Reports

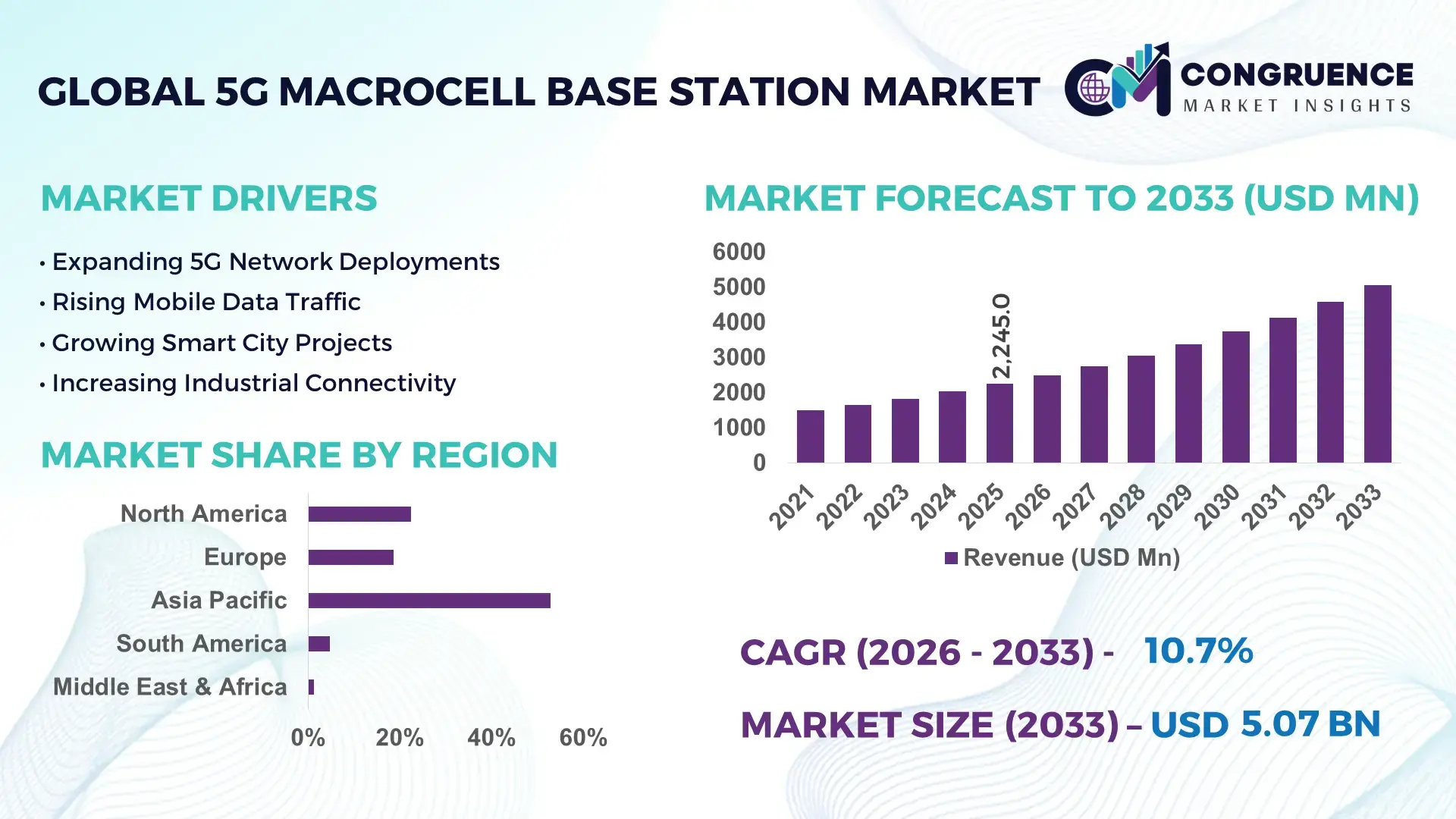

The Global 5G Macrocell Base Station Market was valued at USD 2,245.0 Million in 2025 and is anticipated to reach a value of USD 5,066.5 Million by 2033 expanding at a CAGR of 10.71% between 2026 and 2033. Growth is being accelerated by nationwide standalone 5G deployments, Open RAN integration, and telecom operators expanding mid-band spectrum coverage to support industrial connectivity and ultra-high-capacity mobile networks.

China remains the dominant country in the market, accounting for more than 45% of global 5G base station installations, supported by over 4.3 million deployed 5G sites and continuous infrastructure investment across manufacturing, transportation, and smart city ecosystems. In comparison, the United States contributes nearly 12% of global deployments while emphasizing advanced network modernization and private 5G applications. The ongoing digital infrastructure race between China and the U.S. continues to influence equipment procurement, spectrum strategies, and technology standardization across global telecom markets.

For market participants, deployment scale, spectrum efficiency, and ecosystem partnerships are becoming the primary determinants of long-term competitive positioning.

Market Size & Growth: Valued at USD 2,245.0 Million in 2025 and projected to reach USD 5,066.5 Million by 2033, supported by Open RAN adoption, standalone 5G expansion, and large-scale telecom infrastructure modernization.

Top Growth Drivers: Mid-band spectrum deployments exceed 55% of new installations, network virtualization adoption surpasses 40%, and industrial 5G connectivity projects increased by over 35% globally.

Short-Term Forecast: By 2028, network energy consumption per transmitted bit is expected to decline by nearly 30% through AI-driven radio optimization and advanced power management systems.

Emerging Technologies: AI-native RAN, Open RAN architectures, and cloud-based baseband processing are improving network automation by more than 25%.

Regional Leaders: Asia Pacific exceeds USD 2.3 Billion supported by dense urban deployments, North America surpasses USD 1.1 Billion through private networks, and Europe approaches USD 0.9 Billion through infrastructure upgrades.

Consumer/End-User Trends: Over 68% of mobile traffic now runs on 5G-capable networks in leading telecom markets, driving capacity-focused macrocell investments.

Pilot/Case Example: In 2024, AI-powered radio optimization deployments improved spectrum utilization by approximately 20% while reducing operational intervention requirements.

Competitive Landscape: Huawei holds an estimated 30%+ market share, with Ericsson, Nokia, ZTE, and Samsung strengthening positions through network modernization contracts.

Regulatory & ESG Impact: Energy-efficient radio platforms reduce site power consumption by nearly 25%, aligning with national telecom sustainability mandates.

Investment & Funding: Global telecom infrastructure investments exceed USD 100 Billion annually, with increasing focus on Open RAN partnerships and localized supply chains.

Innovation & Future Outlook: AI-native network orchestration, integrated sensing capabilities, and software-defined radio architectures are reshaping next-generation telecom infrastructure strategies.

The 5G Macrocell Base Station Market is witnessing strong demand from telecom operators, industrial campuses, transportation corridors, and smart manufacturing facilities seeking broader coverage and higher network capacity. AI-enabled radio resource management and cloud-native network architectures are improving operational efficiency, while Open RAN deployments have expanded by more than 40% across selected markets. Simultaneously, supply-chain localization initiatives and spectrum policy reforms are influencing procurement strategies, creating a more diversified and resilient infrastructure ecosystem that sets the stage for deeper strategic evaluation.

The 5G Macrocell Base Station Market has become a strategic pillar of digital infrastructure because network performance increasingly determines competitiveness across manufacturing, logistics, healthcare, transportation, and public services. Telecom operators are prioritizing large-scale infrastructure modernization to support higher data throughput, lower latency, and expanding connected-device ecosystems. At the same time, geopolitical technology competition and telecom equipment localization initiatives are reshaping supply chains and procurement strategies.

Modern 5G macrocell platforms deliver up to 3–5 times greater spectral efficiency than many legacy 4G configurations while reducing energy consumption per unit of traffic by approximately 20–30%. China continues to lead deployment scale through extensive nationwide coverage programs, whereas the United States and several European countries focus on private networks, Open RAN ecosystems, and advanced enterprise applications. Over the next two to three years, AI-driven network automation is expected to significantly increase operational efficiency and reduce manual optimization requirements.

A practical example can be seen in large industrial parks deploying macrocell infrastructure to support autonomous operations, connected machinery, and real-time monitoring systems. In response, equipment vendors are expanding software capabilities, strengthening cloud partnerships, and investing in AI-native radio technologies. Organizations that secure spectrum assets, deployment partnerships, and advanced network management capabilities will establish stronger competitive positioning and long-term operational advantages.

Standalone 5G deployment programs are transforming telecom infrastructure strategies worldwide. More than 55% of newly deployed 5G networks now prioritize standalone architectures, enabling lower latency, network slicing, and industrial-grade connectivity. China has deployed over 4 million 5G base stations, while industrial 5G application projects have expanded by more than 35% across manufacturing and logistics environments. The ongoing shift toward Open RAN and cloud-native network architectures is improving deployment flexibility and vendor interoperability. As network traffic continues migrating toward bandwidth-intensive applications, operators are increasing capital allocation toward macrocell densification and spectrum utilization improvements. Equipment suppliers are responding through AI-integrated radio systems, strategic partnerships, and advanced antenna innovations that improve network capacity while reducing operational complexity.

High infrastructure deployment costs remain a significant structural limitation for market expansion. Radio units, advanced antenna systems, fiber backhaul integration, and power infrastructure can represent more than 60% of total deployment expenditure in certain markets. Global semiconductor supply fluctuations and specialized component dependencies have increased procurement lead times by approximately 15–20% in selected telecom projects. Several emerging economies also face spectrum affordability challenges and limited rural fiber availability, restricting deployment scalability. These constraints directly impact rollout timelines, operational efficiency, and investment returns. To mitigate exposure, telecom vendors are localizing manufacturing, diversifying supplier networks, and entering long-term procurement agreements that improve component availability and deployment predictability.

Industrial digitalization presents one of the strongest opportunities for 5G macrocell infrastructure providers. More than 70% of large manufacturing enterprises are evaluating advanced connectivity solutions to support automation, predictive maintenance, and autonomous operations. AI-enabled radio optimization platforms can improve spectrum efficiency by over 20%, while network automation technologies reduce operational intervention requirements significantly. India, Saudi Arabia, and Indonesia are accelerating digital infrastructure programs and spectrum modernization initiatives that create new deployment opportunities. Vendors are investing heavily in AI-native RAN platforms, private-public network integration models, and ecosystem partnerships. A particularly valuable opportunity lies in enabling mission-critical industrial applications where reliability, coverage, and network intelligence generate substantial operational value beyond traditional consumer connectivity services.

Managing increasingly software-defined telecom infrastructure introduces substantial execution complexity. Open RAN environments can involve 30–40% more integration points than traditional single-vendor deployments, increasing testing, validation, and interoperability requirements. Simultaneously, mobile data traffic growth exceeding 25% annually in many advanced telecom markets places continuous pressure on network optimization and performance management capabilities. Cybersecurity requirements are also intensifying as critical infrastructure operators adopt cloud-native architectures and virtualized network functions. These factors affect deployment consistency, service quality, and long-term operational sustainability. Leading vendors are investing in AI-driven network assurance, automated security monitoring, and advanced interoperability frameworks to address complexity while maintaining performance, resilience, and regulatory compliance across large-scale network environments.

AI-Driven Network Optimization Telecom operators are increasingly embedding AI into radio access networks to automate traffic balancing and spectrum allocation. AI-enabled optimization has improved spectrum utilization by nearly 20% while reducing manual network intervention by over 30%. As mobile data volumes continue rising by more than 25% annually in several advanced markets, operators are deploying self-organizing network platforms to improve service consistency and reduce operating expenses. Vendors are responding through AI-native RAN software partnerships and cloud-integrated management platforms.

Open RAN Ecosystem Expansion Open RAN deployments are accelerating as operators seek greater vendor flexibility and supply-chain resilience. Open architecture adoption has expanded by more than 40% across new deployment projects, while multi-vendor integration initiatives have increased by approximately 35%. Geopolitical procurement restrictions and telecom security policies are encouraging diversification away from single-vendor ecosystems. Infrastructure providers are expanding interoperability testing programs, forming strategic alliances, and developing software-centric radio platforms that simplify network modernization.

Energy-Efficient Radio Deployment Energy consumption has become a major operational focus as network density increases. New-generation radio units reduce power usage by approximately 25%, while intelligent sleep-mode technologies lower site energy demand by nearly 15%. Rising electricity costs and national sustainability targets are accelerating adoption across large telecom networks. Equipment manufacturers are redesigning hardware architectures, integrating advanced semiconductor technologies, and prioritizing energy-performance metrics within procurement frameworks.

Industrial 5G Coverage Scaling Manufacturing facilities, logistics hubs, and transportation corridors are increasingly driving macrocell deployment strategies. Industrial connectivity projects have expanded by more than 35%, while enterprise-grade private-public network integration initiatives have grown nearly 28%. The shift toward automated operations and connected infrastructure is increasing demand for broader coverage and network reliability. Telecom vendors are expanding ecosystem partnerships, deploying dedicated industrial solutions, and aligning network architectures with operational technology requirements.

The Sub-6 GHz segment holds the leading position in the 5G Macrocell Base Station Market, accounting for an estimated 65%–70% of active deployments. Its dominance stems from superior coverage efficiency, lower infrastructure density requirements, and strong compatibility with existing telecom networks. Operators in China, India, and the United States continue prioritizing Sub-6 GHz deployments because a single site can cover significantly larger geographic areas compared to higher-frequency alternatives. The segment remains critical for nationwide coverage programs, rural connectivity expansion, and large-scale consumer broadband services. Vendors are strengthening portfolios through advanced Massive MIMO integration and AI-enabled radio optimization solutions to maximize spectral efficiency and network performance. The mmWave segment is emerging as the fastest-growing category due to increasing demand for ultra-high-capacity urban networks, industrial campuses, transportation hubs, and dense enterprise environments. Deployment activity has increased by more than 35% in selected metropolitan zones where high traffic concentration requires greater bandwidth availability. While mmWave addresses capacity-intensive use cases, Sub-6 GHz continues to anchor broad coverage strategies. Companies are investing in hybrid deployment architectures that combine both technologies, enabling operators to balance coverage, capacity, and operational economics while supporting increasingly diverse connectivity requirements.

Enhanced Mobile Broadband (eMBB) remains the leading application segment, representing approximately 55%–60% of macrocell deployment demand. Rising video streaming traffic, cloud gaming, fixed wireless access, and high-definition mobile content consumption continue to increase network capacity requirements. Telecom operators are expanding macrocell coverage and implementing advanced antenna systems to manage traffic growth that exceeds 25% annually in several high-adoption markets. Network modernization initiatives are increasingly centered on improving throughput, reducing congestion, and supporting growing subscriber expectations for seamless connectivity. The Massive Machine-Type Communications (mMTC) segment is experiencing the fastest expansion as industrial digitalization accelerates across manufacturing, utilities, logistics, and smart city infrastructure. Connected device deployments have increased by more than 30% across several industrial ecosystems, creating demand for scalable network architectures capable of supporting millions of endpoints. Meanwhile, Ultra-Reliable Low-Latency Communications (URLLC) is gaining traction in autonomous systems, industrial automation, and mission-critical operations where reliability requirements exceed traditional network capabilities. Vendors are responding through AI-driven network management, industrial-grade connectivity solutions, and enterprise-focused deployment models that expand application diversity beyond consumer broadband services.

Telecommunication Service Providers represent the largest end-user segment, accounting for roughly 75% of overall deployment activity. Their leadership reflects extensive nationwide coverage obligations, subscriber growth requirements, and ongoing infrastructure modernization programs. Large operators continue investing heavily in network densification, spectrum utilization optimization, and standalone 5G architecture upgrades. As mobile data traffic expands by more than 25% annually in many developed markets, operators are prioritizing advanced radio technologies, cloud-native infrastructure, and AI-based network automation to improve performance and operational efficiency. The Enterprise and Industrial Sector has emerged as the fastest-growing end-user category as manufacturers, logistics providers, mining companies, and transportation operators accelerate digital transformation initiatives. Enterprise-focused deployments have increased by more than 30% in industrial environments seeking greater automation, predictive maintenance, and real-time operational visibility. Government agencies and public infrastructure operators are also increasing investments to support smart city initiatives and critical communications networks. In response, vendors are developing industry-specific solutions, forming ecosystem partnerships, and introducing flexible deployment models tailored to operational technology environments and specialized connectivity requirements.

Asia-Pacific accounted for the largest market share at 52.8% in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 12.4% between 2026 and 2033.

North America represented approximately 22.4% of the global 5G Macrocell Base Station Market in 2025, supported by aggressive standalone 5G deployment programs, fixed wireless access expansion, and increasing enterprise connectivity requirements. The region remains a leader in Open RAN implementation, cloud-native network architecture adoption, and AI-driven network optimization. Telecom operators continue expanding mid-band spectrum utilization to improve network coverage and capacity across urban and suburban markets. More than 70% of population coverage in key metropolitan corridors is now supported by advanced 5G infrastructure. Strategic collaborations between operators, cloud providers, and network equipment vendors are strengthening deployment efficiency while reducing operational complexity across large-scale network environments.

United States Market Outlook: The United States dominates regional deployment activity through extensive spectrum resources, strong telecom infrastructure investment, and advanced enterprise digitalization initiatives. The country leads adoption of private 5G networks across manufacturing, logistics, ports, and energy facilities. More than 300 commercial private wireless deployments have been announced across industrial environments, supporting automation, predictive maintenance, and connected operations. Continued investment in Open RAN ecosystems and AI-enabled network management platforms is strengthening the country's position as a leading innovation hub for next-generation telecom infrastructure.

Europe accounted for nearly 18.7% of global market demand, driven by network modernization initiatives, digital sovereignty strategies, and sustainability-focused telecom investment. Operators are increasingly replacing legacy infrastructure with energy-efficient radio systems capable of reducing power consumption by over 20%. The region continues advancing multi-vendor interoperability programs to diversify equipment procurement and strengthen network resilience. Regulatory support for digital infrastructure modernization is accelerating deployment activity across transportation networks, industrial corridors, and smart city initiatives. Telecom providers are also integrating AI-based automation systems to improve network performance and reduce operational intervention requirements.

Germany Market Outlook: Germany serves as the region's most strategically important market due to its industrial strength, advanced manufacturing ecosystem, and strong enterprise connectivity requirements. The country remains a leader in industrial private 5G deployments supporting automotive production, smart factories, and logistics operations. More than 75% of large industrial operators are actively evaluating or implementing advanced wireless connectivity solutions. Strong collaboration between telecom providers, equipment manufacturers, and industrial enterprises continues to accelerate deployment of mission-critical communications infrastructure across key economic sectors.

Asia-Pacific remains the dominant regional market, contributing approximately 52.8% of global demand in 2025. The region benefits from extensive telecom infrastructure investments, high subscriber density, strong manufacturing capabilities, and government-backed digital transformation programs. Large-scale deployment strategies continue expanding coverage across urban, suburban, and industrial environments. More than half of newly deployed macrocell sites globally are concentrated within Asia-Pacific markets. Telecom operators are increasingly integrating Massive MIMO technologies, AI-powered optimization platforms, and cloud-native network architectures to improve capacity and network efficiency. Regional equipment manufacturing strength also enhances deployment speed and supply-chain stability.

China Market Outlook: China remains the largest individual market globally, supported by unmatched deployment scale and infrastructure investment. The country has surpassed 4.3 million deployed 5G base stations, creating extensive coverage across manufacturing hubs, transportation networks, and smart city ecosystems. Strong integration of industrial internet applications and advanced wireless connectivity continues driving macrocell deployment requirements. Domestic equipment manufacturers maintain significant technological and production capabilities, enabling rapid rollout schedules while supporting the country's broader digital infrastructure modernization objectives.

South America accounted for approximately 4.8% of global market activity in 2025, with deployment growth supported by expanding spectrum availability, increasing smartphone penetration, and telecom network modernization initiatives. Operators are prioritizing macrocell infrastructure to improve coverage quality and address rising mobile broadband consumption. Urban deployment concentration remains high, although rural connectivity programs are gradually expanding network footprints. Infrastructure investment partnerships between telecom operators and tower companies are improving rollout efficiency and reducing deployment costs. Despite strong momentum, fiber backhaul availability and spectrum affordability continue influencing deployment timelines across several markets.

Brazil Market Outlook: Brazil leads regional market development through its large subscriber base, expanding digital economy, and nationwide 5G deployment strategy. Telecom operators continue increasing macrocell investments to strengthen coverage across major metropolitan areas and industrial zones. More than 80% of the country's population is expected to gain access to advanced 5G services through ongoing network expansion initiatives. Growing demand from agribusiness, logistics, mining, and manufacturing sectors is creating additional opportunities for high-capacity macrocell infrastructure deployment throughout the country.

Middle East & Africa represents a smaller share of global deployments but exhibits the strongest forward-looking expansion profile. The region is benefiting from national digital transformation agendas, smart city investments, and extensive telecommunications modernization programs. Governments and telecom operators are accelerating deployment of advanced wireless infrastructure to support economic diversification strategies and emerging digital services. Several Gulf countries have achieved population coverage rates exceeding 75% in key urban areas. Strategic investment in fiber infrastructure, data centers, and cloud ecosystems is creating favorable conditions for broader macrocell deployment while strengthening overall network performance.

Saudi Arabia Market Outlook: Saudi Arabia has emerged as the region's most influential market due to large-scale infrastructure investment, ambitious digital transformation objectives, and strong regulatory support for advanced connectivity technologies. Telecom operators continue expanding nationwide 5G coverage while supporting industrial diversification initiatives across energy, logistics, manufacturing, and smart city projects. More than 80% population coverage has been achieved in several major urban centers. Ongoing investment in intelligent infrastructure and enterprise digitalization programs continues positioning the country as a strategic leader in advanced wireless network deployment.

The competitive landscape is dominated by Huawei Technologies, Ericsson, Nokia, ZTE Corporation, and Samsung Electronics, which collectively control approximately 75–80% of global macrocell base station deployments. Competition primarily occurs between Chinese scale leaders and Western infrastructure vendors, while Open RAN specialists increasingly challenge traditional integrated-network suppliers. Technology performance, energy efficiency, deployment speed, and supply-chain resilience have become the primary competitive battlegrounds. Advanced Massive MIMO radios deliver up to 30% lower power consumption, while AI-enabled network optimization improves spectrum utilization by nearly 20%. Open RAN adoption has increased more than 40%, intensifying pressure on proprietary network architectures. Companies are expanding manufacturing footprints, pursuing long-term operator agreements, strengthening software capabilities, and vertically integrating radio, cloud, and AI platforms. The market is also experiencing a shift from hardware-centric competition toward software-defined and AI-native networks. Regulatory scrutiny, spectrum expertise, and operator qualification requirements remain significant barriers. Winning requires superior network performance, trusted supply chains, AI-driven automation capabilities, and deep telecom operator relationships.

Ericsson

Nokia

Samsung Electronics

ZTE Corporation

Fujitsu Limited

NEC Corporation

Mavenir Systems

Airspan Networks

Parallel Wireless

Comba Telecom Systems

JMA Wireless

Ceragon Networks

Tejas Networks

The technology landscape is rapidly shifting from conventional hardware-centric radio networks toward AI-native, software-defined infrastructure. Massive MIMO, beamforming, and standalone 5G architectures remain the core deployment technologies, supporting over 70% of newly deployed macrocell sites. Compared with legacy 4G radio systems, advanced 5G macrocell platforms deliver up to 4 times greater spectral efficiency and approximately 25% lower energy consumption per transmitted bit. Telecom operators benefit through improved network capacity, reduced congestion, and enhanced asset utilization.

Emerging technologies are centered on Open RAN, virtualized RAN (vRAN), cloud-native baseband processing, and AI-driven network automation. Open RAN adoption has surpassed 40% in several modernization programs, while AI-assisted optimization improves spectrum utilization by nearly 20%. Integration between AI engines, cloud platforms, and radio access networks enables autonomous fault detection, predictive maintenance, and dynamic resource allocation. Operators deploying these technologies gain measurable advantages in deployment flexibility, vendor diversification, and operating efficiency.

Between 2026 and 2028, AI-RAN, intelligent network orchestration, and 5G-Advanced technologies are expected to become major differentiators. Companies with strong software ecosystems, cloud partnerships, and AI integration capabilities will benefit most. As network intelligence becomes increasingly critical, competitive advantage will shift from radio hardware performance alone toward automation, analytics, and adaptive network management capabilities that accelerate service delivery and lower lifecycle operating costs.

June 2024 – Huawei Technologies announced commercial 5G-Advanced deployment initiatives and highlighted industry adoption across more than 60 operators globally, with network speeds reaching 5 Gbps through 3CC technology. The development strengthens Huawei’s leadership in next-generation radio infrastructure and AI-enabled network evolution. Source: www.huawei.com

December 2024 – Ericsson secured a major agreement with Bharti Airtel to deploy centralized RAN and Open RAN-ready 5G solutions across India. The project enhances coverage, speed, and network reliability while strengthening Ericsson’s position in one of the world's largest 5G deployment markets.

March 2026 – Samsung Electronics expanded its Open RAN footprint after being selected by Rakuten Mobile to support nationwide 5G radio deployment in Japan. The initiative accelerates commercial cloud-native network expansion and reinforces Samsung's leadership in virtualized radio access network technologies.

January 2026 – Samsung Electronics achieved the industry's first commercial virtualized RAN call using Intel Xeon 6 processors with up to 72 cores on a live Tier-1 operator network. The milestone advances AI-native and 6G-ready network architectures while improving processing efficiency and deployment flexibility.

The report provides comprehensive analysis of the global 5G Macrocell Base Station Market across major technology categories, deployment architectures, applications, end-user groups, and regional markets. Coverage includes Sub-6 GHz and mmWave infrastructure, alongside key application areas such as Enhanced Mobile Broadband (eMBB), Massive Machine-Type Communications (mMTC), and Ultra-Reliable Low-Latency Communications (URLLC). The study evaluates demand patterns across telecommunications operators, industrial enterprises, government organizations, and emerging private-network deployments. Regional assessment covers North America, Europe, Asia-Pacific, South America, and Middle East & Africa, representing more than 95% of global deployment activity.

The report also examines adoption of Open RAN, AI-RAN, virtualized RAN, cloud-native architectures, Massive MIMO, and 5G-Advanced technologies. Strategic insights include competitive positioning, deployment strategies, infrastructure investment trends, supply-chain developments, and operator modernization priorities. The analysis supports expansion planning, technology evaluation, partnership decisions, and long-term market positioning through 2033 while identifying emerging opportunities across industrial digitalization, private wireless networks, and intelligent connectivity ecosystems.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 2,245.0 Million |

| Market Revenue (2033) | USD 5,066.5 Million |

| CAGR (2026–2033) | 10.71% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Huawei Technologies; Ericsson; Nokia; Samsung Electronics; ZTE Corporation; Fujitsu Limited; NEC Corporation; Mavenir Systems; Airspan Networks; Parallel Wireless; Comba Telecom Systems; JMA Wireless; Ceragon Networks; Tejas Networks |

| Customization & Pricing | Available on Request (10% Customization Free) |