Reports

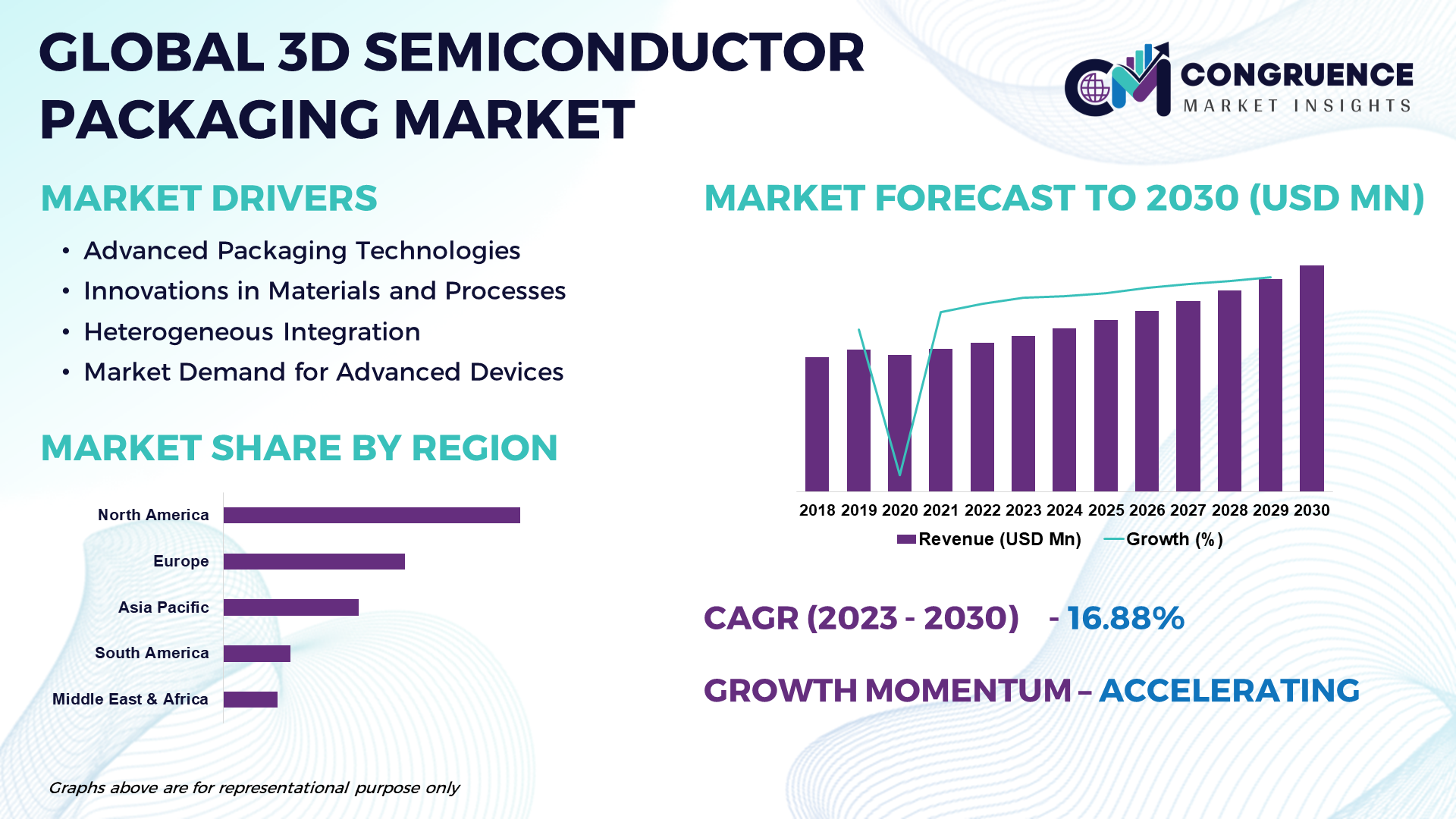

The emergence of 3D semiconductor packaging represents a revolutionary shift in electronics manufacturing, introducing a three-dimensional methodology to integrate and stack multiple semiconductor components. This groundbreaking technology addresses the constraints of traditional 2D packaging by providing improved performance, minimized form factors, and increased energy efficiency. The upgrading of technology in 3D semiconductor packaging employs advanced techniques such as through-silicon via (TSV) and wafer-level packaging, facilitating the vertical integration of chips to enhance data processing speeds. Noteworthy innovations include the integration of heterogeneous components, utilization of advanced thermal management materials, and the adoption of inventive packaging architectures like fan-out wafer-level packaging (FOWLP). Within this dynamic market landscape, marked by fierce competition and swift advancements, major industry players are actively channeling investments into research and development. The global market is experiencing widespread acceptance across various sectors, encompassing consumer electronics, automotive, and telecommunications, driven by the rising demand for compact, high-performance devices. This trend fosters a landscape characterized by continual evolution and collaborative efforts. The Global 3D Semiconductor Packaging Market is expected to expand at a CAGR of 16.88% between 2023 and 2030.

3D Semiconductor Packaging Market Major Driving Forces

Advanced Packaging Technologies: Demand for smaller and more compact electronic devices drives the need for advanced packaging. 3D semiconductor packaging enables component stacking, reducing form factors. Additionally, contribution to the creation of compact devices, including smartphones, wearables, and IoT devices.

Innovations in Materials and Processes: Ongoing innovations in materials and manufacturing processes contribute to the development of more reliable and efficient 3D semiconductor packaging solutions, attracting further interest and investment from industry players.

Heterogeneous Integration: The trend towards heterogeneous integration, which involves combining different technologies and functionalities on a single chip, is a driving force for 3D semiconductor packaging. This approach enables the creation of more versatile and efficient semiconductor devices.

Market Demand for Advanced Devices: Adoption of 3D semiconductor packaging fueled by increasing market demand. Furthermore, characterized by superior performance, enhanced functionality, and improved energy efficiency. Across diverse industries such as consumer electronics, automotive, and telecommunications.

3D Semiconductor Packaging Market Key Opportunities

Integration of Internet of Things (IoT) Devices: With the proliferation of IoT devices, there is a significant opportunity for 3D semiconductor packaging to contribute to the development of compact, energy-efficient, and multifunctional chips for diverse IoT applications.

Rapid deployment of 5G Technology: The deployment of 5G networks creates opportunities for 3D packaging to support the development of high-performance semiconductor components for 5G-enabled devices and infrastructure.

Artificial Intelligence (AI) Hardware: As AI applications continue to grow, there is a significant opportunity for 3D semiconductor packaging to play a crucial role in developing high-performance and energy-efficient AI hardware solutions.

3D Semiconductor Packaging Market Key Trends

· The 3D semiconductor packaging market is witnessing a surge in the momentum behind heterogeneous integration, marked by the amalgamation of various technologies on a single chip.

· Empowered by 3D semiconductor packaging, System-in-Package (SiP) architectures are gaining prominence.

· Emergence of Fan-Out Wafer-Level Packaging (FOWLP) redistributes individual dies across a larger substrate area, facilitating increased input/output connections and enhancing thermal performance, especially in mobile and high-performance computing applications.

· The market is witnessing innovations in materials dedicated to thermal management in 3D semiconductor packaging.

· Optimization of 3D semiconductor packaging is underway to meet the distinctive requirements of AI processors, encompassing efficient power delivery and effective heat dissipation.

Market Competition Landscape

In the 3D semiconductor packaging market, a dynamic competitive environment is marked by fierce competition among major players. To remain leaders, top semiconductor manufacturers consistently allocate resources to research and development, ensuring they are at the cutting edge of technological progress. Maintaining a competitive advantage involves ongoing innovation in packaging solutions, strategic partnerships, and the pursuit of patents. Companies also prioritize meeting the market's need for compact, high-performance devices across diverse industries, emphasizing the importance of adaptability and technological expertise for enduring success in this evolving landscape.

Key players in the global 3D Semiconductor Packaging market implement various organic and inorganic strategies to strengthen and improve their market positioning. Prominent players in the market include:

· Jiangsu Changdian Technology Co., Ltd.

· Advanced Micro Devices, Inc.

· Qualcomm Technologies, Inc.

· Taiwan Semiconductor Manufacturing Company Limited

· Samsung

· Amkor Technology

· United Microelectronics Corporation

· Intel Corporation

· SMG

· UTAC

· Siemens

· Texas Instruments Incorporated

· Powertech Technology Inc.

· Micron Technology, Inc.

· SK HYNIX INC.

· Cadence Design Systems, Inc.

|

Report Attribute/Metric |

Details |

|

Base Year |

2022 |

|

Forecast Period |

2023 – 2030 |

|

Historical Data |

2018 to 2022 |

|

Forecast Unit |

Value (US$ Mn) |

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Segments Covered |

· By Type (3D Through-Silicon Via (TSV), 3D Package-on-Package (PoP), Fan-Out WLP (Wafer-Level Packaging), Others) · By Technology (Wire Bonding, Die-to-Die bonding, and Flip-Chip Bonding) · By Application (Micro-Electro-Mechanical Systems (MEMS), Advanced Driver Assistance Systems (ADAS), Industrial Automation & Robotics, DRAM (Dynamic Random Access Memory) and NAND Flash, Medical Imaging Equipment, and Others) · By End-User Industry (Consumer Electronics, Automotive, IT & Telecommunications, Medical Device and Others) |

|

Geographies Covered |

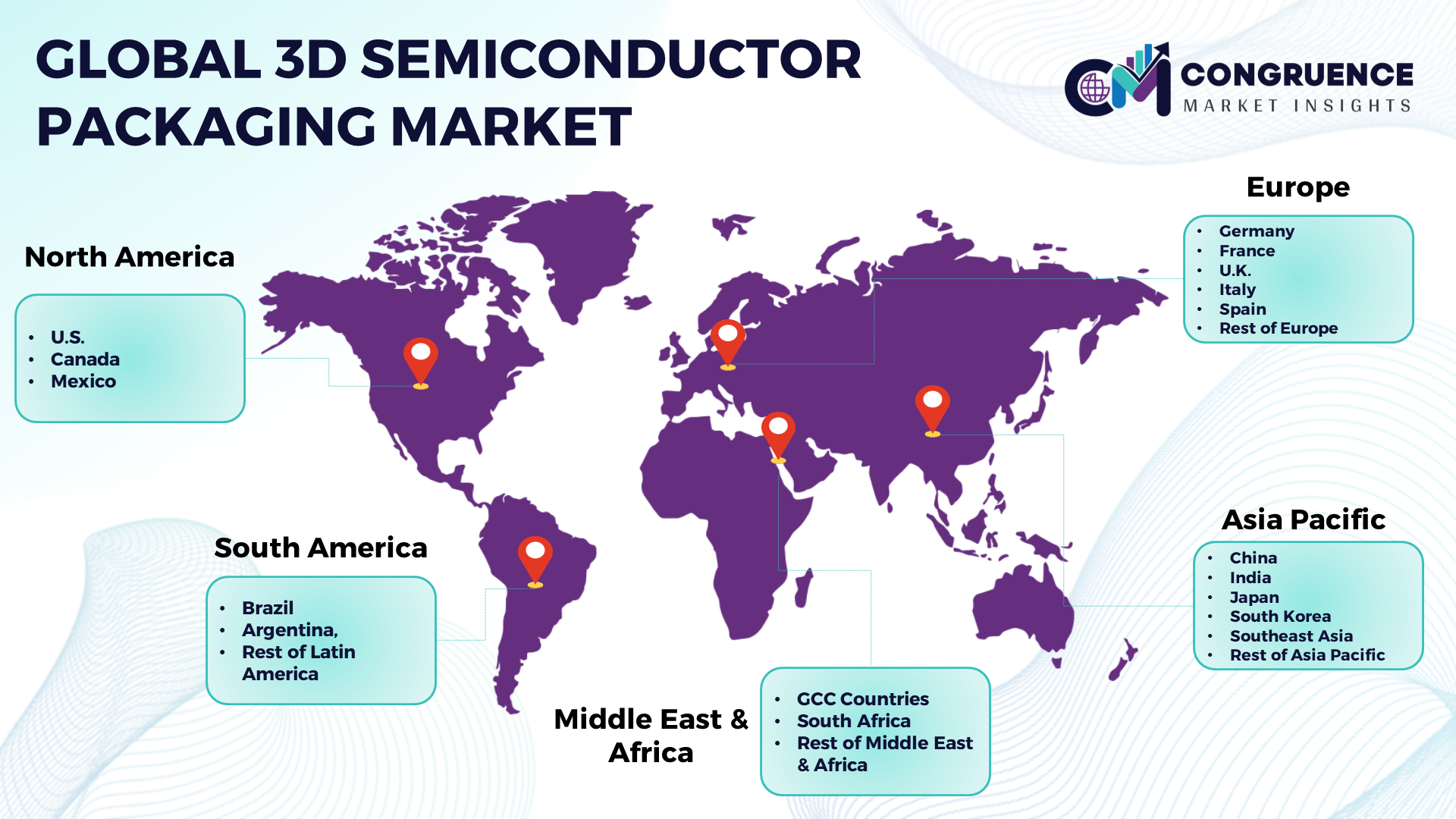

North America: U.S., Canada and Mexico Europe: Germany, France, U.K., Italy, Spain, and Rest of Europe Asia Pacific: China, India, Japan, South Korea, Southeast Asia, and Rest of Asia Pacific South America: Brazil, Argentina, and Rest of Latin America Middle East & Africa: GCC Countries, South Africa, and Rest of Middle East & Africa |

|

Key Players Analyzed |

Jiangsu Changdian Technology Co., Ltd., Advanced Micro Devices, Inc., Qualcomm Technologies, Inc., Taiwan Semiconductor Manufacturing Company Limited, Samsung, Amkor Technology, United Microelectronics Corporation, Intel Corporation, SMG, UTAC, Siemens, Texas Instruments Incorporated, Powertech Technology Inc., Micron Technology, Inc., SK HYNIX INC., Cadence Design Systems, Inc. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |