Reports

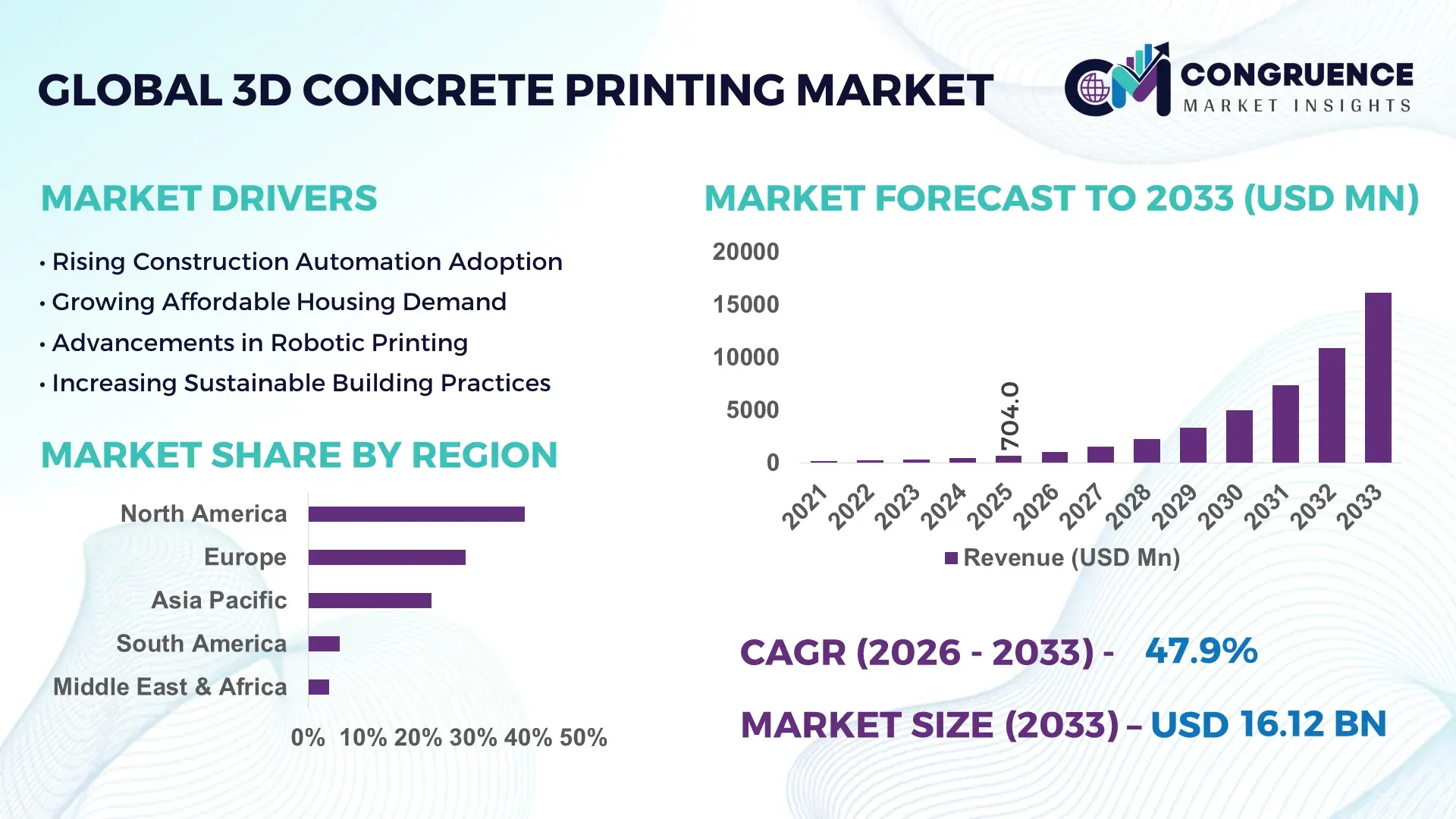

The Global 3D Concrete Printing Market was valued at USD 704.0 Million in 2025 and is anticipated to reach a value of USD 16,118.3 Million by 2033 expanding at a CAGR of 47.9% between 2026 and 2033. Rapid infrastructure digitization, labor shortages in construction, and accelerated adoption of automated additive manufacturing for affordable housing projects are driving sustained market expansion.

The United States leads the global market with approximately 34% share, supported by federal infrastructure modernization initiatives, defense construction programs, and more than 150 active research and commercial projects integrating robotic concrete printing. Compared with Germany, where industrial automation adoption exceeds 22% across advanced construction applications, the U.S. benefits from larger-scale commercial deployment and stronger private investment following the Infrastructure Investment and Jobs Act.

Organizations investing in automated construction capabilities, localized material innovation, and digital project execution will secure stronger long-term competitive positioning across high-value infrastructure projects.

Market Size & Growth: USD 704.0 Million (2025) to USD 16,118.3 Million (2033) at 47.9% CAGR, driven by automated construction technologies and digital infrastructure modernization.

Top Growth Drivers: Construction labor shortages (35%+), material waste reduction up to 60%, and project completion time lowered by nearly 50%.

Short-Term Forecast: By 2028, printing efficiency improves over 40% while on-site labor requirements decline by approximately 30%.

Emerging Technologies: AI-assisted design, robotic automation, and low-carbon printable concrete enhance precision, scalability, and structural performance.

Regional Leaders: North America exceeds USD 5.6 Billion, Europe approaches USD 4.4 Billion, and Asia-Pacific surpasses USD 4.8 Billion through smart infrastructure expansion.

Consumer/End-User Trends: More than 45% of pilot housing developments incorporate automated concrete printing for faster, sustainable project execution.

Pilot/Case Example: In 2024, multiple affordable housing projects achieved nearly 55% faster construction schedules while reducing material waste by over 50%.

Competitive Landscape: COBOD holds approximately 18% global market presence alongside ICON, CyBe Construction, Apis Cor, and PERI through continuous technology expansion.

Regulatory & ESG Impact: Low-carbon construction initiatives reduce concrete waste by up to 60%, aligning with stricter sustainability regulations across major economies.

Investment & Funding: More than USD 1.2 Billion supports strategic partnerships, manufacturing expansion, and advanced robotic construction platforms amid global supply-chain diversification.

Innovation & Future Outlook: AI-enabled autonomous printing, digital twins, and sustainable printable materials are accelerating industrial-scale deployment and competitive differentiation.

The 3D Concrete Printing Market is transforming construction across residential housing, commercial buildings, defense infrastructure, and disaster-relief projects through automated fabrication and low-carbon material innovations. AI-enabled design optimization, robotic printing systems, and advanced cement formulations continue improving build quality and resource efficiency, while printable geopolymer materials gain momentum. More than 60% of leading solution providers are expanding sustainable material portfolios as governments increasingly prioritize resilient infrastructure and localized construction supply chains, setting the stage for broader strategic adoption.

The 3D Concrete Printing Market has become strategically important as construction companies seek greater productivity, resilient supply chains, and digitally enabled project execution. Infrastructure modernization programs, affordable housing initiatives, and increasing labor shortages are accelerating the transition toward automated construction methods. At the same time, stricter sustainability standards are encouraging contractors to reduce material consumption and carbon-intensive building practices through precision manufacturing.

Compared with conventional concrete construction, advanced 3D printing systems reduce material waste by up to 60% while shortening project timelines by nearly 50%, creating measurable operational advantages. North America leads large-scale commercial deployment through infrastructure investments and technology commercialization, whereas Europe emphasizes sustainable construction materials and regulatory compliance. Asia-Pacific continues expanding deployment across urban development projects supported by rapid industrialization and smart city investments.

Commercial deployment is increasingly visible in affordable housing developments, defense facilities, and industrial infrastructure where robotic printing minimizes labor dependency and improves construction consistency. Leading companies are expanding regional manufacturing, forming partnerships with material suppliers, and investing in AI-enabled construction software to strengthen deployment capabilities. Over the next two to three years, broader integration with digital construction workflows and sustainable printable materials will reinforce competitive differentiation, improve operational resilience, and establish automated construction as a core capability for next-generation infrastructure development.

Construction labor shortages, infrastructure modernization, and digital fabrication are fundamentally reshaping the adoption of 3D concrete printing. Automated printing systems reduce material waste by up to 60%, shorten project completion times by nearly 50%, and lower manual labor requirements by approximately 70% on selected structural applications. In the United States, federal infrastructure investments and affordable housing initiatives are accelerating commercial deployment, while stricter sustainability targets encourage precision-based construction. This structural shift improves project predictability and reduces lifecycle costs, prompting technology providers to expand robotic printing capacity, establish material partnerships, and develop AI-enabled design software. A notable strategic outcome is the transition from pilot-scale demonstrations toward standardized industrial construction workflows capable of supporting high-volume residential and public infrastructure projects.

High capital expenditure for industrial-scale printers and inconsistent availability of certified printable concrete continue limiting widespread deployment. Industrial 3D concrete printing systems often require investments exceeding conventional equipment by 40–60%, while specialized printable materials can increase project input costs by nearly 25%. In Germany, varying national construction standards and certification requirements complicate cross-border commercialization and delay project approvals. These structural barriers restrict scalability, particularly for mid-sized contractors lacking dedicated digital construction expertise. To reduce operational exposure, manufacturers are localizing material production, negotiating long-term supply agreements, and introducing modular printer platforms with lower ownership costs. Companies focusing on standardized printable material ecosystems gain stronger deployment consistency and improved commercial competitiveness.

Next-generation sustainable construction materials and intelligent automation present significant commercial opportunities beyond conventional building applications. Printable geopolymer concrete can reduce embodied carbon by approximately 40%, while AI-driven print optimization improves material utilization by over 20% during complex structural fabrication. In Saudi Arabia, large-scale smart city developments and giga-projects are creating demand for automated construction technologies capable of accelerating infrastructure delivery. Technology providers are investing in advanced material R&D, robotic quality monitoring, and integrated digital construction platforms while expanding partnerships with cement producers and engineering firms. A key strategic opportunity lies in developing localized printable material formulations that minimize transportation dependence while meeting country-specific structural and environmental performance standards.

Commercial scalability remains constrained by fragmented construction workflows, workforce capability gaps, and integration complexity between digital design platforms and on-site operations. Industry assessments indicate that nearly 45% of contractors lack personnel experienced in robotic construction technologies, while interoperability challenges increase implementation timelines by approximately 30% for complex projects. In Japan, aging construction workforces intensify the urgency for automation, yet compliance with stringent structural safety regulations requires extensive validation before deployment. These execution challenges directly influence project consistency, operational efficiency, and long-term competitiveness. Companies must strengthen workforce training, expand digital engineering partnerships, standardize BIM-integrated construction processes, and invest in automated quality assurance systems to achieve reliable industrial-scale deployment and sustainable competitive advantage.

AI-Enabled Print Workflow Optimization: Construction firms are embedding AI-driven slicing software and automated quality monitoring into 3D concrete printing workflows, improving print accuracy by nearly 25% while reducing material waste by up to 20%. Labor shortages in the United States are accelerating deployment of autonomous printing systems, prompting technology providers to integrate real-time process monitoring and predictive maintenance into industrial construction operations.

Low-Carbon Material Adoption Expands: Printable geopolymer concrete and supplementary cementitious materials are reducing embodied carbon by approximately 40% while improving resource efficiency by over 18%. Tightening environmental regulations across Germany are encouraging suppliers to commercialize sustainable printable mixes, leading construction companies to establish long-term material partnerships and diversify regional supply networks for greater resilience.

Large-Scale Housing Deployment Accelerates: Affordable housing programs are moving beyond pilot projects into commercial deployment, with automated construction reducing project delivery times by nearly 50% and on-site labor requirements by around 65%. Contractors are restructuring project execution around modular digital construction workflows, enabling faster permitting, standardized production, and improved scheduling reliability across high-volume residential developments.

Integrated Digital Construction Ecosystems: Companies are connecting Building Information Modeling (BIM), robotic printing, and cloud-based project management platforms, improving construction coordination by over 30% and reducing rework by approximately 22%. In Saudi Arabia, smart city developments are driving integrated digital construction practices, while equipment manufacturers are expanding strategic partnerships with software developers to deliver end-to-end automated construction ecosystems rather than standalone printing hardware.

Gantry-based Systems represent the leading segment because they provide superior build volume, structural stability, and continuous printing capability for large residential and infrastructure projects. They account for approximately 52% of global installations, supported by their ability to construct multi-room structures with consistent dimensional accuracy. Construction companies favor gantry platforms due to easier integration with automated material delivery systems and Building Information Modeling (BIM), reducing project interruptions and improving operational efficiency. Manufacturers continue expanding modular gantry platforms that simplify transportation and installation across large construction sites. Robotic Arm-based Systems are the fastest-growing segment as demand rises for complex architectural designs and customized concrete components. Their deployment has increased by nearly 28% over the past two years, driven by improved motion flexibility and precision printing. Crane-based/Contour Crafting Systems remain strategically relevant for specialized infrastructure and large-scale projects where extended reach is essential despite relatively lower commercial deployment. Companies are investing in hybrid robotic platforms, AI-enabled motion control, and collaborative engineering partnerships to broaden application flexibility while improving print accuracy and project scalability.

Residential Housing dominates the market as governments and private developers prioritize affordable, rapid, and sustainable housing solutions. The segment represents nearly 46% of overall demand, supported by faster project execution, lower labor dependence, and reduced construction waste. Automated concrete printing shortens housing construction schedules by approximately 50%, encouraging developers to standardize digital construction workflows. Leading technology providers continue expanding partnerships with housing developers to commercialize turnkey printing solutions for high-volume residential projects. Public Infrastructure is the fastest-growing application as countries accelerate investment in bridges, public facilities, and disaster-resilient infrastructure. Deployment activity has increased by more than 30%, supported by digital infrastructure modernization initiatives. Commercial & Office Buildings continue adopting printed structural elements for architectural flexibility, while Industrial applications increasingly utilize automated printing for warehouses and manufacturing facilities requiring rapid expansion. Companies are strengthening software integration, robotics deployment, and material innovation to improve productivity while addressing complex structural requirements across multiple construction environments.

Construction Contractors remain the largest end-user group, accounting for approximately 38% of market demand due to their direct responsibility for project execution and equipment deployment. Growing labor shortages and productivity targets are encouraging contractors to automate repetitive construction activities while improving schedule certainty. Technology vendors are responding through equipment leasing models, operator training, and integrated software platforms that reduce implementation complexity and accelerate commercial adoption. Government & Public Sector organizations represent the fastest-growing end-user segment as national infrastructure modernization and affordable housing initiatives expand. Procurement activity has increased by nearly 27%, supported by digital construction policies and sustainability objectives. Private Real Estate Developers continue investing in faster project delivery, while Architectural & Structural Engineering Companies increasingly incorporate printable structural designs into digital planning. Prefab Producers, Educational & Research Institutions, Owners, and Others contribute through technology validation, product development, and specialized deployment projects. Companies are strengthening ecosystem partnerships, localized support networks, and application-specific solutions to improve competitiveness across diverse customer groups.

North America accounted for the largest market share at 39.4% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a 50.8% CAGRbetween 2026 and 2033.

North America maintains the leading position through early commercialization of robotic construction technologies, strong infrastructure investments, and advanced digital construction ecosystems. The region contributes approximately 39.4% of global demand, supported by increasing deployment across residential housing, defense facilities, and public infrastructure. Automated concrete printing reduces construction waste by nearly 60%, reinforcing sustainability objectives while improving project execution efficiency. Leading equipment manufacturers continue expanding regional production capacity, software integration, and material development partnerships. Growing adoption of Building Information Modeling (BIM) and robotic construction platforms is enabling contractors to standardize digital construction workflows and accelerate industrial-scale implementation.

United States Market Outlook: The United States represents the largest national market owing to extensive infrastructure modernization, federal housing initiatives, and an established ecosystem of construction technology innovators. More than 150 commercial demonstrations and pilot deployments have strengthened industry confidence in automated construction. Domestic companies continue investing in AI-enabled printing systems, localized printable concrete materials, and strategic partnerships with engineering firms to improve deployment consistency, expand commercial applications, and accelerate adoption across residential, industrial, and public infrastructure projects.

Europe remains a major innovation hub where environmental regulations and industrial automation are reshaping construction practices. The region accounts for approximately 28.6% of global market activity, supported by widespread investment in low-carbon construction materials and digitally integrated building processes. Printable geopolymer concrete adoption continues expanding as contractors pursue lower emissions and improved material efficiency. Several construction technology companies are strengthening partnerships with engineering firms and research institutions to commercialize advanced robotic construction solutions while improving compliance with evolving building standards and certification requirements.

Germany Market Outlook: Germany leads the European market through advanced manufacturing capabilities, robotics expertise, and strong engineering infrastructure. Construction firms increasingly integrate automated printing with Industry 4.0 production environments, improving workflow efficiency and quality assurance. More than 20% of advanced construction technology projects now incorporate automated fabrication or digital construction processes. Equipment suppliers continue expanding research collaborations and localized material development programs to strengthen industrial deployment while supporting sustainable construction objectives across commercial and infrastructure projects.

Asia-Pacific is emerging as the fastest-expanding regional market due to rapid urbanization, smart city investments, and increasing demand for affordable housing solutions. The region represents nearly 22.4% of current global deployment while recording the highest implementation momentum across large-scale infrastructure projects. Governments are accelerating digital construction adoption to address labor shortages and improve project delivery efficiency. Construction companies continue expanding automated production facilities, localized material supply chains, and robotic construction partnerships to support growing demand across residential, commercial, and industrial developments.

China Market Outlook: China dominates the regional landscape through its extensive construction industry, advanced manufacturing ecosystem, and continuous investment in smart infrastructure. Large domestic enterprises are integrating robotic construction technologies into prefabrication and modular building strategies to enhance productivity. Automated construction adoption has increased by approximately 30% across selected pilot developments, while ongoing investment in AI-driven construction software and printable material innovation strengthens the country's long-term competitive position within the global market.

South America is gradually adopting 3D concrete printing as governments prioritize infrastructure upgrades, affordable housing, and construction productivity improvements. The region contributes approximately 5.8% of global market activity, with adoption primarily concentrated in pilot housing developments and institutional construction projects. Limited digital construction infrastructure and skilled workforce availability continue moderating commercial deployment; however, increasing collaboration between international technology providers and regional contractors is expanding implementation opportunities. Companies are introducing modular printing systems and localized technical support to improve operational feasibility across diverse construction environments.

Brazil Market Outlook: Brazil represents the region's most strategically important market due to its large construction sector and growing demand for cost-efficient building technologies. Public housing initiatives and infrastructure modernization programs are encouraging greater evaluation of automated construction methods. Several engineering companies are partnering with international equipment suppliers to demonstrate printable housing applications capable of reducing construction time by nearly 40%, while strengthening local technical capabilities and material supply networks.

The Middle East & Africa region is becoming an important destination for advanced construction technologies through large-scale urban development, smart city initiatives, and government-backed infrastructure investments. The region accounts for roughly 3.8% of global market activity while demonstrating strong deployment potential across commercial, tourism, and residential projects. Major developers are integrating robotic construction technologies into flagship developments to improve productivity and reduce project timelines. Strategic partnerships between construction firms, technology providers, and material suppliers are accelerating localized implementation and supporting digital construction transformation.

Saudi Arabia Market Outlook: Saudi Arabia leads regional adoption through giga-project developments, smart city investments, and national economic diversification initiatives. Large-scale construction programs are incorporating automated building technologies to improve execution efficiency and support ambitious infrastructure schedules. Multiple flagship developments now evaluate robotic concrete printing for selected structural applications, while public and private investment continues expanding digital engineering capabilities, sustainable building materials, and localized technology partnerships that strengthen long-term industrial competitiveness.

The market is characterized by competition between global technology leaders such as COBOD International, ICON Technology, Apis Cor, CyBe Construction, and XtreeE, regional construction specialists, and material solution providers. The top five players collectively account for approximately 58% of the global market, reflecting moderate consolidation driven by proprietary printing platforms and software ecosystems. Competition increasingly centers on robotic precision, printing speed, and integrated material technologies rather than equipment pricing alone. Advanced gantry systems improve construction productivity by nearly 45%, while AI-assisted workflow optimization reduces material waste by up to 20% and automated quality monitoring enhances dimensional accuracy by approximately 25%. Companies compete through manufacturing expansion, strategic partnerships with cement producers, turnkey project delivery, and vertical integration across hardware, software, and printable materials. The competitive landscape is shifting toward multifunctional construction robots and digital construction platforms, increasing pressure on standalone equipment suppliers. High capital investment, certification requirements, and specialized material expertise remain significant entry barriers. Winning requires scalable technology, localized material ecosystems, strong engineering partnerships, and proven commercial deployment capability.

ICON Technology, Inc.

Apis Cor Inc.

CyBe Construction B.V.

XtreeE

Contour Crafting Corporation

Vertico B.V.

Winsun (Yingchuang Building Technique Co., Ltd.)

BetAbram d.o.o.

Hyperion Robotics Oy

SQ4D LLC

WASP S.r.l.

The market is rapidly transitioning from standalone robotic printers to integrated digital construction ecosystems. AI-assisted toolpath optimization, automated quality inspection, and Building Information Modeling (BIM) integration now improve print precision by approximately 25% while reducing project planning time by nearly 30%. Around 45% of newly deployed industrial systems incorporate cloud-enabled monitoring and remote diagnostics, enabling contractors to optimize performance across multiple construction sites. These technologies strengthen operational visibility while reducing costly design revisions.

Material innovation is becoming equally important. Printable geopolymer concrete, fiber-reinforced cementitious composites, and smart admixture technologies reduce material waste by up to 20% and lower embodied carbon by nearly 40% compared with conventional cement formulations. Compared with traditional cast-in-place construction, automated 3D printing shortens project execution by approximately 50%, providing contractors with measurable productivity and scheduling advantages. Technology leaders with proprietary software-material integration benefit most because they deliver complete construction ecosystems rather than isolated hardware.

Between 2026 and 2028, digital twins, machine learning-based process control, and multifunctional construction robots will become mainstream across commercial deployments. Companies investing in autonomous calibration, real-time structural monitoring, and localized printable material development will achieve stronger operational resilience, faster deployment, and improved project consistency. Early adopters are expected to secure competitive advantages through standardized workflows, reduced lifecycle costs, and scalable industrial construction capabilities.

July 2025 – COBOD International launched the world's first multifunctional construction robot, combining 3D concrete printing with robotic shotcrete capabilities. The platform is designed to automate over 50% of construction activities, significantly expanding industrial construction automation beyond structural printing. Business impact: strengthens COBOD's leadership in integrated construction robotics. Source: www.cobod.com

October 2025 – COBOD International announced the completion of Europe's largest 3D-printed housing project, delivering 36 student apartments in Denmark using its BOD3 construction printer. The project validates commercial-scale residential deployment and demonstrates higher construction productivity and sustainability than conventional methods. Business impact: reinforces confidence in high-volume residential applications.

July 2024 – XtreeE deployed a new construction 3D-printing unit at the U.S. National Institute of Standards and Technology (NIST) to support additive construction research and standards development. The installation expanded XtreeE's international deployment footprint while strengthening technology validation for commercial construction. Business impact: enhances standardization and industrial adoption.

2025 – Apis Cor continued expanding commercialization of its autonomous on-site robotic construction platform capable of printing buildings up to two stories directly at project sites. The company strengthened deployment of robotic construction systems focused on reducing labor dependency and accelerating project execution. Business impact: broadens adoption of autonomous construction across residential and infrastructure projects.

The report provides comprehensive coverage of the global 3D concrete printing industry across gantry-based systems, robotic arm-based systems, and crane-based systems, evaluating their deployment strategies, operational advantages, and evolving investment priorities. It analyzes applications spanning residential housing, commercial buildings, industrial facilities, and public infrastructure while assessing demand across construction contractors, government agencies, real estate developers, engineering firms, prefab producers, and research institutions. Regional assessments cover North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting deployment concentration, technology adoption, and competitive positioning.

The study further examines automation, AI-enabled construction software, robotic printing platforms, BIM integration, sustainable printable materials, and digital construction workflows. More than 45% of recent commercial deployments emphasize intelligent automation, while low-carbon printable materials continue expanding across major construction programs. The report supports strategic investment decisions, market entry planning, competitive benchmarking, partnership evaluation, technology adoption, and expansion strategies, providing actionable insights into industry transformation and emerging business opportunities through 2033.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 704.0 Million |

| Market Revenue (2033) | USD 16,118.3 Million |

| CAGR (2026–2033) | 47.9% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | COBOD International A/S; ICON Technology, Inc.; Apis Cor Inc.; CyBe Construction B.V.; XtreeE; Contour Crafting Corporation; Vertico B.V.; Winsun (Yingchuang Building Technique Co., Ltd.); BetAbram d.o.o.; Hyperion Robotics Oy; SQ4D LLC; WASP S.r.l. |

| Customization & Pricing | Available on Request (10% Customization Free) |