Reports

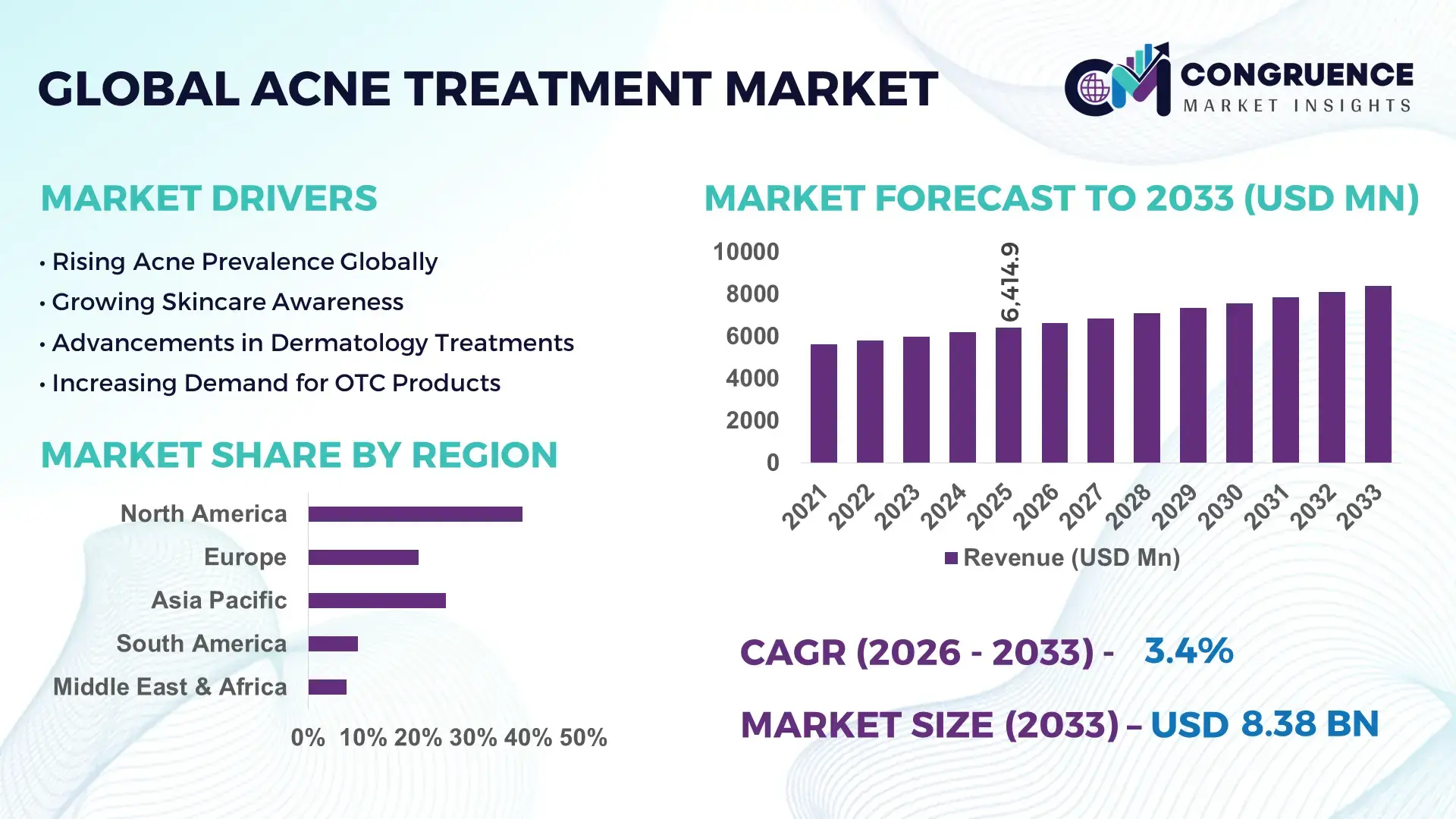

The Global Acne Treatment Market was valued at USD 6414.93 Million in 2025 and is anticipated to reach a value of USD 8382.17 Million by 2033 expanding at a CAGR of 3.4% between 2026 and 2033. Growth is being accelerated by rising prescription retinoid adoption, AI-enabled dermatology diagnostics, expanding teledermatology access, and higher spending on combination therapies targeting hormonal and adult acne segments.

The United States accounted for nearly 34% of global acne treatment demand in 2025, supported by strong dermatology infrastructure, over USD 1.2 billion in annual prescription dermatology spending, and rapid adoption of digital skin-analysis platforms across clinics and retail pharmacies. In comparison, South Korea expanded advanced topical treatment exports by 18%, driven by biotech manufacturing investments and high penetration of medicated skincare products. Ongoing pharmaceutical supply-chain diversification after Red Sea shipping disruptions further strengthened localized production strategies across North America and Asia-Pacific.

Companies prioritizing prescription innovation, localized manufacturing, and AI-driven personalized skincare platforms are securing stronger pricing power and long-term distribution advantages in the global acne treatment industry.

Market Size & Growth: Global acne treatment market reached USD 6414.93 million in 2025 and is projected at USD 8382.17 million by 2033, driven by AI-based dermatology tools and rising adult acne treatment demand.

Top Growth Drivers: Prescription retinoid demand increased 14%, teledermatology consultations expanded 22%, and medicated skincare penetration rose 17% globally in 2025.

Short-Term Forecast: By 2027, automated skin-analysis systems are expected to reduce patient diagnosis time by 28% and improve treatment personalization efficiency by 31%.

Emerging Technologies: AI imaging platforms, microbiome-based formulations, and light-therapy devices improved treatment adherence rates by over 20% across advanced dermatology clinics.

Regional Leaders: North America exceeded USD 2.4 billion with strong prescription adoption, Asia-Pacific crossed USD 1.9 billion through K-beauty expansion, and Europe approached USD 1.5 billion with premium dermaceutical growth.

Consumer/End-User Trends: Nearly 46% of urban consumers aged 18–35 shifted toward dermatologist-backed combination therapies and hormone-targeted acne management products.

Pilot/Case Example: In 2025, a digital dermatology network in Japan improved remote acne assessment accuracy by 33% using AI-enabled imaging integration.

Competitive Landscape: Leading companies controlled approximately 41% market share, with strong positioning from Galderma, Johnson & Johnson, Bausch Health, Sun Pharma, and L'Oréal.

Regulatory & ESG Impact: Sustainable packaging adoption reduced plastic usage by 19%, while stricter dermatology labeling standards improved consumer transparency across Europe and North America.

Investment & Funding: Global investments surpassed USD 850 million in 2025, led by biotech partnerships, advanced topical R&D, and regional manufacturing expansion strategies.

Innovation & Future Outlook: Next-generation microbiome therapies, smart wearable patches, and precision acne diagnostics are reshaping high-growth personalized skincare and pharmaceutical treatment models.

The acne treatment market is witnessing strong demand across prescription therapeutics, medicated skincare, and connected dermatology platforms as consumers increasingly seek faster and clinically validated solutions. Advanced microbiome-based products and AI-powered skin imaging systems improved treatment adherence by nearly 20% in urban healthcare networks during 2025–2026. Simultaneously, regional manufacturing expansion and stricter dermatology labeling regulations are reshaping product development priorities, creating a stronger foundation for strategic competitive positioning across global acne care portfolios.

The acne treatment market is becoming strategically important as pharmaceutical companies, dermatology platforms, and consumer health brands compete for high-frequency skincare spending and long-term patient retention. Digital dermatology adoption increased by 24% in 2025, while prescription combination therapies gained stronger traction among adult consumers aged 25–40. Supply-chain restructuring across India, South Korea, and the United States is also reshaping topical formulation manufacturing, reducing ingredient procurement lead times by nearly 18% after logistics disruptions linked to Red Sea shipping instability.

AI-enabled skin analysis systems are outperforming legacy visual assessment methods by improving diagnostic consistency by 31% and reducing consultation turnaround time by 27% across integrated dermatology networks. The United States continues to lead in prescription-based acne management and insurance-linked treatment access, whereas South Korea is advancing rapid innovation in microbiome-based formulations and high-volume dermaceutical exports. Over the next 2–3 years, smart skincare devices and personalized topical therapies are expected to expand across urban clinics, with connected treatment monitoring platforms improving adherence rates by over 20%.

In 2025, several dermatology chains integrated AI imaging with teleconsultation workflows to optimize patient triaging and reduce repeat clinical visits. Companies are increasing investments in localized production, biotech partnerships, and precision skincare portfolios to strengthen operational resilience and accelerate differentiated product deployment. Organizations securing faster diagnostic capability, integrated digital care ecosystems, and scalable formulation innovation are expected to gain stronger competitive positioning in the global acne treatment market.

Rising adoption of personalized acne therapies and digitally integrated dermatology services is accelerating structural transformation across the acne treatment market. Prescription combination treatments targeting hormonal and inflammatory acne recorded nearly 16% higher patient adherence rates in 2025, while AI-enabled skin diagnostic platforms improved treatment accuracy by 29% in urban dermatology networks. In the United States, teledermatology consultations expanded by 22% following broader insurance support for remote skin assessment services. Simultaneously, South Korean manufacturers increased exports of microbiome-based topical formulations by 18%, supported by advanced biotech manufacturing investments. These shifts are pushing pharmaceutical and skincare companies toward targeted R&D partnerships, AI integration, and direct-to-consumer dermatology ecosystems. Businesses prioritizing personalized treatment protocols and rapid formulation development are strengthening customer retention and improving long-term prescription conversion efficiency.

Supply dependency on pharmaceutical-grade active ingredients and formulation intermediates continues to pressure operational stability across the acne treatment industry. Global prices for key retinoid and benzoyl peroxide inputs fluctuated by nearly 14% during 2025 due to manufacturing concentration in China and freight cost volatility linked to maritime trade disruptions. Regulatory compliance costs for topical dermatology products also increased by approximately 11% across Europe following stricter ingredient transparency and labeling standards. These pressures are directly affecting profit margins for mid-sized skincare manufacturers and delaying product launches in high-demand retail channels. Companies are responding through localized sourcing agreements, regional manufacturing expansion in India, and long-term procurement contracts with specialty chemical suppliers. Firms with vertically integrated formulation capabilities are maintaining stronger pricing stability and faster product commercialization cycles.

Advanced dermatology technologies are creating high-value expansion opportunities across prescription skincare, connected devices, and precision topical formulations. AI-driven acne analysis platforms improved clinical workflow efficiency by 26% in 2025, while microbiome-focused therapies demonstrated over 21% higher effectiveness in recurring inflammatory acne management compared to conventional topical-only treatments. Japan and South Korea are rapidly commercializing smart skin-monitoring systems integrated with mobile health applications, accelerating adoption among digitally engaged consumers. Simultaneously, regulatory support for personalized dermatology innovation is encouraging biotech partnerships and specialized formulation development. Companies are expanding investments in wearable treatment patches, adaptive skincare algorithms, and direct-to-consumer digital care models to capture underserved adult acne segments. Early movers combining biotechnology, diagnostics, and telehealth integration are building stronger ecosystem control and premium treatment differentiation.

Long-term scalability remains a critical challenge as acne treatment providers integrate AI diagnostics, connected skincare devices, and personalized treatment platforms into fragmented healthcare systems. Nearly 32% of dermatology clinics in developing healthcare markets still lack interoperable digital imaging infrastructure, limiting standardized deployment of AI-supported acne assessment tools. Data privacy compliance costs for cloud-based patient imaging systems increased by 13% in 2025 following tighter digital health regulations across the European Union and parts of Asia. Workforce limitations are also emerging, with trained dermatology specialists remaining concentrated in large metropolitan centers despite rising teleconsultation demand. Companies must expand cybersecurity investments, clinician training programs, and interoperable digital platforms to ensure consistent deployment quality. Organizations solving infrastructure integration and scalable digital workflow management will secure stronger operational resilience and sustainable competitive advantage.

AI-Integrated Skin Diagnostics Expansion AI-enabled acne assessment systems recorded 27% higher deployment across dermatology networks during 2025 as clinics in the United States and Japan integrated automated lesion mapping into teleconsultation workflows. Diagnostic turnaround time declined by 30%, while repeat consultation volumes fell by 18% through predictive treatment monitoring. Companies are scaling partnerships with imaging software firms and cloud-health providers to standardize remote dermatology operations and improve patient throughput amid specialist shortages.

Localized Manufacturing Network Restructuring Pharmaceutical and skincare companies are shifting active ingredient sourcing toward India and South Korea after shipping disruptions increased international formulation lead times by nearly 16% in 2025. Regional contract manufacturing deployments expanded by 21%, improving inventory stability and reducing packaging turnaround cycles. A non-obvious operational shift is the increased use of dual-supplier procurement strategies for retinoids and topical antibiotics, allowing companies to reduce stockout exposure while maintaining regulatory compliance efficiency.

Microbiome Therapy Commercialization Surge Advanced microbiome-based acne formulations gained 19% higher prescription adoption in premium dermatology clinics due to improved inflammatory acne response rates and lower irritation levels compared to conventional topical regimens. South Korean biotech firms accelerated commercialization through clinical partnerships and rapid formulation testing platforms. Companies are restructuring R&D investments toward barrier-repair ingredients and adaptive skincare systems that support long-duration treatment adherence and lower product discontinuation rates.

Homecare Device Penetration Rising Light therapy and connected skincare devices expanded by 24% across urban homecare settings as consumers prioritized lower clinic dependency and personalized treatment monitoring. Smart wearable patches and app-linked LED systems improved treatment consistency by 22% through automated usage tracking. Regulatory tightening around oral antibiotic overuse in parts of Europe also accelerated demand for non-invasive alternatives, pushing device manufacturers to expand pharmacy partnerships and subscription-based skincare ecosystems.

Topical Medications remained the dominant segment in 2025 due to broad prescription scalability, lower treatment costs, and strong integration into both retail pharmacy and teledermatology workflows. More than 48% of acne treatment prescriptions globally continued to rely on retinoid-based creams, gels, and combination topical formulations because of faster deployment across mild-to-moderate acne management programs. Companies are expanding microbiome-friendly and low-irritation topical portfolios to improve patient adherence rates, which increased by nearly 17% in digitally monitored dermatology programs. Chemical Peels and Laser Therapy maintained strategic relevance in premium cosmetic clinics, particularly in South Korea and the United States, where procedural acne care expanded with higher consumer spending on aesthetic dermatology.

Light Therapy emerged as the fastest-growing type as connected homecare devices and clinic-based LED systems gained stronger adoption among consumers seeking non-antibiotic treatment pathways. Device-assisted acne management improved treatment consistency by 21% compared to manual topical-only routines. Oral Medications retained importance for severe inflammatory acne but faced tighter prescribing oversight due to concerns around long-duration antibiotic exposure. Companies are prioritizing hybrid treatment ecosystems combining topical therapeutics, connected skincare devices, and procedural dermatology partnerships to diversify treatment outcomes and strengthen recurring patient engagement.

Acne Vulgaris remained the leading application segment due to its high diagnosis frequency, recurring treatment cycles, and extensive integration across retail dermatology and prescription skincare channels. Nearly 61% of dermatology consultations for acne-related conditions in 2025 were associated with acne vulgaris management, particularly among consumers aged 15–30. Companies are scaling combination treatment protocols and AI-assisted diagnostic systems to streamline patient stratification and reduce treatment switching rates. Severe Acne treatments retained strong clinical importance within hospital-linked dermatology programs, where oral therapies and advanced procedural interventions continued to support complex inflammatory cases requiring long-duration supervision.

Hormonal Acne emerged as the fastest-growing application as adult female treatment demand expanded through teledermatology platforms and hormone-targeted skincare regimens. Prescription personalization rates for hormonal acne management increased by 23% across digitally connected dermatology clinics in the United States and South Korea. Scar Treatment applications also gained momentum through laser-assisted resurfacing and collagen-stimulation technologies integrated into cosmetic dermatology workflows. Blackhead and Whitehead Treatment segments remained operationally important in pharmacy-led skincare programs, especially within high-volume over-the-counter product categories. Companies are increasing investments in personalized treatment mapping and long-term skincare subscription ecosystems to improve retention across recurring acne management pathways.

Dermatology Clinics accounted for the dominant end-user share due to specialized treatment infrastructure, integrated diagnostic capability, and high patient throughput for both prescription and procedural acne management. Nearly 46% of advanced acne interventions in 2025 were delivered through dermatology clinic networks using combination therapy protocols and AI-assisted imaging systems. Clinics in the United States and South Korea increased deployment of digital consultation platforms by approximately 24% to improve patient monitoring efficiency and reduce follow-up scheduling delays. Hospitals maintained strategic importance for severe inflammatory acne cases requiring oral medication supervision and multidisciplinary dermatology support. Cosmetic Clinics also expanded procedural treatment offerings through laser resurfacing and chemical peel integration targeting post-acne scarring management.

Online Pharmacies emerged as the fastest-growing end-user segment as consumers increasingly shifted toward digitally fulfilled prescription skincare and subscription-based acne treatment programs. Online acne treatment order volumes increased by nearly 28% during 2025 due to faster prescription processing and integrated teleconsultation workflows. Homecare Settings gained additional traction through connected light-therapy devices and app-enabled treatment tracking systems. Pharmacies remained central to over-the-counter topical medication distribution, especially in India and Southeast Asia where retail accessibility continues to influence treatment adoption. Companies are strengthening ecosystem partnerships across clinics, digital pharmacies, and homecare technology providers to secure recurring treatment engagement and omnichannel distribution advantages.

North America accounted for the largest market share at 36.8% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 4.6% between 2026 and 2033.

Digital Dermatology Integration Accelerating Clinical Efficiency

North America maintained leadership in the acne treatment market through advanced dermatology infrastructure, high prescription therapy penetration, and rapid deployment of AI-enabled diagnostic platforms. The region represented nearly 37% of global treatment demand in 2025, supported by strong teledermatology utilization and broad insurance-linked dermatology access. More than 42% of large dermatology networks in the United States integrated automated skin imaging systems to improve patient triaging and reduce consultation delays. Pharmaceutical companies are strengthening local manufacturing agreements and expanding microbiome-based topical product portfolios to reduce dependency on imported formulation intermediates. Growing collaboration between digital health providers and dermatology clinics is also improving recurring patient management efficiency across urban healthcare systems.

United States Market Outlook: The United States remains the operational center of the regional acne treatment industry due to strong pharmaceutical innovation capacity, large-scale dermatology clinic networks, and high digital health adoption. Over 24% of acne-related consultations in 2025 were conducted through teledermatology platforms integrated with AI-assisted imaging tools. Companies are prioritizing direct-to-consumer prescription ecosystems, connected skincare monitoring, and localized formulation manufacturing to improve treatment continuity and shorten supply-chain turnaround cycles.

Regulatory Modernization Reshaping Product Positioning

Europe continues to strengthen its acne treatment ecosystem through stricter dermatology regulations, sustainable formulation development, and expansion of premium skincare therapeutics. The region accounted for approximately 27% of global market deployment in 2025, with Germany, France, and the United Kingdom leading prescription dermatology adoption. More than 19% of skincare manufacturers across the region reformulated acne products to comply with tighter ingredient transparency and environmental packaging standards. Companies are increasing investments in recyclable packaging systems, microbiome-friendly formulations, and pharmacy-linked digital skincare services to strengthen compliance efficiency and premium product differentiation. Cross-border distribution modernization is also improving product availability across specialized dermatology retail channels.

Germany Market Outlook: Germany remains a strategic manufacturing and dermatology innovation hub due to strong pharmaceutical production infrastructure and advanced regulatory integration. In 2025, nearly 31% of premium prescription acne therapies distributed across Central Europe originated from German pharmaceutical and dermaceutical facilities. Companies are expanding automated formulation plants and digital pharmacy collaborations to accelerate treatment accessibility while maintaining high compliance standards across topical and oral acne therapy categories.

Manufacturing Scale and Digital Adoption Expanding Rapidly

Asia-Pacific is emerging as the fastest-evolving acne treatment market due to large-scale pharmaceutical manufacturing, rising digital skincare adoption, and expanding middle-income consumer spending. The region contributed nearly 29% of global acne treatment deployment in 2025, while exports of medicated skincare formulations from South Korea and India increased by approximately 21%. China, Japan, and South Korea are accelerating integration of AI-based skin diagnostics into cosmetic dermatology workflows to improve treatment precision and patient retention. Companies are scaling localized production facilities and contract manufacturing partnerships to reduce sourcing risks and improve inventory responsiveness following supply-chain disruptions affecting international ingredient movement.

South Korea Market Outlook: South Korea continues to lead innovation in advanced acne skincare through high-volume dermaceutical manufacturing and rapid commercialization of microbiome-based treatments. More than 38% of premium acne treatment exports from the country in 2025 were linked to personalized skincare and connected beauty technology ecosystems. Domestic companies are increasing investments in AI-supported skin analysis platforms, adaptive topical formulations, and international clinic partnerships to strengthen export competitiveness and accelerate premium treatment positioning.

Urban Dermatology Demand Strengthening Retail Expansion

South America is experiencing steady acne treatment expansion through rising urban dermatology awareness, growing pharmacy distribution networks, and increasing cosmetic procedure adoption. Brazil and Argentina accounted for the majority of regional deployment activity in 2025, supported by expanding access to prescription skincare and clinic-based acne scar therapies. Retail pharmacy-led acne product distribution increased by nearly 18% across metropolitan areas, while private dermatology networks expanded teleconsultation services to improve treatment accessibility. Companies are balancing growth opportunities with infrastructure limitations by strengthening local distribution partnerships and regional packaging operations to reduce import dependency and improve product availability consistency.

Brazil Market Outlook: Brazil remains the largest operational market in South America due to strong cosmetic dermatology demand and widespread retail pharmacy penetration. In 2025, nearly 34% of acne-related aesthetic procedures in Latin America were performed in Brazilian cosmetic clinics and dermatology centers. Companies are prioritizing localized packaging facilities, pharmacy partnerships, and affordable combination therapy portfolios to improve market reach across both premium and mid-tier consumer segments.

Healthcare Modernization Supporting Specialized Dermatology Expansion

The Middle East & Africa acne treatment market is advancing through healthcare infrastructure modernization, expanding private dermatology networks, and growing investment in specialized skincare services. Gulf countries represented the highest deployment concentration in 2025, supported by rising adoption of premium dermatology treatments and digitally connected clinic ecosystems. More than 16% of private skincare clinics across the United Arab Emirates integrated AI-assisted skin assessment tools to improve consultation speed and treatment planning efficiency. Companies are strengthening regional distribution partnerships and localized warehousing operations to improve inventory reliability and reduce international shipping dependency affecting pharmaceutical skincare supply chains.

United Arab Emirates Market Outlook: The United Arab Emirates continues to strengthen its position as a premium dermatology and cosmetic treatment hub through advanced clinic infrastructure and rapid digital health integration. In 2025, approximately 27% of specialized dermatology centers in Dubai expanded connected skincare consultation services linked with AI-supported treatment monitoring systems. Companies are investing in high-end dermatology facilities, international pharmaceutical collaborations, and medical tourism-focused skincare programs to improve regional treatment accessibility and premium service positioning.

The acne treatment market is led by global pharmaceutical companies including Galderma, Johnson & Johnson, Bausch Health, Sun Pharma, and L'Oréal, competing directly against regional dermaceutical manufacturers and digital dermatology platforms. The top five players collectively controlled nearly 41% of market activity in 2025 through prescription therapies, premium skincare portfolios, and integrated distribution networks. Competition is centered on formulation efficiency, treatment personalization, supply-chain resilience, and speed-to-commercialization. AI-enabled diagnostic integration improved patient retention rates by 22%, while localized manufacturing strategies reduced product replenishment delays by nearly 18% after international shipping disruptions. Companies are strengthening vertical integration through biotech partnerships, teledermatology collaborations, and microbiome-focused product development. Premium players are competing on clinical performance and digital ecosystem control, whereas regional manufacturers are leveraging lower-cost production and retail pharmacy penetration. Regulatory compliance, ingredient sourcing stability, and advanced dermatology infrastructure remain major entry barriers. Winning requires scalable innovation, localized supply control, and digitally integrated treatment ecosystems.

Galderma

Johnson & Johnson

Bausch Health Companies Inc.

Sun Pharmaceutical Industries Ltd.

L'Oréal

Pfizer Inc.

AbbVie Inc.

Almirall S.A.

Teva Pharmaceutical Industries Ltd.

GlaxoSmithKline plc

Reckitt Benckiser Group plc

Cipla Limited

Viatris Inc.

La Roche-Posay

AI-enabled dermatology platforms, automated lesion mapping, and connected teledermatology systems are transforming acne treatment workflows across hospitals and specialty clinics. In 2025, nearly 34% of advanced dermatology networks integrated AI-supported skin analysis tools, improving diagnostic consistency by 31% and reducing consultation turnaround time by 27% compared to conventional visual-only assessments. Companies are integrating imaging analytics with prescription management systems to improve treatment adherence, reduce repeat visits, and optimize clinician workload allocation across high-volume dermatology operations.

Emerging technologies including microbiome-based formulations, smart LED therapy devices, and adaptive topical delivery systems are reshaping personalized acne management. Connected light-therapy platforms improved home-treatment compliance by 22%, while microbiome-focused topical therapies demonstrated nearly 19% higher inflammatory acne response rates than legacy benzoyl peroxide-only regimens. South Korean and Japanese skincare manufacturers are expanding partnerships with biotechnology firms and digital health providers to accelerate precision skincare commercialization and strengthen premium treatment positioning.

Between 2026 and 2028, wearable skin-monitoring patches, predictive treatment algorithms, and digitally connected pharmacy ecosystems will become major competitive differentiators. Companies controlling AI diagnostics, localized formulation manufacturing, and integrated digital care platforms are expected to reduce product deployment delays by nearly 18% while strengthening long-term patient retention and operational scalability.

March 2026 – Galderma reported strong expansion in therapeutic dermatology operations, with Therapeutic Dermatology product growth exceeding 50.2% during 2025 through innovation-driven portfolio scaling and international launch expansion. The development strengthened Galderma’s competitive positioning across prescription dermatology and integrated skincare ecosystems. Source: galderma.com

October 2025 – Galderma accelerated global dermatological skincare deployment, achieving 15.0% year-on-year operational growth across key product categories and expanding innovation-led treatment launches in 17 international markets. The expansion improved commercial scale, international distribution efficiency, and premium dermatology market penetration. Source: investors. investors.galderma.com

May 2024 – L'Oréal advanced bioprinted artificial skin technology capable of replicating acne-related skin conditions while reducing laboratory development cycles from 21–35 days to nearly 18 days. The innovation strengthened dermatology testing efficiency, personalized skincare research capability, and alternative cosmetic validation infrastructure. Source: nypost.com

June 2024 – Researchers from Nanyang Technological University and collaborating institutions introduced physics-based controllable facial blemish simulation technology improving gradual acne recovery visualization accuracy through melanin and hemoglobin modeling integration. The advancement enhanced digital dermatology imaging realism and strengthened AI-assisted skincare analysis applications. Source:arxiv.org

The Acne Treatment Market report provides detailed analysis across treatment types, applications, end-users, competitive positioning, and regional deployment dynamics between 2026 and 2033. The study covers Topical Medications, Oral Medications, Laser Therapy, Chemical Peels, and Light Therapy while evaluating demand across Acne Vulgaris, Hormonal Acne, Severe Acne, Scar Treatment, and Blackhead and Whitehead Treatment applications. More than 45% of treatment deployment continues to concentrate within dermatology clinic networks and digitally integrated prescription skincare ecosystems.

The report evaluates operational trends across North America, Europe, Asia-Pacific, South America, and Middle East & Africa, highlighting manufacturing concentration, digital dermatology adoption, AI-enabled diagnostics, microbiome-based formulations, and connected skincare technologies. It also examines enterprise expansion strategies, localized manufacturing shifts, teledermatology integration, and competitive differentiation through personalized treatment platforms. Strategic insights support investment planning, distribution optimization, product innovation, partnership development, and long-term competitive positioning within the evolving global acne treatment industry.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 6414.93 Million |

|

Market Revenue in 2033 |

USD 8382.17 Million |

|

CAGR (2026 - 2033) |

3.4% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Galderma, Johnson & Johnson, Bausch Health Companies Inc., Sun Pharmaceutical Industries Ltd., L'Oréal, Pfizer Inc., AbbVie Inc., Almirall S.A., Teva Pharmaceutical Industries Ltd., GlaxoSmithKline plc, Reckitt Benckiser Group plc, Cipla Limited, Viatris Inc., La Roche-Posay |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |