. Emerging technologies such as catalytic oxidation and digital monitoring have been integrated in over 35% of facilities, improving process efficiency. Local players like BASF SE have modernized European plants with advanced safety and monitoring systems. Consumer behavior in Europe is influenced by regulatory pressure, with chemical manufacturers emphasizing traceability, efficiency, and ESG compliance across operations.

Asia-Pacific represents 45% of global Acrolein market volume, with top-consuming countries being China, India, and Japan. The region’s infrastructure supports large-scale chemical manufacturing, with over 120,000 tons produced annually in China alone. Technology trends include continuous-flow reactors, automated catalytic systems, and integrated process monitoring across industrial hubs. Companies such as Sinopec have expanded production lines with energy-efficient reactors, boosting operational throughput. Consumer behavior in Asia-Pacific favors high-volume applications for acrylic acid production, agrochemical intermediates, and pharmaceutical synthesis, with more than 60% of enterprises adopting advanced digital solutions for process optimization.

South America accounts for 4% of the global Acrolein market, with Brazil and Argentina as key contributors. Growth is supported by the chemical, energy, and agrochemical sectors, with investments in modernized processing infrastructure. Government incentives include tax benefits and trade facilitation for chemical imports. Local players such as Braskem have implemented advanced catalytic systems in specialty chemical production. Regional consumer behavior shows demand closely tied to agricultural output, industrial polymers, and localized production requirements, with over 35% of enterprises adopting stabilized Acrolein to ensure safe handling and storage.

Middle East & Africa holds 2% of global Acrolein consumption, with UAE and South Africa as leading markets. Regional demand is primarily in oil & gas, construction chemicals, and agrochemical intermediates. Technological modernization includes automated reaction monitoring and process optimization in approximately 25% of facilities. Local regulations and trade partnerships facilitate chemical imports and safe handling standards. Players like Sasol Ltd. have upgraded plants with digital monitoring and catalytic optimization systems. Regional consumer behavior shows a preference for safe, stable Acrolein solutions in industrial applications, particularly in construction and energy sectors.

China – 32% Market Share: High production capacity, large-scale industrial adoption, and advanced technological integration drive dominance.

United States – 18% Market Share: Strong end-user demand in pharmaceuticals, agrochemicals, and polymer intermediates, coupled with digital process monitoring initiatives.

The global Acrolein market exhibits a moderately consolidated competitive structure, with roughly 8–12 active major producers alongside a broad base of smaller regional suppliers. The top five companies collectively account for approximately 45–55% of global production capacity, underscoring a substantial but not fully monopolized market.

Major players such as Evonik Industries AG, Arkema S.A., The Dow Chemical Company, and leading Asian manufacturers like Hubei Jinghong Chemical Co., Ltd. and Wuhan Ruiji Chemical Co., Ltd. compete on capacity, product purity, downstream integration, and sustainability. Evonik leads with approximately 24%–28% share in high‑purity acrolein, leveraging vertically integrated production, advanced catalytic oxidation processes, and closed‑loop waste recycling systems for margin and compliance advantages.

Competition has recently intensified around sustainable production — several firms are investing in bio‑based acrolein production routes (e.g., glycerol dehydration) and optimized catalytic processes. Some regional producers in Asia are expanding capacity rapidly to capture rising demand for agrochemical intermediates and water‑treatment chemicals, often using cost‑effective production methods to challenge incumbents.

Strategic initiatives shaping competition include expansion of production capacity, adoption of green chemistry processes, and vertical integration with downstream products (e.g., methionine, acrylic acid derivatives). Leaders emphasize quality, supply reliability, and regulatory-compliant production. As a result, while the top players maintain dominance, a diversified group of mid‑ to small‑scale producers ensures that the market remains neither monopolized nor completely fragmented — but rather competitively balanced with room for new entrants and innovations.

Hubei Jinghong Chemical Co., Ltd.

Wuhan Ruiji Chemical Co., Ltd.

Daicel Corporation

Hubei Shengling Technology Co., Ltd.

Technological innovation is playing a critical role in shaping the future of the Acrolein market. Traditional production relies on propylene oxidation, but increasing environmental and regulatory pressure has spurred the development and scaling of bio‑based production routes — notably glycerol dehydration. Recent trends indicate that glycerol‑derived acrolein now represents a growing portion of total output, offering lower carbon footprint and compliance advantages.

Advancements in catalytic oxidation remain central: leading producers have optimized catalysts to deliver high‑purity acrolein suitable for pharmaceutical and specialty chemical applications, with purity levels reaching ≈ 99.8% in some cases. Closed‑loop recycling systems and waste‑minimizing reactor designs are helping firms meet stricter global emission and chemical‑safety standards, aligning production with ESG and regulatory compliance goals.

Digitalization and process automation are also gaining traction: companies increasingly deploy real-time monitoring, process-control systems, and optimized oxidation reactors to enhance yield consistency, reduce by-products, and lower operational costs. This improves process reliability and supports rapid scalability to meet growing demand in agrochemical, polymer, and water‑treatment segments.

There is a clear shift toward vertical integration and downstream coupling: acrolein producers are integrating production with derivative manufacturing — such as methionine, acrylic acid, glutaraldehyde — to improve supply chain control, margin stability, and product quality.

Emerging technologies under exploration include biomass‑based feedstock utilisation, advanced catalyst regeneration systems, reactor intensification, and closed-loop waste treatment — all catering to sustainability, cost efficiency, and regulatory compliance. Collectively, these technological developments are strengthening the competitive edge of established players and enabling new entrants with eco‑efficient production models.

In January 2024, Evonik Industries AG launched a new phosphate‑methacrylate monomer called VISIOMER® HEMA‑P 100, designed for coatings, adhesives and composites — a move reflecting its broader push into high‑performance, specialty chemicals that often rely on acrolein-derived intermediates. Source: www.evonik.com

In April 2024, DAICEL Corporation signed a collaboration agreement with Industrial Technology Research Institute (ITRI) to launch a “Cooperate Accelerator Program” — aimed at accelerating startup‑driven innovation in chemical materials, potentially including acrolein‑based chemistries or alternative feedstock/biomass‑derived intermediates. Source: www.daicel.com

In 2023, firms in the chemical sector (including companies with known acrolein exposure) increased their focus on bio‑based production routes and sustainable chemistries to replace fossil‑based feedstocks. Industry reports note rising investments in glycerol‑to‑acrolein (or aldehyde) processes, aligning acrolein supply with sustainability trends.

In 2023–2024, several leading chemical companies reportedly expanded or upgraded their acrolein‑derivative production facilities and product portfolios — targeting downstream applications such as specialty coatings, water‑treatment agents, agrochemical intermediates, and high‑performance polymers. This reflects increasing demand-side diversification for acrolein-based products beyond traditional uses. Source: www.openpr.com

This Acrolein Market Report encompasses a comprehensive global scope, covering multiple dimensions essential for strategic decision-making. The report evaluates the market across product types (e.g., high-purity acrolein, standard-grade, stabilized forms, derivatives), applications (including methionine synthesis for animal feed, polymer intermediates, agrochemicals, water treatment, glutaraldehyde production, and specialty chemicals), and end-user industries (animal nutrition, pharmaceuticals, agrochemical manufacturing, water treatment, coatings, polymers).

Geographically, the report analyzes all major regions — Asia‑Pacific, Europe, North America, South America, and Middle East & Africa — with country‑level insights for nations such as China, USA, Germany, Japan, Brazil, UAE, and others exhibiting significant demand or production capacity. It also evaluates production methods and technology pathways, comparing traditional propylene oxidation with emerging bio‑based glycerol dehydration, and assessing capacity expansions, sustainability initiatives, and downstream integration strategies.

The scope extends to market structure analysis — competitive landscape, company profiling, capacity share distribution, as well as innovation trends, regulatory impacts, ESG compliance, and supply chain dynamics. The report additionally considers niche and emerging segments, such as high‑purity acrolein for pharmaceuticals, bio‑derived acrolein for green chemicals, and derivative‑driven specialty applications, giving a broad yet detailed perspective for analysts, investors, and decision‑makers.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 1,178.4 Million |

| Market Revenue (2032) | USD 1,525.5 Million |

| CAGR (2025–2032) | 3.28% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments, Regulatory Overview |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Evonik Industries AG, Arkema S.A., The Dow Chemical Company, Hubei Jinghong Chemical Co., Ltd., Wuhan Ruiji Chemical Co., Ltd., Daicel Corporation, Hubei Shengling Technology Co., Ltd. |

| Customization & Pricing | Available on Request (10% Customization Free) |