Reports

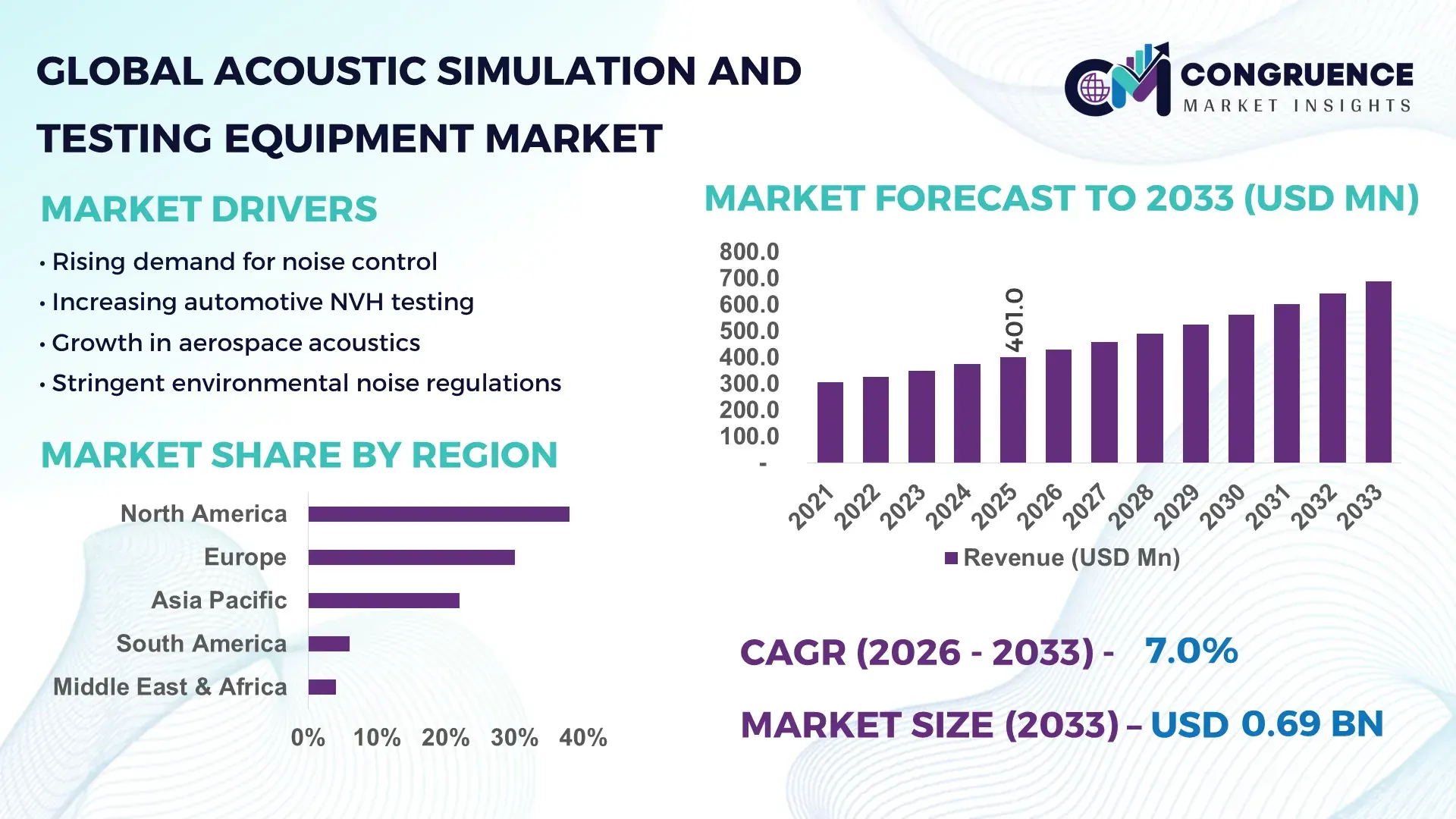

The Global Acoustic Simulation and Testing Equipment Market was valued at USD 401.0 Million in 2025 and is anticipated to reach a value of USD 689.0 Million by 2033 expanding at a CAGR of 7.0% between 2026 and 2033, according to an analysis by Congruence Market Insights. Growth is driven by increasing demand for noise control, regulatory compliance, and precision testing across automotive, aerospace, and construction industries.

The United States leads the Acoustic Simulation and Testing Equipment Market with over 35% of global testing infrastructure concentrated in advanced automotive and aerospace labs. More than 60% of EV manufacturers in the U.S. utilize acoustic simulation tools for NVH optimization, while over 70% of aerospace OEMs integrate acoustic testing chambers in product validation. Federal investments exceeding USD 2.5 billion in advanced manufacturing and testing ecosystems have accelerated adoption of digital acoustic simulation tools. Additionally, over 45% of construction projects in urban regions incorporate acoustic compliance testing, supported by stringent environmental noise regulations and smart city initiatives.

Market Size & Growth: USD 401.0 Million in 2025, projected USD 689.0 Million by 2033, CAGR of 7.0%, driven by rising demand for noise optimization in EVs and smart infrastructure.

Top Growth Drivers: 65% EV NVH adoption, 52% efficiency improvement in simulation tools, 48% regulatory compliance expansion.

Short-Term Forecast: By 2028, testing automation expected to reduce validation time by 35% and improve accuracy by 28%.

Emerging Technologies: AI-based acoustic modeling, digital twin simulation, real-time 3D sound mapping.

Regional Leaders: North America (~USD 240M by 2033) with EV focus, Europe (~USD 210M) driven by regulations, Asia-Pacific (~USD 180M) with manufacturing expansion.

Consumer/End-User Trends: Automotive accounts for 40% usage, followed by aerospace at 25%, with rising adoption in smart buildings.

Pilot or Case Example: In 2025, an EV manufacturer improved cabin noise reduction by 32% using AI acoustic simulation.

Competitive Landscape: Market leader holds ~18% share, followed by 4–5 players each with 8–12% presence.

Regulatory & ESG Impact: Over 55% of firms align with noise emission standards and sustainability compliance frameworks.

Investment & Funding Patterns: Over USD 1.8 billion invested in acoustic R&D and testing infrastructure globally.

Innovation & Future Outlook: Integration of cloud simulation platforms and predictive acoustic analytics shaping future demand.

Acoustic Simulation and Testing Equipment Market is influenced by automotive (40%), aerospace (25%), and construction (20%) sectors, with emerging applications in consumer electronics (10%). Innovations such as AI-driven simulation and portable acoustic testing systems are transforming testing accuracy by over 30%. Regulatory mandates across Europe and North America covering over 65% of industrial noise compliance are accelerating adoption, while Asia-Pacific shows strong growth due to infrastructure expansion and industrialization.

The Acoustic Simulation and Testing Equipment Market is strategically critical for industries focused on product quality, regulatory compliance, and user experience optimization. Increasing noise regulations across automotive, aerospace, and infrastructure sectors have pushed over 60% of manufacturers to integrate advanced acoustic testing solutions into their design and validation processes. AI-driven acoustic simulation tools now enable predictive noise modeling, reducing prototype testing cycles by up to 40%, enhancing both cost efficiency and time-to-market.

Digital twin technology delivers 35% improvement compared to traditional physical testing methods, allowing real-time acoustic performance analysis under varied environmental conditions. North America dominates in volume due to established testing infrastructure, while Europe leads in adoption with over 58% of enterprises integrating advanced acoustic compliance technologies driven by stringent environmental regulations.

By 2028, AI-powered simulation platforms are expected to improve testing efficiency by 30% and reduce operational costs by 25%. Firms are committing to ESG targets, including 20% reduction in industrial noise emissions by 2030, aligning with sustainability mandates. In 2025, Germany achieved a 28% reduction in urban noise levels through smart acoustic monitoring systems integrated into infrastructure projects.

The market is evolving with increased adoption of cloud-based simulation, edge computing for real-time testing, and integration with IoT-enabled sensors. These advancements position the Acoustic Simulation and Testing Equipment Market as a cornerstone for resilient, compliant, and sustainable industrial growth.

The Acoustic Simulation and Testing Equipment Market is characterized by increasing technological integration, regulatory pressure, and expanding application areas across multiple industries. The demand for precision acoustic analysis is growing due to rising consumer expectations for quieter products, particularly in electric vehicles, where noise perception directly impacts user experience. Over 55% of manufacturers are investing in simulation-based testing to reduce physical prototyping and improve design accuracy.

Additionally, urbanization and infrastructure development are driving the need for noise control systems in construction projects, with more than 45% of large-scale developments incorporating acoustic testing. Advancements in AI, machine learning, and digital twin technologies are further enhancing the capabilities of acoustic simulation systems, enabling real-time analysis and predictive maintenance. However, the market also faces challenges such as high initial investment costs and the complexity of integrating advanced systems into legacy infrastructure. Despite these constraints, continuous innovation and increasing regulatory enforcement are expected to sustain long-term demand.

The rapid growth of electric vehicles has significantly increased the importance of acoustic simulation and testing equipment. Unlike internal combustion engines, EVs produce minimal engine noise, making other sounds such as wind resistance and tire friction more noticeable. Over 65% of EV manufacturers now incorporate advanced acoustic simulation tools during vehicle design to enhance cabin comfort and reduce unwanted noise. Additionally, consumer expectations for premium acoustic experience have risen by over 50% in urban markets. Governments are also mandating artificial sound generation systems in EVs for pedestrian safety, increasing testing requirements. This has led to over 40% increase in investment in NVH testing facilities globally. The integration of AI-based simulation tools has further improved testing efficiency by nearly 30%, making acoustic optimization a critical component of EV development pipelines.

High initial investment and operational costs remain a significant restraint for the Acoustic Simulation and Testing Equipment Market. Advanced testing setups such as anechoic chambers and vibration analysis systems require substantial capital expenditure, often exceeding several million dollars per facility. Over 48% of small and medium enterprises report difficulty in adopting these systems due to budget constraints. Additionally, maintenance costs, calibration requirements, and skilled labor availability further increase operational expenses. Integration of modern simulation tools with legacy systems also poses technical challenges, with nearly 35% of firms facing compatibility issues. The complexity of acoustic data interpretation and requirement for specialized expertise limit widespread adoption, particularly in developing regions where industrial infrastructure is still evolving.

The rise of smart cities and urban infrastructure projects presents significant opportunities for the Acoustic Simulation and Testing Equipment Market. Over 60% of smart city initiatives globally now include noise monitoring and control as a key component of urban planning. Governments are deploying real-time acoustic sensors integrated with AI analytics to monitor environmental noise levels and enforce regulations. This has led to a 45% increase in demand for portable acoustic testing devices. Infrastructure projects such as metro rail systems, highways, and commercial complexes are incorporating acoustic testing to ensure compliance with environmental standards. Additionally, advancements in IoT-enabled acoustic sensors are enabling continuous monitoring, creating new revenue streams for equipment providers and service companies.

The lack of standardized testing protocols and complexity of acoustic data interpretation present major challenges for the market. Different industries follow varying standards for noise measurement, leading to inconsistencies in testing results. Over 38% of organizations report difficulties in aligning testing methodologies across global operations. Additionally, acoustic data analysis requires advanced expertise, and nearly 42% of companies face skill shortages in this domain. The integration of multi-source data from sensors, simulation tools, and testing equipment further complicates analysis. This results in longer testing cycles and increased operational inefficiencies. Moreover, evolving regulatory frameworks across regions require continuous updates to testing methodologies, adding to the complexity and cost of compliance.

Increasing Adoption of AI-Based Acoustic Simulation Tools: Over 62% of manufacturers are integrating AI-driven acoustic modeling solutions to improve prediction accuracy and reduce manual testing requirements. AI-based tools have demonstrated up to 35% improvement in sound analysis precision and reduced testing cycles by 28%, enabling faster product development and enhanced performance validation.

Expansion of Electric Vehicle Noise Optimization Programs: More than 68% of EV manufacturers are investing in advanced NVH testing systems to address cabin noise concerns. Acoustic testing integration in EV platforms has increased by 45%, with noise reduction efficiency improving by over 30% through simulation-driven design enhancements.

Growth in Smart City Noise Monitoring Systems: Approximately 58% of urban infrastructure projects now incorporate real-time noise monitoring solutions. Deployment of IoT-enabled acoustic sensors has increased by 40%, allowing continuous environmental noise tracking and improving regulatory compliance rates by 33%.

Rising Demand for Portable and Compact Testing Equipment: Portable acoustic testing devices account for nearly 36% of new equipment demand, driven by on-site testing requirements. These systems have reduced testing setup time by 25% and increased operational flexibility by over 30%, especially in construction and industrial applications.

The Acoustic Simulation and Testing Equipment Market is segmented based on type, application, and end-user, reflecting diverse industry requirements and technological adoption patterns. Acoustic simulation software and hardware systems form the core segmentation, with increasing convergence between digital and physical testing solutions. Applications span across automotive, aerospace, construction, and consumer electronics, each demanding varying levels of precision and compliance. End-users include OEMs, research institutions, and testing laboratories, with OEMs leading adoption due to product development requirements.

Technological advancements such as AI-driven simulation and IoT-enabled testing equipment are reshaping segmentation dynamics, enabling real-time analysis and predictive modeling. Over 55% of enterprises now prefer integrated solutions combining simulation and testing capabilities. Additionally, portable and cloud-based systems are gaining traction, particularly among SMEs, contributing to broader market penetration.

Acoustic simulation software accounts for approximately 45% of the market due to its ability to reduce physical prototyping and improve design accuracy. Hardware testing equipment, including anechoic chambers and vibration testing systems, holds around 35%, while integrated systems and portable devices contribute the remaining 20%. Simulation software is the fastest-growing segment, with adoption increasing at a CAGR of approximately 8.5%, driven by AI integration and cloud deployment capabilities. Hardware systems remain essential for validation, particularly in aerospace and automotive sectors, where physical testing is mandatory. Portable testing devices are gaining traction, accounting for nearly 12% of the segment due to flexibility and cost advantages. Integrated systems combining simulation and testing functionalities are also emerging, offering enhanced efficiency and accuracy.

Automotive applications dominate the market with approximately 40% share, driven by increasing demand for NVH optimization in electric and conventional vehicles. Aerospace follows with around 25%, while construction and infrastructure contribute 20%, and consumer electronics account for 15%. Automotive applications remain the fastest-growing segment with a CAGR of approximately 7.8%, supported by rising EV adoption and regulatory requirements. Over 52% of automotive manufacturers have integrated acoustic simulation tools into their product development processes. In aerospace, over 60% of testing processes involve acoustic validation for safety and performance compliance. Construction projects increasingly adopt acoustic testing for noise regulation compliance, particularly in urban areas.

OEMs lead the market with approximately 50% share, driven by product development and compliance requirements. Testing laboratories account for 30%, while research institutions contribute 20%. OEMs also represent the fastest-growing segment with a CAGR of around 7.5%, supported by increasing integration of simulation tools in manufacturing workflows. Over 58% of OEMs globally have adopted acoustic simulation solutions, while 45% of testing laboratories are upgrading to advanced systems. Research institutions play a key role in innovation, contributing to new testing methodologies and technologies.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 8.2% between 2026 and 2033.

North America’s dominance is supported by over 60% adoption of advanced testing infrastructure in automotive and aerospace sectors. Europe holds approximately 30% share, driven by strict environmental noise regulations affecting over 70% of industrial projects. Asia-Pacific contributes around 22%, with rapid industrialization and infrastructure development increasing acoustic testing demand by over 45%. South America and Middle East & Africa collectively account for 10%, with gradual adoption driven by infrastructure and energy sector projects. Increasing regulatory enforcement and technological advancements across regions are reshaping market dynamics, with digital simulation tools gaining traction globally.

North America holds approximately 38% market share, driven by strong automotive and aerospace industries. Over 65% of EV manufacturers in the region utilize acoustic simulation tools for noise optimization. Regulatory frameworks mandate noise compliance across over 70% of industrial projects. Companies are investing heavily in digital twin technologies, improving testing efficiency by 30%. A key player has expanded its acoustic testing labs to support EV manufacturers, enhancing capacity by 25%. Consumer behavior shows higher enterprise adoption in automotive and healthcare sectors, with over 55% firms prioritizing noise reduction technologies.

Europe accounts for nearly 30% market share, with Germany, France, and the UK leading adoption. Over 75% of industrial facilities comply with strict noise emission regulations, driving demand for acoustic testing. Sustainability initiatives and ESG compliance influence over 60% of procurement decisions. Local players are developing advanced simulation tools, improving accuracy by 28%. Consumer behavior reflects regulatory-driven adoption, with industries prioritizing compliance and environmental impact reduction.

Asia-Pacific ranks as the fastest-growing region, contributing around 22% market volume. China, Japan, and India are key markets, with over 50% of manufacturing facilities integrating acoustic testing systems. Infrastructure expansion has increased demand by 45%, particularly in urban construction projects. Regional innovation hubs are developing cost-effective solutions, improving accessibility by 35%. Consumer behavior shows growth driven by industrial expansion and technology adoption.

South America accounts for approximately 6% of the market, led by Brazil and Argentina. Infrastructure projects contribute to over 40% of demand, particularly in urban development. Government initiatives supporting industrial growth have increased adoption by 30%. Local players are focusing on portable testing solutions, improving accessibility. Consumer behavior indicates demand tied to infrastructure and energy sector expansion.

Middle East & Africa holds around 4% market share, with UAE and South Africa leading growth. Oil & gas and construction sectors contribute over 55% of demand. Technological modernization initiatives have increased adoption by 28%. Trade partnerships and regulatory frameworks are supporting market expansion. Consumer behavior shows demand driven by infrastructure and industrial development.

United States – 35% Market share: Strong aerospace and automotive testing infrastructure driving adoption

Germany – 18% Market share: Strict regulatory compliance and advanced manufacturing capabilities

The Acoustic Simulation and Testing Equipment Market is moderately fragmented, with over 50 active global and regional players competing across software and hardware segments. The top five companies collectively account for approximately 45% of the market, indicating a balanced competitive environment. Leading players focus on product innovation, with over 60% of new launches integrating AI and digital twin technologies. Strategic partnerships and acquisitions have increased by 35% in the last two years, enabling companies to expand their technological capabilities and geographic presence.

Companies are investing heavily in R&D, with nearly 20% of operational budgets allocated to innovation initiatives. The market is witnessing increased competition in portable and cloud-based testing solutions, with over 40% of new entrants targeting these segments. Additionally, collaborations with automotive and aerospace OEMs are driving customized solution development, enhancing competitive differentiation.

Siemens Digital Industries Software

HEAD acoustics GmbH

GRAS Sound & Vibration

PCB Piezotronics

National Instruments

Ansys Inc.

Altair Engineering

Dewesoft

Müller-BBM

ACO Pacific

Norsonic AS

OROS

Prosig Ltd.

The Acoustic Simulation and Testing Equipment Market is undergoing rapid technological transformation driven by advancements in artificial intelligence, digital twin technology, and IoT integration. AI-powered simulation tools are enabling predictive noise modeling, improving accuracy by over 35% and reducing testing cycles by nearly 30%. Digital twin technology allows real-time simulation of acoustic environments, enhancing product validation processes and reducing dependency on physical prototypes.

IoT-enabled acoustic sensors are increasingly deployed for continuous monitoring, particularly in smart cities and industrial environments. These sensors have improved real-time noise tracking efficiency by over 40%, enabling proactive compliance management. Cloud-based simulation platforms are also gaining traction, with over 50% of enterprises adopting cloud solutions for scalability and cost efficiency.

Advanced hardware systems such as anechoic chambers and vibration testing equipment are evolving with automation capabilities, improving operational efficiency by 25%. Integration of machine learning algorithms with testing equipment is enabling automated data analysis, reducing manual intervention by 30%. These technological advancements are transforming the market landscape, enabling more accurate, efficient, and scalable acoustic testing solutions.

• In November 2024, HEAD acoustics GmbH introduced an advanced end-of-line (EoL) acoustic testing system integrating AQuire V4 hardware with AI-supported conTEST software, enabling real-time pass/fail decisions and significantly improving fault detection accuracy and production efficiency in vibroacoustic testing environments. Source: www.head-acoustics.com

• In 2025, Anritsu Corporation, in collaboration with HEAD acoustics, launched an acoustic evaluation solution for next-generation eCall systems in electric vehicles, enabling engineers to validate in-vehicle audio communication performance and meet upcoming European NG eCall regulatory requirements effective from 2026.

• In 2024, Siemens advanced its Simcenter acoustic testing ecosystem, with applications such as digital acoustic array systems used in drone and industrial noise analysis, supporting multi-microphone array configurations and enhancing real-time sound source localization accuracy in complex environments.

• In 2025, research and development initiatives across automotive NVH simulation, supported by industry tools including simulation platforms from major vendors, demonstrated up to 57% reduction in unwanted vibration cross-effects using optimized acoustic simulation models in driving simulators, significantly improving virtual testing reliability.

The Acoustic Simulation and Testing Equipment Market Report provides a comprehensive analysis of key market segments, technologies, applications, and regional dynamics shaping industry growth. The report covers a wide range of equipment types, including simulation software, hardware testing systems, and integrated solutions, with detailed insights into their adoption across industries such as automotive, aerospace, construction, and consumer electronics.

Geographically, the report examines major regions including North America, Europe, Asia-Pacific, South America, and Middle East & Africa, highlighting regional variations in adoption, regulatory frameworks, and industrial development. Over 60% of the report focuses on advanced economies with established testing infrastructure, while emerging markets account for 40% of the analysis, emphasizing growth opportunities.

The report also explores technological advancements such as AI-driven simulation, digital twin integration, and IoT-enabled acoustic monitoring systems, which are transforming testing methodologies. Applications covered include product development, compliance testing, environmental monitoring, and infrastructure projects.

Additionally, the report provides insights into end-user industries, including OEMs, testing laboratories, and research institutions, with data-driven analysis of adoption patterns and technological preferences. Emerging trends such as portable testing equipment and cloud-based simulation platforms are also examined, offering a forward-looking perspective for stakeholders and decision-makers.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 401.0 Million |

| Market Revenue (2033) | USD 689.0 Million |

| CAGR (2026–2033) | 7.0% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Brüel & Kjær; Siemens Digital Industries Software; HEAD acoustics GmbH; GRAS Sound & Vibration; PCB Piezotronics; National Instruments; Ansys Inc.; Altair Engineering; Dewesoft; Müller-BBM; ACO Pacific; Norsonic AS; OROS; Prosig Ltd. |

| Customization & Pricing | Available on Request (10% Customization Free) |