Reports

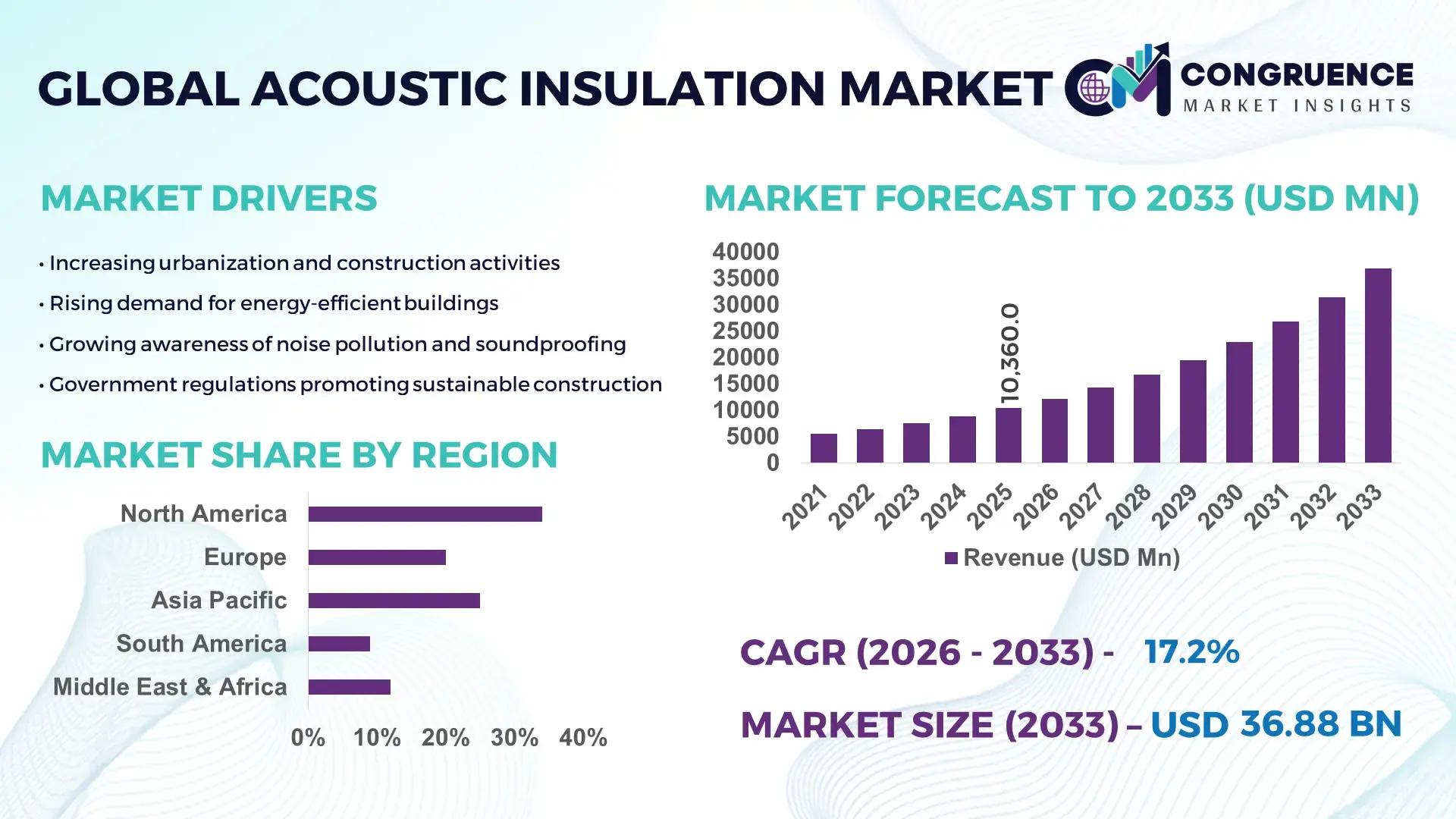

The Global Acoustic Insulation Market was valued at USD 10359.98 Million in 2025 and is anticipated to reach a value of USD 36879.06 Million by 2033 expanding at a CAGR of 17.2% between 2026 and 2033. Growth is primarily driven by stringent building energy codes and rising demand for advanced soundproofing solutions across residential, commercial, and industrial infrastructure.

The United States represents the most advanced acoustic insulation production ecosystem, supported by more than 140 large-scale mineral wool and fiberglass manufacturing facilities operating across multiple states. Annual building construction spending in the country exceeded USD 1.9 trillion in 2024, significantly accelerating demand for high-performance acoustic insulation panels, spray foam systems, and eco-friendly cellulose materials. Commercial real estate retrofits account for over 35% of total insulation upgrades, with healthcare and educational facilities adopting next-generation noise-control materials that reduce decibel transmission by up to 45%. Federal energy-efficiency programs and green building certifications have further encouraged technological innovation in recycled-content insulation, enhancing thermal-acoustic hybrid solutions for smart infrastructure projects.

Market Size & Growth: Valued at USD 10359.98 Million in 2025 and projected to reach USD 36879.06 Million by 2033 at a CAGR of 17.2%, fueled by accelerated urban construction and stricter environmental building standards.

Top Growth Drivers: 42% surge in green building adoption, 35% increase in infrastructure renovation projects, 28% rise in industrial noise compliance investments.

Short-Term Forecast: By 2028, advanced acoustic insulation materials are expected to improve energy efficiency in buildings by 18% while reducing noise transmission by 30%.

Emerging Technologies: Aerogel-based insulation composites, recycled mineral wool with low embodied carbon, and smart acoustic panels integrated with IoT-enabled monitoring systems.

Regional Leaders: North America projected to reach USD 11.8 Billion by 2033 with strong retrofit demand; Europe expected at USD 9.6 Billion driven by sustainability mandates; Asia-Pacific forecasted at USD 12.4 Billion supported by rapid urban housing expansion.

Consumer/End-User Trends: Residential housing accounts for over 40% of installations, while industrial facilities increasingly adopt high-density acoustic insulation to meet occupational safety standards.

Pilot or Case Example: In 2024, a large-scale smart hospital retrofit project achieved a 32% reduction in interior noise levels and 20% improvement in energy efficiency using advanced acoustic insulation panels.

Competitive Landscape: Owens Corning holds approximately 18% share, followed by Saint-Gobain, Rockwool International, Knauf Insulation, and Johns Manville.

Regulatory & ESG Impact: Carbon reduction mandates and zero-energy building codes are driving a 25% rise in demand for sustainable acoustic insulation materials with recycled content.

Investment & Funding Patterns: Over USD 2.3 Billion invested globally in advanced insulation manufacturing expansion and low-carbon material R&D between 2023 and 2025.

Innovation & Future Outlook: Integration of lightweight composite insulation, modular construction compatibility, and digital acoustic modeling tools are shaping next-generation building acoustics solutions.

The acoustic insulation market is strongly influenced by construction, transportation, and industrial manufacturing sectors, with building applications contributing nearly 55% of total demand. Automotive and rail industries collectively account for around 20% of installations due to increasing vehicle noise reduction standards. Technological innovations such as bio-based insulation fibers, vacuum insulation panels, and hybrid thermal-acoustic materials are reshaping product portfolios. Regulatory pressure related to occupational noise exposure and energy conservation continues to accelerate product adoption. Asia-Pacific exhibits the fastest consumption growth due to urban housing expansion and industrial infrastructure investments, while Europe emphasizes low-carbon, recyclable insulation systems. Forward-looking trends include circular economy integration, prefabricated building insulation modules, and advanced decibel-optimized material engineering to meet evolving global construction standards.

The Acoustic Insulation Market holds strategic relevance within global construction, transportation, and industrial infrastructure ecosystems, where compliance with noise control standards and energy performance benchmarks has become non-negotiable. As urban density increases and mixed-use developments expand, developers are prioritizing high-performance acoustic insulation systems that combine thermal efficiency, fire resistance, and decibel reduction. Aerogel-enhanced acoustic composites deliver 35% improvement in sound absorption compared to conventional fiberglass insulation, positioning advanced materials as a competitive differentiator in green building projects.

Asia-Pacific dominates in volume due to large-scale residential and commercial construction, while Europe leads in adoption with over 62% of enterprises integrating certified low-carbon insulation materials into new developments. By 2028, AI-driven building performance simulation is expected to improve acoustic optimization accuracy by 25%, enabling cost-efficient material deployment and reducing project rework. Firms are committing to ESG metrics such as 30% recycled content usage and 40% reduction in embodied carbon by 2030, aligning insulation production with decarbonization goals.

In 2024, a German construction consortium achieved a 28% reduction in interior noise transmission through digital acoustic modeling combined with high-density mineral wool systems. Over the next decade, the Acoustic Insulation Market is positioned as a pillar of resilient urban infrastructure, regulatory compliance, and sustainable growth, supporting long-term environmental targets and operational efficiency across multiple industries.

Rapid urban infrastructure expansion is significantly boosting the deployment of acoustic insulation across residential and commercial buildings. Global urban population levels have surpassed 56%, with projections indicating continued growth in metropolitan construction activity. High-rise apartments and mixed-use complexes require insulation systems capable of reducing airborne and impact noise by up to 50 decibels to comply with building codes. Public infrastructure investments, including airports, metros, and healthcare facilities, increasingly mandate certified acoustic performance standards. In education and healthcare settings, studies show that effective noise reduction can improve productivity and recovery rates by more than 20%, prompting higher specification of advanced insulation materials. These measurable performance benefits directly influence procurement policies, making acoustic insulation a critical component in modern construction strategies.

Raw material price volatility, particularly in mineral wool, petrochemical-based foams, and fiberglass, creates cost uncertainty for manufacturers and contractors. Energy-intensive production processes contribute to fluctuating manufacturing expenses, with energy costs accounting for nearly 30% of total production input in some facilities. Additionally, improper installation can reduce acoustic efficiency by up to 25%, increasing the need for skilled labor and certified contractors. In emerging markets, limited technical expertise and inconsistent enforcement of building codes slow adoption. Transportation costs for bulky insulation materials further impact project budgets, especially in remote infrastructure developments. These operational and cost-related constraints can delay procurement decisions and reduce immediate adoption rates despite strong long-term demand fundamentals.

Green building certifications and large-scale retrofit initiatives present substantial opportunities for acoustic insulation providers. More than 100,000 commercial projects worldwide are pursuing sustainability certifications that require enhanced indoor environmental quality and noise mitigation standards. Retrofitting aging office buildings and public infrastructure can reduce energy consumption by up to 30% when thermal-acoustic hybrid insulation systems are installed. Demand for bio-based and recycled insulation materials is expanding, particularly in Europe and North America, where low-carbon construction targets are enforced. Modular construction methods also create new product integration pathways, enabling pre-installed acoustic panels that shorten project timelines by approximately 15%. These structural shifts open avenues for innovative product differentiation and premium solution offerings.

Stringent fire safety and environmental compliance requirements pose operational challenges for acoustic insulation manufacturers. Building regulations increasingly demand fire-resistant materials capable of withstanding temperatures exceeding 1,000°C, requiring additional testing and certification. Compliance with chemical emission standards and waste disposal regulations raises R&D and production costs. Manufacturers must also meet evolving environmental directives that mandate reduced volatile organic compound emissions and higher recyclability rates. Certification processes can extend product launch timelines by several months, affecting speed to market. Smaller producers often face capital constraints in upgrading facilities to meet sustainability benchmarks, creating competitive pressure within the acoustic insulation ecosystem.

• Accelerated Adoption of High-Performance, Multi-Functional Insulation Materials: Advanced composite insulation materials combining thermal resistance, fire protection, and acoustic damping are gaining rapid traction. High-density mineral wool systems now achieve up to 50 dB sound reduction while improving thermal efficiency by 20% compared to single-function materials. Nearly 48% of newly approved commercial building projects specify hybrid insulation solutions to meet integrated building performance standards. Demand for thin-profile acoustic panels has increased by 33% in high-rise developments, where space optimization is critical. This measurable performance enhancement is driving product innovation pipelines across leading manufacturers.

• Expansion of Sustainable and Recycled Acoustic Insulation Solutions: Environmental compliance mandates are accelerating the shift toward low-carbon and recycled-content insulation products. More than 60% of large construction firms have committed to incorporating insulation materials with at least 25% recycled content by 2030. Bio-based acoustic insulation products have demonstrated up to 18% lower embodied carbon compared to traditional fiberglass systems. In Europe, approximately 58% of new public infrastructure projects now require Environmental Product Declarations (EPDs), reinforcing the demand for certified sustainable acoustic insulation solutions across institutional and commercial buildings.

• Rise in Modular and Prefabricated Construction Integration: The adoption of modular construction is reshaping demand dynamics in the Acoustic Insulation Market. Approximately 55% of newly commissioned projects report measurable cost efficiencies through prefabrication practices. Factory-installed acoustic insulation panels reduce on-site labor requirements by nearly 30% and shorten project timelines by up to 20%. Pre-cut, precision-engineered components manufactured using automated production lines enhance installation accuracy and reduce material waste by 15%. This trend is particularly pronounced in North America and Europe, where industrialized construction methods account for over 35% of urban residential developments.

• Increasing Industrial and Transportation Noise Compliance Requirements: Industrial facilities and transportation manufacturers are intensifying investments in acoustic insulation to comply with occupational noise exposure standards. Nearly 40% of manufacturing plants have upgraded internal soundproofing systems within the past three years to reduce noise levels below 85 dB workplace thresholds. In the automotive sector, lightweight acoustic insulation materials have reduced cabin noise by up to 25%, improving passenger comfort and vehicle quality ratings. Rail and metro infrastructure projects are integrating vibration-dampening insulation systems capable of decreasing structural noise transmission by 30%, supporting stricter urban noise regulations.

The Acoustic Insulation Market is segmented by type, application, and end-user, each reflecting differentiated demand patterns and compliance requirements. By type, mineral wool and fiberglass dominate due to their high-density structure and fire-resistant properties, while foam-based and bio-based insulation solutions are expanding in specialized use cases. In applications, building and construction accounts for the largest deployment, driven by residential and commercial soundproofing standards that require up to 50 dB noise reduction in multi-unit housing. Transportation applications, including automotive and rail, increasingly integrate lightweight acoustic materials to reduce cabin noise by approximately 20–25%. Industrial installations emphasize vibration control and machinery noise containment to meet workplace thresholds below 85 dB. From an end-user perspective, construction firms represent the primary adopters, while automotive manufacturers and infrastructure operators contribute significant volume demand. This structured segmentation enables manufacturers to align product development with regulatory, performance, and sustainability priorities across diverse verticals.

Mineral wool currently accounts for approximately 38% of total product adoption, driven by its superior fire resistance exceeding 1,000°C and ability to reduce airborne sound transmission by up to 50 dB. Fiberglass insulation follows with nearly 27% share, favored for its lightweight structure and cost efficiency in residential installations. While mineral wool and fiberglass together represent 65% of market deployment, foam-based acoustic insulation is expanding rapidly in specialized industrial and automotive applications. Polyurethane and melamine foam systems are the fastest-growing segment, advancing at an estimated CAGR of 8.5%, supported by demand for lightweight, high-absorption materials capable of reducing vibration and structure-borne noise by 30%.

Bio-based and recycled cellulose insulation collectively contribute around 15%, gaining traction due to sustainability mandates and requirements for 25–40% recycled content in certified green buildings. Aerogel-infused acoustic composites remain niche but strategically important for high-end commercial projects where space-saving insulation thickness of 50% less than conventional materials is required.

Building and construction applications account for nearly 55% of overall acoustic insulation usage, reflecting strict building codes that mandate minimum Sound Transmission Class (STC) ratings of 50 or higher in multi-unit residential properties. Commercial office and healthcare projects are particularly significant, as controlled acoustic environments can improve workplace productivity by up to 15%. Transportation applications, including automotive, aerospace, and rail, represent approximately 25% of installations, with manufacturers integrating lightweight insulation systems to reduce cabin noise by 20–30%.

Industrial applications are emerging as the fastest-growing segment, expanding at an estimated CAGR of 7.9%, driven by occupational safety regulations requiring workplace noise exposure below 85 dB. Manufacturing plants are increasingly retrofitting machinery enclosures with high-performance acoustic barriers capable of reducing operational noise by 35%. Other applications, including marine and specialized infrastructure projects, collectively contribute around 20% of demand, serving niche environments requiring vibration damping and moisture-resistant insulation.

Construction companies remain the leading end-user group, accounting for roughly 60% of total acoustic insulation deployment due to widespread residential, commercial, and institutional building projects. Infrastructure developers and real estate firms prioritize compliance with energy and acoustic performance standards, often integrating hybrid insulation systems that improve sound attenuation by 30% compared to legacy installations. Automotive manufacturers represent approximately 18% of end-user demand, incorporating lightweight acoustic foams and fiber-based insulation to meet interior cabin noise benchmarks below 70 dB.

Industrial manufacturing is the fastest-growing end-user segment, advancing at an estimated CAGR of 8.2%, fueled by stricter occupational safety regulations and automation-driven machinery installations that generate higher decibel levels. Facilities are adopting customized acoustic enclosures that reduce equipment noise by up to 40%. Other end-users, including rail operators, marine shipbuilders, and aerospace manufacturers, collectively contribute around 22% of market demand, particularly in vibration-sensitive and high-precision environments.

North America accounted for the largest market share at 34% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 8.9% between 2026 and 2033.

North America’s leadership is supported by annual construction spending exceeding USD 1.9 trillion and strict indoor noise regulations requiring Sound Transmission Class (STC) ratings above 50 in multi-family housing. Europe follows with approximately 28% share, driven by sustainability mandates requiring at least 25% recycled content in certified building materials. Asia-Pacific represents nearly 26% of total volume demand, with over 60% of consumption concentrated in China, India, and Japan due to rapid urban housing expansion and industrialization. South America holds close to 7%, supported by infrastructure modernization and energy-sector investments, while the Middle East & Africa accounts for about 5%, fueled by large-scale commercial real estate and oil & gas facility developments. Across regions, more than 45% of new commercial buildings globally now integrate high-density acoustic insulation systems to comply with occupational noise thresholds below 85 dB, reflecting a harmonized regulatory-driven demand structure.

How are stringent building codes and retrofit programs strengthening competitive positioning?

North America represents approximately 34% of the global Acoustic Insulation Market share, supported by robust residential retrofitting and commercial construction upgrades. The United States contributes over 75% of regional demand, with Canada accounting for nearly 15%. Healthcare, education, and commercial real estate are key industries driving adoption, as building standards require minimum STC ratings of 50–55 in multi-unit housing and patient-care environments. Updated energy-efficiency regulations encourage integration of hybrid thermal-acoustic materials capable of improving insulation performance by 20%. Digital building modeling tools are increasingly used, improving installation precision by 18% and reducing material waste by 12%. Owens Corning has expanded mineral wool production capacity in the region to meet rising retrofit demand. Regional consumer behavior indicates higher enterprise adoption in healthcare and corporate office spaces, where acoustic comfort is linked to productivity improvements of up to 15%.

Why are sustainability mandates and green certifications accelerating advanced insulation deployment?

Europe accounts for approximately 28% of the Acoustic Insulation Market, with Germany, the United Kingdom, and France representing over 60% of regional consumption. Regulatory bodies enforce strict environmental standards, requiring low-emission insulation materials and documented Environmental Product Declarations in more than 55% of new public projects. The construction sector emphasizes fire-resistant mineral wool systems capable of withstanding temperatures above 1,000°C. Nearly 58% of large enterprises integrate recycled-content insulation in commercial buildings to align with decarbonization targets. Adoption of prefabricated construction techniques has grown by 30%, increasing demand for factory-integrated acoustic panels. Rockwool International continues investing in low-carbon stone wool technology to reduce embodied carbon by 20%. Consumer behavior reflects regulatory-driven purchasing decisions, with developers prioritizing certified sustainable acoustic insulation solutions to comply with energy-performance directives.

How is rapid urbanization and industrial expansion reshaping procurement strategies?

Asia-Pacific holds approximately 26% of the global Acoustic Insulation Market volume and ranks as the fastest-growing region. China contributes nearly 45% of regional demand, followed by India at 20% and Japan at 15%. Urban housing projects exceeding 10 million new units annually in major economies significantly elevate demand for cost-efficient soundproofing systems. Industrial expansion and metro rail development projects require vibration-dampening insulation capable of reducing structural noise by 30%. Smart manufacturing hubs increasingly deploy lightweight foam-based acoustic materials to comply with workplace noise limits below 85 dB. Knauf Insulation has expanded production lines in Asia to strengthen regional supply chains. Consumer behavior reflects price sensitivity balanced with performance needs, particularly in high-density residential complexes and rapidly expanding industrial corridors.

What role do infrastructure modernization and energy investments play in shaping demand?

South America accounts for nearly 7% of the Acoustic Insulation Market, with Brazil representing approximately 55% of regional consumption and Argentina contributing close to 18%. Infrastructure modernization, including airport expansions and metro projects, has increased demand for high-performance acoustic panels capable of reducing ambient noise by 25–30%. The energy sector, particularly oil and gas processing facilities, integrates industrial-grade insulation to meet occupational exposure standards. Government-backed housing initiatives targeting over 1 million affordable housing units have boosted mineral wool and fiberglass installations. Regional manufacturers are focusing on localized production to reduce import dependency by 12%. Consumer behavior is strongly tied to public infrastructure spending cycles, with institutional buyers prioritizing cost-effective yet regulation-compliant insulation materials.

How are commercial megaprojects and industrial facilities influencing specification standards?

The Middle East & Africa region represents approximately 5% of the global Acoustic Insulation Market, with the UAE and Saudi Arabia accounting for over 50% of regional demand, followed by South Africa at nearly 20%. Large-scale commercial megaprojects and hospitality developments require advanced acoustic systems capable of reducing interior noise by up to 35%. Oil & gas processing facilities adopt high-temperature-resistant insulation materials exceeding 1,000°C thresholds. Technological modernization, including smart building integration, has increased specification of modular acoustic panels by 22%. Trade partnerships and local manufacturing incentives have strengthened regional supply chains. Consumer demand is largely project-driven, with developers prioritizing premium insulation systems for commercial real estate, aviation hubs, and mixed-use developments.

United States – 29% market share: The Acoustic Insulation Market in the United States is driven by high construction expenditure, strong retrofit activity, and strict building acoustic compliance standards across healthcare and residential sectors.

China – 22% market share: The Acoustic Insulation Market in China benefits from large-scale urban housing development, expanding industrial manufacturing capacity, and significant infrastructure investments supporting sustained material demand.

The Acoustic Insulation Market is moderately fragmented, with more than 120 active global and regional manufacturers competing across mineral wool, fiberglass, foam-based, and bio-based insulation segments. The top five companies collectively account for approximately 48% of total market share, indicating a competitive yet strategically concentrated environment. Leading players focus on product differentiation through fire-resistant materials exceeding 1,000°C tolerance, lightweight composites reducing installation weight by 25%, and hybrid thermal-acoustic systems delivering up to 30% enhanced performance compared to traditional insulation solutions.

Strategic initiatives between 2023 and 2025 include over 15 production capacity expansions globally, particularly in North America and Asia-Pacific, to address rising retrofit and infrastructure demand. Partnerships with modular construction firms have increased by 20%, enabling factory-integrated acoustic panels that shorten installation time by nearly 18%. Innovation trends emphasize low-carbon manufacturing, with several major producers targeting 30–40% reductions in embodied carbon by 2030. Digital transformation is reshaping the competitive landscape, as more than 35% of leading manufacturers now utilize AI-based acoustic modeling tools to optimize product performance and reduce material waste by 12–15%. Mergers and joint ventures remain selective, primarily aimed at strengthening regional distribution networks and enhancing sustainable product portfolios to meet evolving environmental regulations and industrial noise compliance standards.

Owens Corning

Saint-Gobain

Rockwool International

Knauf Insulation

Johns Manville

Paroc Group

Kingspan Group

BASF SE

Armacell International

Huntsman Corporation

Fletcher Insulation

URSA Insulation

GAF Materials Corporation

Nichiha Corporation

Recticel Group

Technological advancement in the Acoustic Insulation Market is centered on high-performance materials, digital integration, and sustainability-driven engineering. Mineral wool and fiberglass production lines are increasingly automated, with robotic fiberizing systems improving material consistency by up to 18% and reducing production waste by nearly 12%. Advanced binder technologies have lowered volatile organic compound (VOC) emissions by more than 30%, enabling compliance with strict indoor air quality standards across commercial buildings and healthcare facilities. High-density acoustic panels now achieve Sound Transmission Class (STC) ratings above 60, meeting premium specifications for multi-family residential and hospitality projects.

Emerging aerogel-based acoustic insulation is gaining traction in space-constrained environments, offering up to 50% thinner profiles while maintaining equivalent sound absorption performance compared to conventional mineral wool. Vacuum insulation panels (VIPs) integrated with acoustic layers are being deployed in high-rise developments to deliver combined thermal and noise control efficiency improvements exceeding 25%. In transportation applications, lightweight melamine foam and polyurethane composites reduce cabin noise by approximately 20–30% while lowering vehicle weight by nearly 15%, contributing to fuel efficiency gains.

Digital acoustic modeling software and Building Information Modeling (BIM) integration have transformed specification processes. Over 40% of large construction firms now use AI-driven simulation tools to predict decibel reduction outcomes with accuracy improvements of 22%, minimizing rework during installation. Smart acoustic panels equipped with embedded IoT sensors are also emerging, capable of monitoring ambient noise levels in real time and optimizing sound control performance dynamically. Additionally, circular manufacturing practices are enabling insulation products with up to 40% recycled content, aligning technology innovation with environmental performance targets and long-term sustainability commitments.

• In February 2024, Owens Corning announced the expansion of its mineral wool insulation manufacturing facility in the United States, increasing production capacity by approximately 20% to address growing demand from residential and commercial construction segments. The investment supports enhanced fire-resistant and acoustic product lines. Source: www.owenscorning.com

• In April 2024, Rockwool International inaugurated a new stone wool production line in Europe designed to improve energy efficiency by 15% and reduce CO₂ emissions intensity per ton produced. The facility strengthens supply capabilities for high-performance acoustic and fire-resistant insulation solutions. Source: www.rockwool.com

• In September 2024, Saint-Gobain completed the acquisition of a regional insulation manufacturer to expand its sustainable building solutions portfolio, reinforcing its presence in lightweight and recycled-content acoustic insulation products across key European markets. Source: www.saint-gobain.com

• In January 2025, Knauf Insulation introduced a next-generation glass mineral wool product manufactured using advanced binder technology that reduces embodied carbon by up to 25% while maintaining high sound absorption performance for commercial and industrial buildings. Source: www.knaufinsulation.com

The Acoustic Insulation Market Report provides a comprehensive analysis of material types, applications, end-user industries, technological advancements, and regional demand patterns shaping the global industry landscape. The report evaluates primary product categories including mineral wool, fiberglass, foam-based insulation, cellulose, aerogel composites, and hybrid thermal-acoustic materials, which collectively serve more than 80% of building-related soundproofing requirements. It assesses application segments across residential construction, commercial infrastructure, healthcare facilities, industrial manufacturing plants, transportation systems, and energy installations, where sound reduction performance ranging from 25 dB to over 60 dB is critical.

Geographically, the report covers five major regions—North America, Europe, Asia-Pacific, South America, and Middle East & Africa—analyzing infrastructure development trends, regulatory compliance frameworks, and regional consumption volumes. More than 45% of total installations are linked to retrofit projects, while new construction projects account for approximately 55% of demand. The scope further includes evaluation of digital integration such as AI-based acoustic modeling, modular construction compatibility, and IoT-enabled monitoring panels.

Additionally, the report reviews competitive positioning among over 100 active global manufacturers, production capacity expansions exceeding 15 facilities between 2023 and 2025, and sustainability initiatives targeting 25–40% recycled material integration. Niche segments such as marine insulation, aerospace acoustic damping systems, and high-temperature industrial enclosures are also assessed, providing decision-makers with a holistic perspective on operational, regulatory, and technological developments influencing strategic planning within the Acoustic Insulation Market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

17.2% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Owens Corning, Saint-Gobain, Rockwool International, Knauf Insulation, Johns Manville, Paroc Group, Kingspan Group, BASF SE, Armacell International, Huntsman Corporation, Fletcher Insulation, URSA Insulation, GAF Materials Corporation, Nichiha Corporation, Recticel Group |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |