Reports

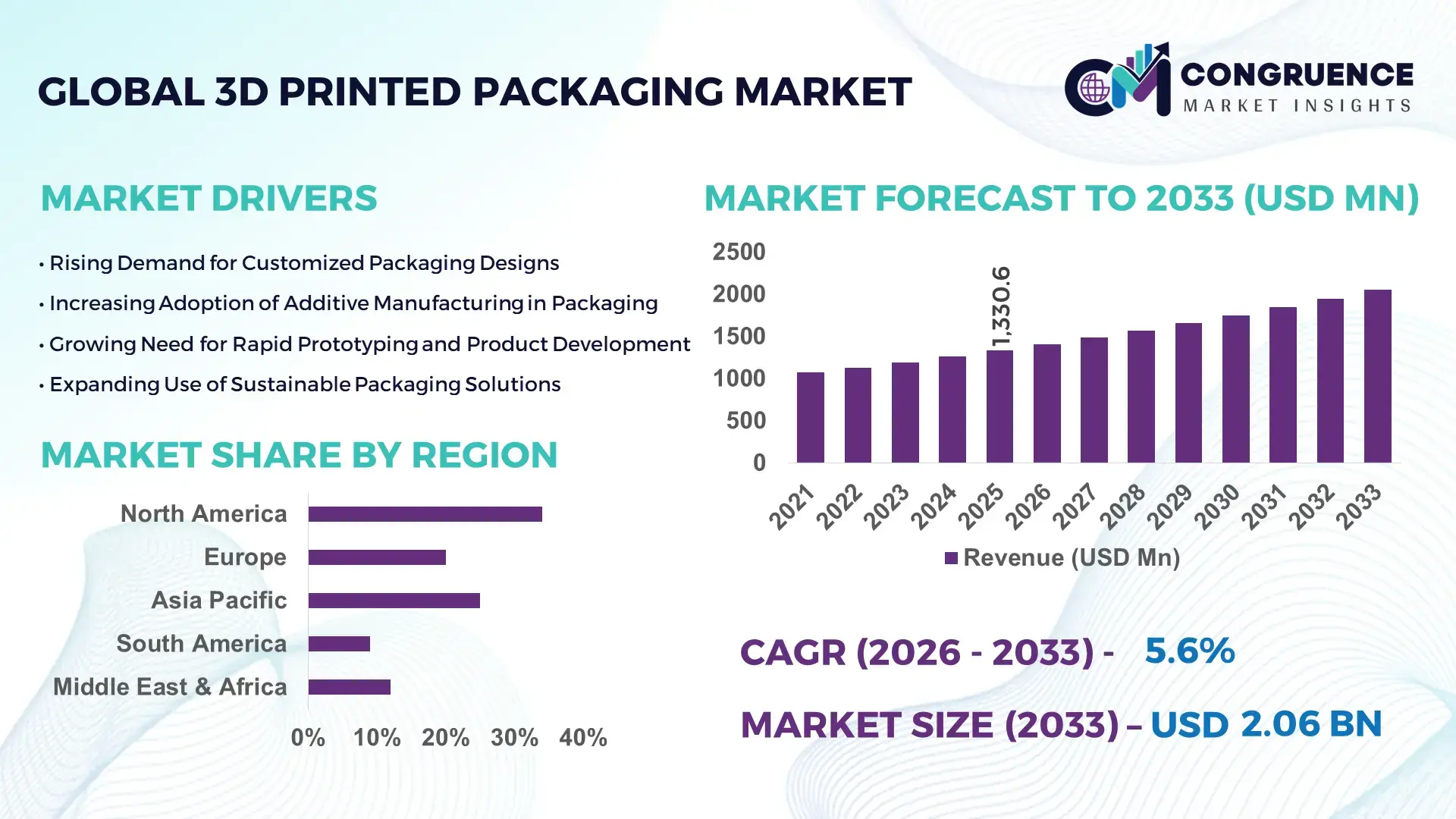

The Global 3D Printed Packaging Market was valued at USD 1330.56 Million in 2025 and is anticipated to reach a value of USD 2057.5 Million by 2033 expanding at a CAGR of 5.6% between 2026 and 2033. The market is expanding due to the rising need for customizable, lightweight, and sustainable packaging solutions across multiple industries including consumer goods, pharmaceuticals, and electronics.

The United States represents a leading hub for 3D printed packaging innovation, supported by extensive additive manufacturing infrastructure and strong industrial adoption. The country hosts more than 2,500 industrial-grade additive manufacturing facilities, with over 35% actively developing packaging prototypes and functional packaging components. Major consumer goods manufacturers in the U.S. are increasingly using 3D printing to create lightweight packaging structures that reduce material usage by nearly 20% while improving structural durability. In addition, approximately 42% of packaging design firms in North America now utilize 3D printing for rapid prototyping and short-run customized packaging production. The U.S. also accounts for a substantial portion of global additive manufacturing patents related to packaging materials and structural packaging optimization technologies.

• Market Size & Growth: The global 3D printed packaging market was valued at USD 1330.56 million in 2025 and is projected to reach USD 2057.5 million by 2033, expanding at a CAGR of 5.6% due to increasing adoption of additive manufacturing for customized and lightweight packaging solutions.

• Top Growth Drivers: 38% growth in demand for sustainable packaging, 31% increase in customized packaging adoption by consumer brands, and 27% improvement in manufacturing efficiency using additive production techniques.

• Short-Term Forecast: By 2028, advanced additive manufacturing technologies are expected to reduce packaging prototyping costs by nearly 22% while improving production speed by approximately 18%.

• Emerging Technologies: Multi-material additive manufacturing, AI-assisted packaging design optimization, and bio-based 3D printable polymers are emerging as key innovations transforming the packaging industry.

• Regional Leaders: North America is expected to reach nearly USD 720 million by 2033 driven by strong R&D investments; Europe is projected to approach USD 610 million supported by sustainable packaging regulations; Asia-Pacific is forecast to exceed USD 540 million with rapid manufacturing expansion and consumer goods production.

• Consumer/End-User Trends: Consumer electronics, cosmetics, and premium beverage industries account for over 48% of early adoption as brands seek highly customized and visually distinctive packaging formats.

• Pilot or Case Example: In 2024, a European packaging manufacturer implemented automated 3D printed packaging tooling that reduced production setup time by 30% and improved prototype development cycles by 25%.

• Competitive Landscape: The market leader holds approximately 17% share, followed by major competitors including additive manufacturing technology firms and specialized packaging design providers operating globally.

• Regulatory & ESG Impact: Over 60% of packaging manufacturers are integrating recyclable or biodegradable 3D printing materials to comply with emerging sustainability standards and circular economy regulations.

• Investment & Funding Patterns: Global investments in additive manufacturing technologies exceeded USD 2.5 billion in recent years, with significant capital flowing into packaging-focused 3D printing startups and material development companies.

• Innovation & Future Outlook: Advancements in digital manufacturing, topology optimization, and smart packaging structures are expected to redefine packaging design capabilities and enable scalable mass customization in global supply chains.

Across the global packaging ecosystem, sectors such as cosmetics, pharmaceuticals, food & beverage, and electronics represent significant contributors to the 3D printed packaging market. Consumer goods and cosmetics together account for nearly 40% of experimental packaging applications, particularly for limited-edition product packaging and rapid design prototyping. Technological innovations including biodegradable printable polymers, lattice-structured packaging for enhanced protection, and lightweight design algorithms are transforming product packaging formats. Regulatory pressures encouraging recyclable materials and reduced plastic waste are also accelerating adoption. Europe has witnessed increased demand for eco-friendly packaging designs, while Asia-Pacific manufacturing hubs are rapidly integrating additive manufacturing to support flexible packaging development and faster product launches.

The strategic relevance of the 3D Printed Packaging Market is growing rapidly as manufacturers seek flexible, cost-efficient, and sustainable packaging solutions that can adapt to modern supply chain demands. Additive manufacturing technologies are enabling packaging designers to create highly customized structures, lightweight packaging formats, and optimized protective geometries that traditional manufacturing methods cannot easily achieve. As industries increasingly emphasize product differentiation and sustainable packaging materials, the adoption of 3D printed packaging continues to expand across sectors including cosmetics, healthcare, electronics, and consumer goods. Advanced additive manufacturing systems now enable packaging manufacturers to produce complex packaging prototypes with significantly reduced development timelines. For example, digital packaging design platforms combined with additive manufacturing deliver nearly 35% improvement in design efficiency compared to traditional injection-mold prototyping methods. This capability allows companies to accelerate packaging development cycles while minimizing tooling expenses and reducing material waste during early production stages.

Regional adoption patterns also highlight the evolving structure of the market. North America dominates in production volume, supported by strong industrial infrastructure and additive manufacturing research facilities, while Europe leads in adoption with nearly 44% of packaging design enterprises integrating additive manufacturing for sustainable packaging innovation. Meanwhile, Asia-Pacific manufacturing hubs are rapidly scaling pilot projects focused on flexible packaging customization for consumer products. In the short term, technological convergence will continue to reshape packaging innovation. By 2028, AI-assisted generative design systems are expected to improve packaging material efficiency by approximately 28%, enabling manufacturers to reduce packaging weight while maintaining structural strength and product protection. In 2024, a European consumer goods company successfully deployed additive manufacturing-based packaging prototypes that reduced design iteration time by nearly 32% through AI-enabled packaging simulation tools, demonstrating the operational efficiency benefits of digital packaging production.

The growing demand for highly customized and lightweight packaging solutions is a major factor accelerating the adoption of 3D printed packaging technologies. Brands across cosmetics, luxury goods, and consumer electronics sectors increasingly seek unique packaging designs that enhance product visibility and customer experience. Traditional packaging manufacturing processes often require expensive molds and extended production timelines, whereas additive manufacturing allows rapid production of customized packaging prototypes and small-batch packaging components. Studies indicate that additive manufacturing techniques can reduce packaging material usage by approximately 20–30% through optimized structural design. In addition, packaging development cycles can be shortened by nearly 40% when using digital design and additive manufacturing systems. The cosmetics industry has particularly embraced 3D printed packaging for limited-edition product launches and personalized packaging designs. As global consumer brands continue to prioritize design differentiation and sustainable packaging materials, additive manufacturing is becoming an increasingly valuable solution for producing innovative packaging structures that balance aesthetics, functionality, and environmental responsibility.

Despite its technological advantages, the 3D printed packaging market faces constraints due to the relatively high cost of industrial additive manufacturing equipment and limited availability of specialized printable packaging materials. Industrial-grade additive manufacturing systems can cost between USD 100,000 and USD 500,000 depending on the technology and production capacity. This significant capital investment makes adoption challenging for small and medium-sized packaging manufacturers. Additionally, not all packaging-grade materials are compatible with additive manufacturing processes, limiting the range of applications that can be commercially scaled. For instance, food-grade and pharmaceutical-grade packaging materials require strict compliance with safety regulations, and many current printable polymers still require extensive certification before widespread adoption. Production speed is another constraint, as additive manufacturing is generally slower than high-volume conventional packaging manufacturing methods such as injection molding or thermoforming. These technical and economic limitations currently restrict the widespread use of 3D printed packaging primarily to prototyping, specialized packaging designs, and short-run production applications.

The global shift toward environmentally sustainable packaging materials presents significant growth opportunities for the 3D printed packaging market. Governments and regulatory bodies across multiple regions are implementing strict policies aimed at reducing plastic waste and encouraging recyclable or biodegradable packaging solutions. Additive manufacturing technologies provide the flexibility to experiment with innovative material formulations including plant-based polymers, recycled plastics, and biodegradable composites. Research initiatives have already demonstrated that certain bio-based printable materials can reduce packaging carbon footprints by nearly 35% compared to conventional petroleum-based plastics. Additionally, additive manufacturing enables precise material deposition, minimizing waste generated during production. This efficiency is particularly beneficial for companies pursuing circular economy strategies. Consumer goods manufacturers are increasingly exploring 3D printed packaging to develop eco-friendly packaging formats that use less raw material while maintaining product protection. As sustainability targets intensify globally, additive manufacturing technologies are expected to play a crucial role in enabling environmentally responsible packaging innovation.

Regulatory compliance and scalability issues remain key challenges affecting the large-scale adoption of 3D printed packaging technologies. Packaging used in food, pharmaceuticals, and healthcare products must comply with strict safety and material certification standards to ensure consumer protection. Many emerging 3D printing materials are still undergoing regulatory evaluation, which can delay their commercial deployment. Furthermore, additive manufacturing systems are generally optimized for prototyping and small-scale production rather than high-volume manufacturing. Large packaging manufacturers often produce millions of units daily using high-speed molding equipment, while additive manufacturing production rates remain comparatively lower. Scaling additive production to meet global packaging demand requires significant technological improvements in printer speed, automation, and material processing efficiency. Supply chain integration also presents a challenge, as many packaging production facilities are designed around traditional manufacturing systems. Addressing these technological and regulatory barriers will be essential for enabling broader commercialization of 3D printed packaging solutions across global industries.

• Rapid Adoption of Lightweight Lattice Packaging Structures:

Advanced lattice and topology-optimized packaging structures are becoming increasingly popular in the 3D Printed Packaging market as companies aim to reduce material usage while maintaining structural strength. Studies indicate that lattice-based packaging designs can reduce raw material consumption by nearly 28% while maintaining 95% structural durability compared with traditional molded packaging formats. Approximately 41% of industrial packaging design laboratories are now experimenting with topology-optimized geometries to create shock-resistant packaging solutions for fragile electronics and pharmaceutical products. Additionally, additive manufacturing allows the creation of internal support networks that enhance product protection while lowering overall packaging weight by nearly 18%, improving logistics efficiency and reducing shipping costs. These lightweight packaging innovations are particularly valuable for e-commerce and global supply chains where transportation efficiency is critical.

• Expansion of Sustainable and Bio-Based Printable Materials:

Sustainability initiatives are accelerating the adoption of biodegradable and recycled materials compatible with additive manufacturing technologies. Nearly 46% of packaging innovation projects now focus on developing bio-based printable polymers derived from corn starch, sugarcane, and cellulose fibers. Several packaging manufacturers have reported that bio-polymer 3D printing materials can reduce lifecycle carbon emissions by up to 32% compared with petroleum-based plastics. In addition, more than 35% of new packaging design prototypes launched by consumer goods companies in 2024 incorporated recyclable or compostable 3D printed materials. Increasing regulatory pressure on single-use plastics is also pushing packaging companies to invest in recyclable additive manufacturing materials that support circular economy initiatives.

• Integration of AI-Driven Packaging Design Platforms:

Artificial intelligence is increasingly integrated with additive manufacturing to optimize packaging designs and reduce development cycles. AI-assisted generative design software has demonstrated the ability to improve packaging material efficiency by approximately 25% and reduce prototype development time by nearly 30%. Around 39% of packaging engineering teams in advanced manufacturing regions now utilize machine-learning design tools to test thousands of structural variations before physical production. These tools allow engineers to simulate stress resistance, product protection, and stacking performance digitally, significantly lowering the number of physical prototypes required during packaging development while improving design accuracy and material efficiency.

• Rise of On-Demand and Localized Packaging Production:

On-demand manufacturing is transforming packaging supply chains as additive manufacturing enables localized production close to distribution centers. Industry analysis indicates that approximately 34% of packaging prototypes are now produced through distributed additive manufacturing networks rather than centralized facilities. This approach can reduce packaging production lead times by nearly 40% and minimize transportation requirements by 20–25%. Consumer electronics and luxury cosmetics brands have particularly embraced on-demand packaging production to support limited-edition product launches and personalized packaging designs, enabling faster market entry and greater product differentiation.

The 3D Printed Packaging Market is segmented based on type, application, and end-user industries, each contributing uniquely to the evolving market landscape. Product type segmentation includes plastic-based packaging, metal-based packaging, paper-based additive packaging formats, and bio-material packaging solutions. Plastic materials currently dominate due to their compatibility with most additive manufacturing technologies and their ability to support complex structural designs. From an application perspective, consumer goods and cosmetics packaging account for a significant portion of demand because companies in these sectors frequently launch customized or limited-edition packaging formats that benefit from rapid prototyping capabilities. Electronics and healthcare packaging applications are also expanding due to the need for highly protective and lightweight packaging structures. End-user segmentation highlights strong adoption among consumer product manufacturers, pharmaceutical companies, and electronics producers that require rapid packaging development and flexible production capabilities. Sustainability regulations, digital manufacturing adoption, and increasing demand for customized product presentation are shaping the segmentation structure of the global 3D printed packaging market.

Plastic-based 3D printed packaging represents the leading product type in the market, accounting for approximately 48% of total adoption due to its strong compatibility with additive manufacturing processes such as fused deposition modeling and selective laser sintering. Plastic materials offer flexibility, lightweight properties, and design versatility, making them suitable for customized packaging components and rapid prototyping. Thermoplastics including PLA, ABS, and PETG are widely used because they support complex geometries while maintaining sufficient mechanical strength for protective packaging applications. Metal-based 3D printed packaging structures represent a smaller but specialized segment with nearly 19% adoption, primarily used in high-value industrial and electronics packaging where durability and thermal resistance are essential. However, bio-material packaging solutions are emerging as the fastest-growing segment with an expected CAGR of about 8.2%, driven by increasing demand for environmentally sustainable packaging alternatives. Bio-based polymers and cellulose-derived printable materials are gaining traction among companies seeking recyclable and biodegradable packaging solutions. Paper-based additive packaging formats and hybrid composite materials together account for approximately 33% of the market, offering niche applications such as lightweight protective inserts and sustainable packaging prototypes.

Consumer goods packaging represents the dominant application segment within the 3D Printed Packaging market, accounting for approximately 37% of total usage, driven by the growing need for visually distinctive and customized packaging designs. Brands in cosmetics, luxury retail, and premium beverages frequently utilize additive manufacturing to produce limited-edition packaging designs, promotional packaging components, and rapid product launch prototypes. The flexibility offered by additive manufacturing allows companies to create complex packaging structures that enhance product presentation while reducing material waste. Electronics packaging accounts for nearly 24% of adoption, mainly due to the requirement for highly protective and lightweight packaging solutions that safely transport delicate electronic components. However, pharmaceutical and healthcare packaging is emerging as the fastest-growing application with an estimated CAGR of around 7.9%, supported by the demand for precision packaging designs that protect temperature-sensitive medicines and diagnostic equipment. Food and beverage packaging prototypes, industrial packaging inserts, and specialty packaging applications collectively represent approximately 39% of the remaining market share. These segments benefit from additive manufacturing’s ability to produce customized protective geometries and packaging structures for specialized products.

Consumer goods manufacturers represent the largest end-user segment in the 3D Printed Packaging market, accounting for nearly 36% of total industry adoption. Companies in cosmetics, personal care, and luxury retail sectors rely on additive manufacturing to create innovative packaging designs that differentiate their products in competitive retail environments. Approximately 44% of premium cosmetic brands have integrated additive manufacturing into their packaging design process to accelerate prototype development and create distinctive packaging formats. The pharmaceutical industry is the fastest-growing end-user segment with an estimated CAGR of approximately 8.1%, driven by the need for precision packaging solutions capable of protecting temperature-sensitive drugs, medical devices, and diagnostic products. Additive manufacturing enables pharmaceutical companies to design customized protective packaging structures that improve product safety during transportation. Electronics manufacturers, industrial equipment producers, and food and beverage companies collectively represent about 64% of the remaining end-user adoption, utilizing 3D printed packaging mainly for protective packaging inserts, prototype components, and customized packaging development.

Region North America accounted for the largest market share at 34% in 2025 however, Region Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.4% between 2026 and 2033.

North America maintains a strong position due to the presence of advanced additive manufacturing infrastructure and a high concentration of packaging technology companies. Approximately 45% of industrial packaging prototyping facilities in the region have adopted additive manufacturing solutions for rapid packaging design. Europe represents the second-largest regional market with nearly 29% share, driven by sustainability regulations and strong adoption of eco-friendly packaging materials. Asia-Pacific currently holds approximately 26% of the global market, supported by expanding manufacturing capabilities and growing e-commerce logistics networks across China, Japan, and India. South America contributes nearly 6% of the global market, largely supported by consumer goods packaging demand in Brazil and Argentina. Meanwhile, the Middle East & Africa region accounts for around 5% of total adoption, with increasing investment in advanced manufacturing technologies and packaging innovation initiatives across industrial sectors.

How is advanced digital manufacturing transforming packaging innovation and supply chain efficiency?

North America accounts for approximately 34% of global 3D Printed Packaging market adoption, supported by strong industrial research capabilities and early adoption of additive manufacturing technologies. The United States and Canada represent the primary markets where consumer goods manufacturers, pharmaceutical companies, and electronics producers utilize 3D printing for packaging prototyping and customized packaging components. Nearly 42% of packaging R&D laboratories in the region now incorporate additive manufacturing tools for packaging design optimization and rapid product development cycles. Government initiatives encouraging advanced manufacturing technologies are also supporting market expansion. Several national manufacturing programs have allocated funding to support digital manufacturing infrastructure, with more than 1,200 manufacturing innovation facilities integrating additive production technologies. Technological advancements such as AI-assisted packaging design, topology optimization, and bio-based printable materials are widely explored within the region.mLocal companies are increasingly experimenting with on-demand packaging manufacturing models. For instance, a major additive manufacturing technology provider based in the United States has introduced packaging-specific design software capable of reducing material waste by up to 25% during structural packaging design. Consumer behavior in the region also supports market growth. Enterprises across healthcare, electronics, and luxury retail sectors demonstrate high adoption levels for customized packaging formats that enhance brand differentiation and improve logistics protection.

Why are sustainability mandates accelerating the transition toward advanced packaging design technologies?

Europe accounts for nearly 29% of the global 3D Printed Packaging market, driven by strong environmental regulations and a growing focus on sustainable packaging development. Germany, the United Kingdom, and France represent the largest markets, collectively accounting for more than 60% of regional packaging innovation activities. These countries maintain extensive additive manufacturing research ecosystems supporting new packaging materials and structural design innovations. Strict environmental policies aimed at reducing plastic waste are accelerating the adoption of recyclable and biodegradable 3D printed packaging materials. Nearly 48% of packaging innovation programs across European manufacturing hubs are focused on developing sustainable packaging prototypes compatible with additive manufacturing technologies. The European packaging industry also emphasizes circular economy strategies that encourage recyclable material usage and reduced packaging waste. Technological advancements such as multi-material additive printing and generative design software are increasingly used to develop lightweight and optimized packaging structures. Several European manufacturing clusters have also invested in digital production laboratories dedicated to additive manufacturing applications. Regional consumer behavior plays an important role in shaping market demand. Companies operating in this region prioritize transparency and sustainability, resulting in higher adoption of packaging technologies capable of supporting recyclable materials and environmentally responsible packaging solutions.

How is rapid manufacturing expansion reshaping next-generation packaging development?

Asia-Pacific ranks among the fastest-growing regions in the 3D Printed Packaging market and currently accounts for approximately 26% of global adoption. China, Japan, and India represent the largest consuming markets due to their extensive manufacturing sectors and expanding consumer product industries. China alone contributes nearly 38% of regional additive manufacturing production capacity, making it a significant hub for packaging innovation. Manufacturing infrastructure across the region continues to expand rapidly, with more than 4,500 additive manufacturing facilities operating across Asia-Pacific industrial zones. Countries such as Japan and South Korea are leading technological innovation in high-precision additive manufacturing systems designed for complex packaging components. Regional innovation hubs are increasingly focusing on digital manufacturing integration, AI-driven packaging design, and eco-friendly packaging materials. Several technology parks and manufacturing incubators across Asia-Pacific are actively supporting research into biodegradable printable polymers and lightweight packaging structures. A notable example involves a leading Japanese manufacturing company that introduced an automated additive manufacturing packaging system capable of reducing packaging development cycles by 28% while improving structural packaging performance. Consumer behavior in the region is also strongly influenced by e-commerce expansion. Rapid growth in online retail and logistics networks has increased demand for durable, lightweight packaging solutions that can protect products during long-distance transportation.

What factors are driving modernization of packaging manufacturing capabilities?

South America holds approximately 6% of the global 3D Printed Packaging market, with Brazil and Argentina serving as the primary markets within the region. Brazil alone represents nearly 52% of regional packaging innovation activities, largely supported by its expanding consumer goods manufacturing sector and strong demand for customized packaging formats. Infrastructure modernization within manufacturing facilities is encouraging the adoption of advanced production technologies including additive manufacturing systems. Several packaging manufacturers in Brazil have introduced digital prototyping laboratories that allow companies to develop packaging prototypes in significantly shorter timeframes. Government programs promoting industrial innovation and advanced manufacturing technologies have also supported market development. Regional trade initiatives aimed at strengthening manufacturing competitiveness have resulted in increased adoption of automated packaging design systems and additive manufacturing equipment. Local packaging design firms are experimenting with additive manufacturing to create specialized packaging inserts for fragile products and electronics components. A Brazilian packaging technology startup recently demonstrated a packaging design platform capable of reducing material usage by 18% through optimized additive manufacturing structures. Consumer behavior across the region is strongly tied to product localization and brand identity, particularly within consumer goods and beverage industries where packaging design plays a significant role in product differentiation.

How is industrial diversification influencing packaging innovation across emerging markets?

The Middle East & Africa region accounts for approximately 5% of the global 3D Printed Packaging market, with increasing adoption of advanced manufacturing technologies across several industrial sectors. The United Arab Emirates and South Africa represent the leading markets within the region, supported by government initiatives aimed at diversifying industrial economies and strengthening manufacturing capabilities. Several technology development programs in the region focus on integrating additive manufacturing into production ecosystems. For example, industrial innovation strategies in the United Arab Emirates encourage the adoption of advanced manufacturing technologies, including additive manufacturing systems used for industrial packaging prototypes. Demand for customized packaging solutions is increasing across sectors such as consumer electronics, luxury retail, and industrial equipment manufacturing. These industries often require protective packaging formats designed to withstand long-distance transportation across international supply chains. Regional manufacturing facilities are also experimenting with digital design platforms and additive manufacturing equipment to accelerate packaging product development cycles. A manufacturing technology hub in the Gulf region recently introduced a collaborative research initiative exploring lightweight additive packaging designs capable of improving transportation efficiency by 20%.

• United States – 31% share in the 3D Printed Packaging market, supported by strong additive manufacturing infrastructure, extensive packaging R&D capabilities, and high adoption among consumer goods and healthcare manufacturers.

• China – 24% share in the 3D Printed Packaging market, driven by large-scale manufacturing capacity, expanding e-commerce logistics networks, and rapid investment in industrial additive manufacturing technologies.

The 3D Printed Packaging market is characterized by a moderately fragmented competitive landscape consisting of additive manufacturing technology providers, specialized packaging design companies, and material innovation firms. More than 120 active companies operate globally within this market ecosystem, developing advanced packaging technologies based on additive manufacturing systems, digital design platforms, and innovative printable materials.

The top five companies collectively account for approximately 38% of the global market presence, indicating moderate concentration with strong competition among technology innovators and packaging manufacturers. Industry participants are increasingly focusing on strategic partnerships, joint research initiatives, and technology collaborations to expand their packaging capabilities. Over 60 new product developments related to additive packaging materials and packaging design software were introduced between 2023 and 2025.

Innovation remains a key competitive differentiator within the market. Companies are investing heavily in bio-based printable materials, multi-material additive manufacturing systems, and AI-assisted packaging design technologies. Approximately 44% of leading packaging technology companies now maintain dedicated additive manufacturing research laboratories focused on packaging innovation.

Stratasys Ltd.

3D Systems Corporation

Materialise NV

EOS GmbH

HP Inc.

Protolabs Inc.

Carbon, Inc.

Desktop Metal, Inc.

Sculpteo

Formlabs Inc.

Ultimaker BV

EnvisionTEC GmbH

Technological innovation in the 3D Printed Packaging market is largely driven by advancements in additive manufacturing systems, digital design platforms, and next-generation material engineering. Industrial additive manufacturing technologies such as fused deposition modeling (FDM), selective laser sintering (SLS), and multi-jet fusion (MJF) are widely used to develop packaging prototypes and customized packaging components with complex geometries. Among these, FDM accounts for nearly 45% of packaging prototyping applications due to its compatibility with multiple thermoplastic materials and relatively low operational cost. Selective laser sintering has also gained traction for producing highly durable packaging inserts and structural components capable of withstanding mechanical stress during transportation.

Multi-material 3D printing is emerging as a critical technology for packaging innovation, allowing manufacturers to combine flexible and rigid materials within a single structure. This capability enables the production of shock-absorbing packaging components that improve product protection. Studies show that multi-material packaging structures can increase protective performance by nearly 30% compared with single-material packaging formats. Additionally, advanced topology optimization software is enabling engineers to create lattice-based packaging structures that reduce material usage by approximately 25% while maintaining mechanical strength.

Artificial intelligence and generative design platforms are also transforming packaging development workflows. AI-driven design tools can analyze thousands of structural variations and simulate stress performance digitally, reducing packaging prototype development cycles by nearly 35%. Around 38% of packaging engineering teams in advanced manufacturing regions have already integrated AI-assisted design software into their additive manufacturing processes.

Material innovation represents another major technological driver within the market. Research initiatives are focusing on biodegradable polymers, recycled plastic filaments, and cellulose-based printable materials that support sustainable packaging strategies. Bio-based polymers used in additive manufacturing can reduce packaging carbon emissions by nearly 30% compared with petroleum-based plastics. Additionally, advancements in high-speed industrial 3D printing systems have increased production efficiency, enabling packaging manufacturers to produce multiple packaging components simultaneously and improve operational throughput by nearly 20%.

• In March 2024, Stratasys launched the F3300 industrial FDM 3D printer designed for high-volume manufacturing environments. The system offers build speeds up to 2 times faster than previous models and improved material throughput, enabling packaging designers to accelerate the development of complex and lightweight packaging prototypes. Source: www.stratasys.com

• In May 2024, HP expanded its Multi Jet Fusion ecosystem with new automation and materials capabilities designed to support industrial applications, including packaging tooling and structural packaging prototypes. The enhanced platform improved production efficiency by enabling continuous manufacturing workflows and advanced material recycling features. Source: www.hp.com

• In September 2024, Materialise introduced upgraded simulation software within its Magics platform, allowing packaging designers to optimize additive manufacturing workflows and reduce material consumption by up to 20% when designing complex packaging geometries. The software also improves build preparation speed and production reliability. Source: www.materialise.com

• In February 2025, BASF Forward AM expanded its portfolio of sustainable additive manufacturing materials with new recyclable polymer filaments designed for industrial applications including packaging prototyping and lightweight packaging components, supporting manufacturers pursuing circular packaging strategies.

The 3D Printed Packaging Market Report provides a comprehensive evaluation of the global industry landscape, focusing on technological innovation, material advancements, and the growing integration of additive manufacturing in packaging design and production. The report examines multiple packaging types including plastic-based, metal-based, paper-based, and bio-material packaging formats that are compatible with industrial additive manufacturing systems. Plastic-based materials currently represent a substantial portion of additive manufacturing applications due to their versatility, lightweight properties, and compatibility with several 3D printing technologies.

From an application perspective, the report analyzes major packaging uses across consumer goods, electronics, pharmaceutical products, food and beverage packaging prototypes, and industrial packaging inserts. Consumer goods and cosmetics packaging together account for a significant portion of additive manufacturing experimentation due to the demand for customized packaging designs and rapid product launch cycles. Electronics and pharmaceutical packaging applications are also highlighted due to their need for protective and highly precise packaging structures.

The geographic scope of the report covers key regions including North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. Each regional analysis evaluates manufacturing infrastructure, packaging innovation trends, industrial adoption patterns, and evolving regulatory frameworks affecting packaging materials and sustainability practices. Major packaging manufacturing hubs in the United States, Germany, China, and Japan are examined due to their strong additive manufacturing ecosystems.

Technological coverage within the report includes additive manufacturing methods such as fused deposition modeling, selective laser sintering, stereolithography, and multi-jet fusion systems. The report also explores emerging technologies including AI-assisted packaging design platforms, multi-material additive manufacturing, topology optimization software, and biodegradable printable polymers that are reshaping packaging innovation.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

5.6% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Stratasys Ltd., 3D Systems Corporation, Materialise NV, EOS GmbH, HP Inc., Protolabs Inc., Carbon, Inc., Desktop Metal, Inc., Sculpteo, Formlabs Inc., Ultimaker BV, EnvisionTEC GmbH |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |