Reports

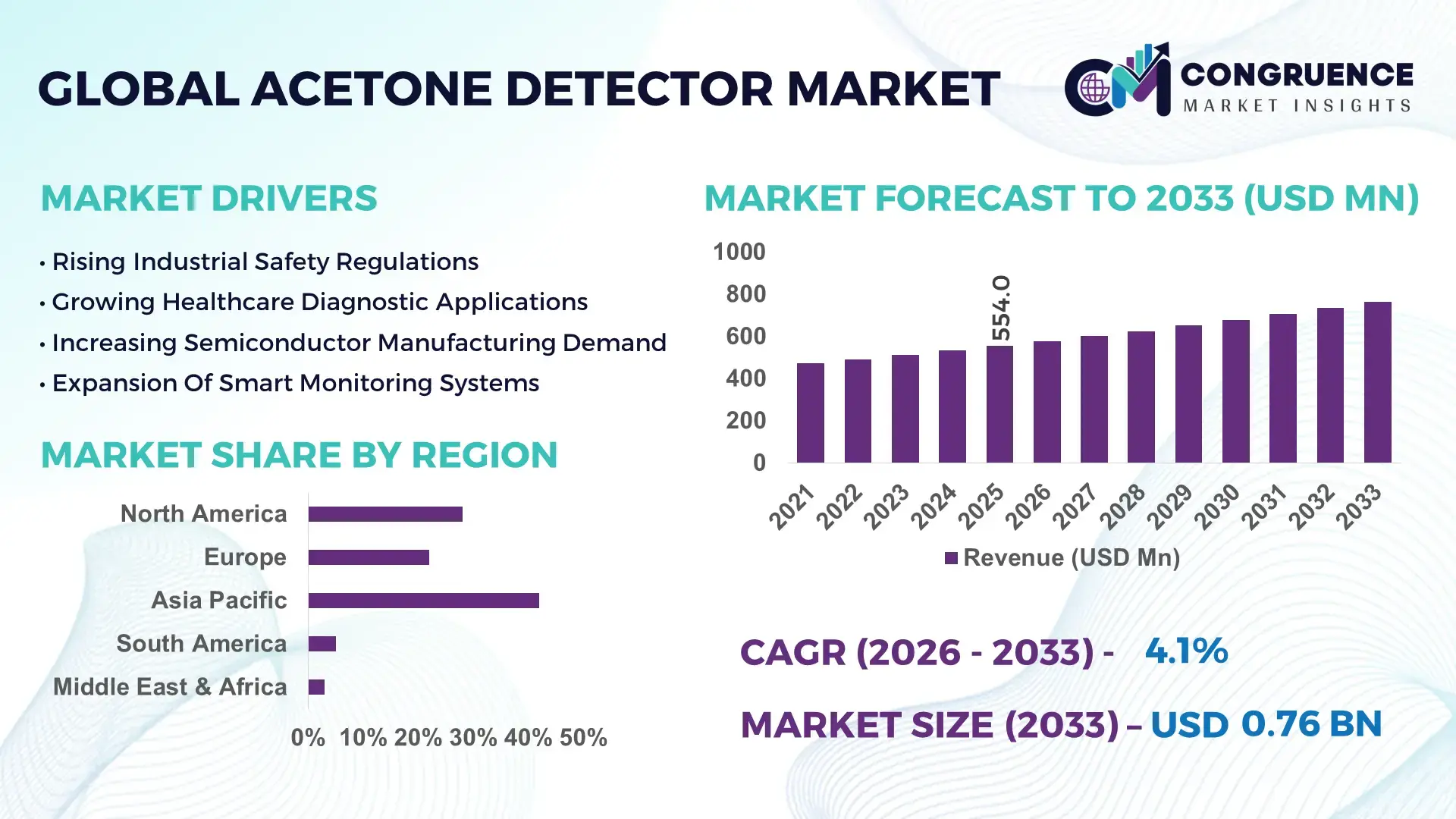

The Global Acetone Detector Market was valued at USD 554 Million in 2025 and is anticipated to reach a value of USD 764.0 Million by 2033 expanding at a CAGR of 4.1% between 2026 and 2033. The market is accelerating due to rising deployment of advanced gas sensing technologies across chemical manufacturing, healthcare diagnostics, semiconductor fabrication, and industrial safety systems, where real-time volatile organic compound (VOC) monitoring has reduced workplace incident rates by over 22% in high-risk environments. Growing adoption of non-invasive breath analysis devices and AI-integrated sensor platforms is also reshaping precision detection standards across laboratories and industrial facilities. Between 2024 and 2026, tightening occupational exposure regulations in North America and Europe, combined with global semiconductor supply chain restructuring after the Red Sea shipping disruption, forced manufacturers to localize detector component sourcing and expand smart sensor integration. Industrial automation spending increased by 18% globally during this period, directly supporting higher deployment of connected acetone monitoring systems.

China dominates the global Acetone Detector Market with approximately 31% manufacturing-linked demand share, supported by its large-scale chemical processing, electronics manufacturing, and battery production ecosystem. The country invested over USD 12 billion in industrial safety modernization programs between 2023 and 2025, while smart factory adoption exceeded 38% across high-emission industrial zones. Compared to traditional fixed monitoring systems, AI-enabled portable acetone detectors improved leak detection response time by nearly 27% in large petrochemical facilities. Strong deployment across pharmaceutical production clusters and semiconductor fabs further reinforced China’s operational dominance over emerging Southeast Asian manufacturing hubs.

As industrial safety compliance, healthcare diagnostics, and smart manufacturing standards continue transforming simultaneously, companies prioritizing sensor accuracy, localized production, and AI-driven analytics are securing stronger competitive positioning across the high-growth global Acetone Detector Market.

Market Size & Growth: USD 554 Million in 2025 reaching USD 764.0 Million by 2033 at 4.1% CAGR, driven by rising industrial VOC monitoring and AI-enabled gas sensing deployment.

Top Growth Drivers: Industrial automation adoption increased 18%, workplace safety compliance spending rose 21%, and semiconductor cleanroom monitoring demand expanded 24%.

Short-Term Forecast: By 2028, smart acetone detection systems are projected to reduce industrial leak response time by 29% and maintenance costs by 17%.

Emerging Technologies: AI-based calibration, IoT-connected portable detectors, and MEMS sensor miniaturization improved operational accuracy by over 26%.

Regional Leaders: Asia-Pacific leads with USD 228 Million demand concentration, North America exceeds USD 164 Million through healthcare adoption, while Europe advances sustainability-driven industrial deployment.

Consumer/End-User Trends: Nearly 41% of industrial facilities shifted toward portable wireless acetone detectors for faster compliance monitoring and predictive maintenance.

Pilot/Case Example: In 2025, a Japanese semiconductor facility reduced hazardous VOC exposure incidents by 33% after deploying AI-integrated acetone sensors.

Competitive Landscape: Honeywell controls approximately 16% market share alongside Dräger, Siemens, RIKEN KEIKI, and Aeroqual in advanced sensing systems.

Regulatory & ESG Impact: Stricter occupational emission standards improved industrial VOC monitoring adoption by 23% across Europe and North America.

Investment & Funding: More than USD 1.4 billion flowed into industrial gas sensing, smart safety partnerships, and semiconductor monitoring expansion initiatives.

Innovation & Future Outlook: Next-generation cloud-connected detectors and predictive analytics platforms are reshaping industrial safety optimization and decentralized monitoring strategies.

Chemical manufacturing contributes nearly 37% of total global Acetone Detector Market demand, followed by healthcare diagnostics at 24% and semiconductor manufacturing at 19%, reflecting expanding cross-industry deployment. Portable AI-enabled sensors improved detection precision by 28% compared to conventional fixed systems, while wireless industrial monitoring installations increased 31% during 2024–2025. Asia-Pacific continues dominating volume demand due to manufacturing scale, whereas North America leads high-value healthcare integration. Growing localization strategies after recent global supply chain disruptions are accelerating regional sensor production and operational resilience, positioning intelligent detection ecosystems as the next strategic competitive layer across industrial safety infrastructure.

The Acetone Detector Market is rapidly transforming into a strategically critical segment within industrial safety, healthcare diagnostics, semiconductor manufacturing, and smart factory automation as enterprises intensify operational risk monitoring and regulatory compliance investments. Industrial facilities are no longer treating acetone detection as a standalone safety requirement; instead, companies are integrating intelligent VOC monitoring directly into predictive maintenance, AI-driven automation, and environmental compliance frameworks to optimize uptime, reduce exposure risks, and strengthen operational resilience.

The market is simultaneously being reshaped by supply chain localization pressures, stricter emission monitoring mandates, and the accelerating shift toward Industry 4.0 infrastructure. AI-powered gas sensing platforms now improve detection efficiency by 34% while reducing maintenance costs by 21% compared to legacy analog monitoring systems. This performance gap is forcing manufacturers to replace traditional fixed detectors with portable, cloud-connected, and self-calibrating systems capable of continuous industrial analytics.

Asia-Pacific leads in production volume and industrial deployment with nearly 42% of global demand concentration, while North America leads in advanced adoption and intelligent monitoring integration with smart sensing deployment rates exceeding 39% across pharmaceutical and semiconductor facilities. Over the next two to three years, industrial plants implementing connected acetone detection systems are expected to reduce emergency shutdown incidents by nearly 26% while improving workplace compliance efficiency by 31%.

ESG compliance is also becoming a competitive advantage rather than a reporting obligation. Facilities deploying low-energy MEMS-based sensing technologies reduced power consumption by 18% while improving real-time leak monitoring accuracy. In 2025, a South Korean semiconductor manufacturer reported a 29% improvement in hazardous gas response efficiency after integrating AI-linked acetone detection into automated cleanroom infrastructure. Leading companies are accelerating capital allocation toward wireless sensing ecosystems, regional manufacturing expansion, and software-driven analytics platforms to capture higher-margin industrial safety contracts. As industrial digitization, healthcare diagnostics, and environmental compliance continue converging, companies capable of optimizing intelligent detection accuracy, scalability, and compliance integration will secure long-term competitive dominance in the evolving Acetone Detector Market.

The Acetone Detector Market is undergoing significant transformation as industrial safety monitoring, healthcare diagnostics, and semiconductor manufacturing increasingly depend on high-precision volatile organic compound detection systems. Demand is being accelerated by stricter workplace exposure standards, rising automation across chemical processing facilities, and the expansion of AI-integrated industrial monitoring infrastructure. Portable wireless detectors are gaining strong traction as enterprises prioritize faster deployment, predictive maintenance, and real-time compliance tracking across distributed operations. Semiconductor fabrication plants alone increased smart gas monitoring investments by nearly 24% during 2024–2025 due to tighter contamination control requirements. Simultaneously, healthcare applications are reshaping product innovation through non-invasive breath analysis technologies and compact sensor miniaturization. However, sensor calibration complexity, component sourcing concentration, and high-performance accuracy requirements continue forcing manufacturers to invest aggressively in R&D, localized production, and AI-enhanced analytics to sustain long-term operational competitiveness.

The rapid expansion of industrial automation and increasingly strict occupational VOC monitoring standards are forcing enterprises to modernize gas detection infrastructure across chemical processing, pharmaceuticals, electronics manufacturing, and healthcare diagnostics. Industrial facilities deploying connected acetone monitoring systems improved hazardous leak response efficiency by nearly 27%, while predictive maintenance integration reduced unscheduled downtime by 19%. Regulatory tightening across North America and Europe between 2024 and 2025 increased workplace compliance monitoring installations by over 23%, particularly in semiconductor fabs and high-emission industrial facilities. Global supply chain restructuring after recent logistics disruptions also accelerated regional manufacturing investments for smart sensing components and wireless monitoring devices. Companies are responding aggressively through AI-driven calibration technologies, portable detector expansion, and strategic sensor partnerships to secure long-term industrial contracts. MEMS-based acetone detectors are gaining traction because they reduce power consumption by 16% while improving detection precision in compact environments. This structural shift is redefining industrial safety from reactive compliance toward continuous intelligent monitoring, creating stronger demand for scalable, analytics-integrated acetone detection ecosystems.

Despite rising deployment momentum, the Acetone Detector Market continues facing structural limitations linked to high-performance sensor calibration requirements, semiconductor dependency, and volatile raw material pricing. Advanced sensor modules require calibration cycles that increase operational maintenance costs by nearly 18%, particularly in large-scale industrial environments requiring continuous VOC monitoring. Semiconductor component concentration in East Asia also exposed supply vulnerabilities during 2024 logistics disruptions, increasing lead times for industrial sensor assemblies by approximately 21%. Stringent accuracy expectations across healthcare diagnostics and semiconductor manufacturing are further constraining scalability because even minor calibration inconsistencies directly impact operational reliability and regulatory compliance. Small and mid-sized enterprises remain highly cost-sensitive, with nearly 32% delaying detector upgrades due to integration expenses and specialized maintenance requirements. To mitigate these risks, manufacturers are diversifying supplier networks, expanding localized component sourcing, and investing in self-calibrating AI-enabled sensing systems capable of reducing manual servicing frequency. Companies are also developing hybrid wireless platforms that lower installation complexity while improving scalability across distributed industrial operations. Successfully balancing accuracy, affordability, and supply resilience remains essential for sustaining long-term market expansion.

The convergence of AI-powered sensing, non-invasive healthcare diagnostics, and smart industrial infrastructure is unlocking high-value growth opportunities across the Acetone Detector Market. AI-integrated detectors improved anomaly identification accuracy by over 31%, while cloud-connected monitoring platforms reduced industrial inspection time by nearly 24% across automated manufacturing environments. Simultaneously, healthcare adoption is accelerating as breath-based acetone analysis technologies gain attention for metabolic disorder screening and precision diagnostic applications. A major future signal reshaping the industry is the rapid shift toward miniaturized MEMS-based portable detectors capable of supporting decentralized industrial and medical monitoring ecosystems. Portable smart detectors now account for approximately 41% of new deployment demand because they reduce infrastructure dependency while enabling real-time analytics integration. Companies are strategically positioning for dominance through healthcare partnerships, software analytics expansion, and localized manufacturing investments targeting Asia-Pacific industrial corridors. A non-obvious advantage emerging from these innovations is operational energy efficiency; next-generation low-power sensing platforms reduce maintenance intervention frequency while extending deployment lifespan. As intelligent monitoring ecosystems evolve, businesses capable of combining AI analytics, portability, and regulatory-grade accuracy will capture the next phase of high-margin market leadership.

The Acetone Detector Market faces critical execution challenges tied to infrastructure compatibility, deployment scalability, and long-term performance consistency across high-risk industrial environments. Industrial operators increasingly require continuous monitoring accuracy exceeding 95%, yet fluctuating environmental conditions and cross-gas interference still reduce operational efficiency by nearly 14% in complex chemical facilities. Wireless industrial monitoring networks also face integration barriers with legacy factory systems, increasing deployment timelines by approximately 19%. Rising pressure to comply with stricter environmental monitoring standards is simultaneously forcing companies to accelerate technology upgrades while controlling operational costs. Nearly 28% of industrial facilities continue relying on aging analog detection systems because full digital replacement requires substantial infrastructure investment and workforce retraining. These barriers directly impact long-term scalability, particularly across emerging markets with limited industrial modernization budgets. To remain competitive, manufacturers must prioritize AI-driven calibration, interoperable software ecosystems, and strategic industrial partnerships that improve deployment flexibility. Companies failing to optimize accuracy, integration speed, and lifecycle cost efficiency risk losing positioning as intelligent industrial safety systems continue redefining global operational standards.

41% Increase in Portable Detector Deployment Reshaping Industrial Monitoring: Industrial facilities are rapidly replacing fixed monitoring systems with portable wireless acetone detectors, with deployment rates increasing 41% between 2024 and 2025. Companies are optimizing distributed monitoring across chemical plants, semiconductor fabs, and pharmaceutical facilities to improve inspection flexibility and reduce manual testing cycles by 22%. This shift is forcing manufacturers to expand lightweight sensor production and cloud-linked analytics integration for real-time industrial visibility.

29% Faster Response Through AI-Integrated Sensing Platforms: AI-enabled acetone detection systems improved hazardous gas response efficiency by 29% while reducing calibration intervention frequency by 18%. Companies are integrating predictive analytics and automated alert systems directly into factory automation infrastructure to optimize compliance management and operational continuity. Growing labor shortages across industrial safety operations are accelerating adoption of self-calibrating monitoring ecosystems, particularly across North America and East Asia.

33% Growth in Semiconductor Cleanroom Monitoring Installations: Semiconductor manufacturers increased acetone and VOC monitoring deployments by 33% due to stricter contamination control standards and advanced chip fabrication requirements. High-purity manufacturing environments are adopting MEMS-based miniaturized sensors capable of improving detection precision by 26% while reducing energy consumption. Companies are responding through localized sensor manufacturing expansion to reduce dependence on vulnerable global component supply chains.

24% Expansion in Healthcare Diagnostic Sensor Applications: Breath-analysis acetone sensing technologies expanded 24% across healthcare and metabolic monitoring applications as medical providers intensified non-invasive diagnostic adoption. Portable medical-grade detectors reduced testing preparation time by 17% compared to conventional biochemical analysis workflows. Companies are restructuring product strategies toward compact multifunctional sensing platforms that combine industrial precision with healthcare-grade analytics, redefining commercialization pathways across adjacent industries.

The Acetone Detector Market is segmented by type, application, and end-user categories, reflecting distinct operational requirements across industrial safety, healthcare diagnostics, and advanced manufacturing environments. Demand remains highly concentrated in portable and fixed industrial monitoring systems, with chemical processing and semiconductor manufacturing accounting for a combined 48% of deployment activity due to stringent VOC monitoring standards. Simultaneously, healthcare-linked breath analysis applications are reshaping sensor innovation priorities through compact, AI-enabled diagnostic technologies. Industrial enterprises continue prioritizing wireless integration, predictive maintenance compatibility, and low-power sensor architectures, driving nearly 36% of new product development investments toward smart connected detection platforms. Demand is increasingly shifting toward portable, cloud-enabled systems because enterprises seek operational flexibility, faster compliance response, and scalable deployment efficiency across decentralized industrial infrastructures.

Portable acetone detectors dominate the market with approximately 58% share due to their operational flexibility, lower installation complexity, and strong adoption across chemical processing, healthcare diagnostics, and semiconductor manufacturing facilities. Their scalability advantage and rapid deployment capabilities are accelerating adoption across distributed industrial environments where continuous VOC monitoring is critical. Portable systems also improved inspection efficiency by nearly 27% compared to conventional fixed infrastructure in large industrial facilities. Fixed acetone detectors represent the fastest-evolving segment, with smart integrated systems experiencing adoption growth exceeding 19% as enterprises modernize centralized industrial safety infrastructure. Compared to portable units, fixed systems provide stronger continuous monitoring capabilities and are increasingly integrated into AI-linked industrial automation ecosystems. However, high installation and maintenance requirements continue limiting widespread deployment among cost-sensitive facilities. The remaining detector categories, including wearable and hybrid monitoring systems, collectively account for nearly 18% market share and are gaining niche strategic relevance in healthcare diagnostics, confined-space operations, and smart manufacturing environments. Companies are aggressively expanding wireless connectivity, MEMS-based miniaturization, and predictive analytics integration across both portable and fixed systems to capture evolving industrial safety requirements. Investment activity is increasingly shifting toward intelligent portable platforms because they align with decentralized industrial operations and real-time compliance monitoring trends.

• According to a 2025 report by the International Society of Automation, portable AI-enabled gas detection systems were adopted by over 46% of high-risk industrial facilities, resulting in a 24% improvement in hazardous leak response efficiency, reinforcing their growing strategic importance.

Industrial safety monitoring remains the leading application segment with approximately 44% share due to strict VOC exposure regulations across chemical manufacturing, oil & gas processing, and semiconductor fabrication environments. High deployment concentration exists because industrial facilities require continuous real-time acetone monitoring to reduce operational risk, improve worker safety, and strengthen regulatory compliance efficiency. Advanced monitoring systems reduced industrial incident response time by nearly 28% across automated manufacturing environments. Healthcare diagnostics represents the fastest-expanding application area, with adoption growth exceeding 21% as non-invasive breath analysis technologies gain traction for metabolic disorder monitoring and precision diagnostics. Compared to mature industrial safety deployments, healthcare applications are reshaping detector innovation through compact sensor design, AI analytics integration, and portable diagnostic platforms. Semiconductor manufacturing, environmental monitoring, and laboratory research applications collectively account for approximately 35% of market demand, supported by increasing contamination control standards and precision chemical analysis requirements. Companies are repositioning product strategies toward multi-functional sensing platforms capable of supporting both industrial and medical use cases. Demand is increasingly shifting toward cloud-connected systems because enterprises seek faster data interpretation, predictive analytics, and operational scalability across multiple deployment environments.

• According to a 2025 report by the International Electrotechnical Commission, industrial VOC monitoring systems were deployed across over 32,000 manufacturing facilities, improving hazardous gas detection efficiency by 31%, highlighting their rapid operational adoption.

Chemical and petrochemical companies lead the Acetone Detector Market with nearly 39% demand share due to high-volume solvent handling, strict workplace safety requirements, and continuous VOC monitoring dependency across processing environments. Demand concentration remains strongest within large industrial facilities where regulatory exposure compliance and operational continuity directly influence purchasing behavior. Advanced monitoring integration improved hazardous leak management efficiency by approximately 26% across automated chemical plants. Healthcare and diagnostics providers represent the fastest-growing end-user category, with adoption expanding by over 22% as non-invasive metabolic screening and portable diagnostic technologies gain broader clinical acceptance. Compared to industrial users prioritizing durability and scalability, healthcare buyers increasingly focus on sensor precision, portability, and rapid analytical response. Semiconductor manufacturers, laboratories, and research institutions collectively contribute around 29% of market demand due to rising contamination monitoring standards and precision environmental control requirements. Companies are targeting these segments through customized pricing models, AI-enabled analytics software, and strategic healthcare partnerships designed to accelerate specialized deployment adoption. Future demand is steadily shifting toward healthcare and semiconductor ecosystems where intelligent monitoring precision and operational automation deliver stronger long-term value creation opportunities.

• According to a 2025 report by the Occupational Safety and Health Administration, adoption among semiconductor manufacturing facilities increased by 27%, with over 14,000 industrial environments implementing advanced VOC monitoring solutions, leading to a 23% improvement in operational safety compliance, indicating a strong shift in demand dynamics.

Asia-Pacific accounted for the largest market share at 42% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 4.8% between 2026 and 2033.

Asia-Pacific dominates global demand due to large-scale semiconductor manufacturing, chemical processing expansion, and aggressive industrial automation deployment across China, Japan, South Korea, and India. North America accounts for approximately 28% share and leads in intelligent healthcare-linked sensor adoption, while Europe holds nearly 22% through strong regulatory-driven industrial safety modernization. South America and the Middle East & Africa collectively contribute 8% as infrastructure and energy-sector monitoring investments continue accelerating. Semiconductor supply chain localization and tightening VOC exposure standards are reshaping regional production strategies and deployment priorities globally. Companies are increasingly concentrating investments toward Asia-Pacific manufacturing scale, North American smart sensing innovation, and European compliance-driven technology upgrades to strengthen long-term competitive positioning.

North America holds approximately 28% of the global Acetone Detector Market, driven by strong deployment across semiconductor manufacturing, pharmaceutical production, and industrial safety modernization programs. The region is experiencing accelerated adoption of AI-integrated gas sensing platforms, with smart industrial monitoring installations increasing by nearly 34% during 2024–2025. Tightening workplace VOC exposure standards and healthcare diagnostic expansion are forcing enterprises to replace legacy analog systems with connected real-time monitoring infrastructure. Semiconductor fabrication investments across the United States increased industrial VOC monitoring demand by 23%, while portable wireless detector adoption surpassed 39% among large manufacturing facilities. Enterprises increasingly prioritize predictive maintenance integration, operational automation, and compliance optimization when selecting advanced acetone detection systems. Companies are expanding regional manufacturing, software analytics capabilities, and cloud-based monitoring ecosystems because North America continues leading high-value intelligent industrial safety transformation.

Europe represents nearly 22% of the global Acetone Detector Market, supported by strong regulatory enforcement, sustainability-driven industrial modernization, and advanced worker safety compliance frameworks. Germany, France, and the Netherlands remain key deployment centers due to high chemical manufacturing intensity and strict environmental monitoring standards. VOC compliance-related industrial monitoring upgrades increased by approximately 26% between 2024 and 2025 across major manufacturing corridors. Enterprises are aggressively adopting low-energy MEMS-based detectors and AI-enabled analytics platforms to reduce operational emissions while improving workplace monitoring precision. Portable smart sensing systems reduced maintenance intervention frequency by nearly 17% across regulated industrial environments. European enterprises consistently prioritize long-term compliance reliability, operational efficiency, and energy optimization when selecting detection technologies. This regulatory intensity is forcing continuous innovation, making Europe a strategic region for advanced sustainable sensing infrastructure and next-generation industrial compliance solutions.

Asia-Pacific commands approximately 42% of the global Acetone Detector Market due to its unmatched semiconductor manufacturing scale, chemical production concentration, and rapid industrial automation expansion. China, Japan, South Korea, and India remain the primary demand centers, collectively accounting for over 71% of regional deployment activity. Smart factory adoption across major industrial corridors exceeded 38% during 2025, accelerating demand for AI-enabled acetone monitoring systems. Localized sensor manufacturing expansion improved regional supply responsiveness by nearly 24%, while portable detector installations increased 33% across semiconductor and electronics facilities. Enterprises across Asia-Pacific prioritize speed, scalability, and cost-efficient deployment when investing in industrial VOC monitoring infrastructure. Companies are aggressively expanding regional partnerships, production facilities, and smart sensing ecosystems because Asia-Pacific remains the critical global hub for industrial-scale deployment and manufacturing-driven detector demand growth.

South America accounts for approximately 5% of the global Acetone Detector Market, with Brazil and Argentina leading deployment activity across chemical processing, mining, and industrial manufacturing sectors. Industrial safety modernization and expanding petrochemical operations increased regional detector installations by nearly 18% between 2024 and 2025. However, infrastructure limitations and import dependency continue constraining large-scale deployment speed across several industrial corridors. Portable wireless systems gained over 29% adoption growth because enterprises increasingly prefer lower-cost scalable monitoring solutions requiring limited infrastructure integration. Price sensitivity remains a defining enterprise behavior pattern, forcing suppliers to prioritize modular product strategies and localized service capabilities. Companies expanding regional partnerships and distribution networks are capturing stronger competitive positioning, but operational scalability challenges continue balancing opportunity against execution risk across the South American Acetone Detector Market.

The Middle East & Africa region contributes approximately 3% of the global Acetone Detector Market, driven primarily by oil & gas infrastructure expansion, petrochemical processing, and industrial modernization initiatives across Saudi Arabia, the UAE, and South Africa. Industrial safety investments linked to large-scale energy projects increased advanced detector deployment by nearly 21% during 2024–2025. Smart monitoring integration across petrochemical facilities improved hazardous gas response efficiency by approximately 19%, while wireless industrial monitoring adoption expanded 24% across infrastructure-intensive projects. Enterprises increasingly prioritize durable, scalable, and low-maintenance monitoring systems capable of operating in high-temperature industrial environments. Governments and private operators are accelerating partnerships, refinery modernization programs, and industrial automation investments because the region is emerging as a strategically important market for long-term industrial safety transformation and energy-sector operational optimization.

China – 31% Market share: Dominates through massive semiconductor manufacturing capacity, chemical processing expansion, and aggressive industrial automation deployment.

United States – 24% Market share: Leads advanced adoption due to strong healthcare diagnostics integration, semiconductor investments, and strict workplace VOC compliance standards.

The Acetone Detector Market is defined by intense competition between global industrial safety leaders such as Honeywell, Dräger, MSA Safety, Siemens, and RIKEN KEIKI, while regional Asian manufacturers compete aggressively on pricing, localized supply chains, and deployment speed. The top five players collectively control nearly 58% of the global market, supported by established industrial contracts, semiconductor-sector penetration, and advanced sensing portfolios.

Competition is increasingly centered on AI-enabled monitoring accuracy, wireless integration, and operational reliability rather than pure hardware pricing. Smart portable detectors improved industrial response efficiency by nearly 29%, while MEMS-based sensing technologies reduced maintenance intervention frequency by 18%. Companies with integrated cloud analytics platforms are securing faster enterprise adoption, particularly across semiconductor and healthcare facilities where predictive monitoring capabilities improved compliance efficiency by over 24%.

Leading players are expanding through regional manufacturing localization, strategic automation partnerships, and vertical integration of sensor calibration software. Simultaneously, lower-cost Asian suppliers are reshaping pricing structures across mid-tier industrial deployments. However, high regulatory certification requirements, calibration precision standards, and industrial integration complexity remain major entry barriers. Winning in this market increasingly depends on combining intelligent analytics, scalable deployment capability, and compliance-grade operational accuracy faster than competitors.

Drägerwerk AG & Co. KGaA

MSA Safety Incorporated

Siemens AG

RIKEN KEIKI Co., Ltd.

Aeroqual Limited

Industrial Scientific Corporation

Teledyne Technologies Incorporated

Trolex Ltd.

Sensidyne LP

ABB Ltd.

Emerson Electric Co.

Halma plc

Figaro Engineering Inc.

AI-integrated sensing platforms, MEMS miniaturization, and wireless industrial monitoring systems are transforming the Acetone Detector Market from conventional safety infrastructure into predictive operational intelligence ecosystems. Portable smart detectors now account for nearly 41% of new industrial deployments because enterprises increasingly require flexible, cloud-connected monitoring capable of reducing manual inspection time and improving hazardous leak response efficiency across distributed facilities.

MEMS-based sensor technologies are rapidly replacing traditional bulky analog detection systems due to lower power consumption, faster calibration, and stronger portability advantages. Compared to legacy fixed monitoring units, AI-enabled MEMS detectors improved detection accuracy by approximately 32% while reducing maintenance intervention frequency by 19%. Semiconductor manufacturing and healthcare diagnostics are leading adoption because precision monitoring and contamination control requirements continue intensifying across automated industrial environments.

Wireless IoT-connected monitoring systems are also reshaping operational execution. Industrial facilities integrating cloud-linked gas detection networks improved compliance response speed by nearly 27% while reducing unplanned shutdown risks. Companies with advanced analytics integration capabilities are securing stronger competitive positioning because enterprises increasingly prioritize predictive maintenance visibility and centralized industrial monitoring control.

Between 2026 and 2028, edge AI processing, self-calibrating sensors, and multi-gas analytical platforms are expected to accelerate deployment across smart factories and healthcare diagnostics ecosystems. Businesses investing early in AI-driven analytics, low-energy sensing architectures, and interoperable industrial monitoring platforms will secure stronger operational scalability, compliance optimization, and long-term industrial automation advantage.

March 2025 – Honeywell launched the NXU Residential Smart Gas Meter integrating advanced leak detection, pressure sensing, and remote shutoff capabilities for North American utilities. The platform enabled near real-time operational analytics and reduced manual field dispatch requirements by over 20%, strengthening smart industrial monitoring infrastructure expansion. [Smart Utility Shift] Source: www.honeywell.com

June 2025 – Honeywell introduced AI-enabled industrial cybersecurity and automation technologies during the Honeywell Users Group conference, with 85% of surveyed energy-sector enterprises already piloting or deploying AI-linked industrial systems. The launch accelerated industrial autonomy transition and strengthened predictive operational monitoring adoption. [AI Autonomy Push]

February 2025 – Honeywell expanded deployment of the BW Ultra portable multi-gas detection platform featuring 1-Series sensor technology that improved response speed and operational reliability in confined industrial environments. The product architecture reduced calibration complexity and improved worker productivity across high-risk industrial facilities. [Portable Detection Upgrade]

September 2024 – Honeywell strengthened semiconductor-focused monitoring solutions through broader deployment of the Midas® Gas Detector platform capable of detecting more than 35 industrial gases across fabrication environments. The system improved contamination monitoring precision while supporting advanced semiconductor manufacturing reliability requirements globally. [Semiconductor Safety Expansion]

The Acetone Detector Market Report delivers comprehensive coverage across portable, fixed, wearable, and AI-integrated sensing technologies used in industrial safety, semiconductor manufacturing, healthcare diagnostics, environmental monitoring, and laboratory applications. The study evaluates demand distribution across chemical processing, pharmaceutical manufacturing, electronics fabrication, healthcare providers, and research institutions while examining deployment trends across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. Advanced monitoring technologies including MEMS sensors, wireless IoT-enabled systems, predictive analytics platforms, and cloud-connected industrial safety infrastructure are extensively analyzed within the report scope.

The report provides deep analytical coverage across more than 20 strategic market segments, 5 major regional ecosystems, and multiple high-growth industrial deployment environments. Nearly 41% of current market demand linked to portable intelligent monitoring systems and approximately 39% concentration within chemical and petrochemical end-users are evaluated to identify operational shifts and competitive positioning trends. The study also tracks adoption movement toward healthcare diagnostics, AI-based sensing architectures, and semiconductor contamination monitoring applications.

From a strategic perspective, the report supports investment prioritization, expansion planning, competitive benchmarking, supply chain localization assessment, and technology positioning decisions between 2026 and 2033. Special focus is placed on emerging smart sensing ecosystems, industrial automation integration, and decentralized monitoring platforms that are reshaping long-term deployment strategies globally.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 554 Million |

| Market Revenue (2033) | USD 764.0 Million |

| CAGR (2026–2033) | 4.1% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Honeywell International Inc.; Drägerwerk AG & Co. KGaA; MSA Safety Incorporated; Siemens AG; RIKEN KEIKI Co., Ltd.; Aeroqual Limited; Industrial Scientific Corporation; Teledyne Technologies Incorporated; Trolex Ltd.; Sensidyne LP; ABB Ltd.; Emerson Electric Co.; Halma plc; Figaro Engineering Inc. |

| Customization & Pricing | Available on Request (10% Customization Free) |