Reports

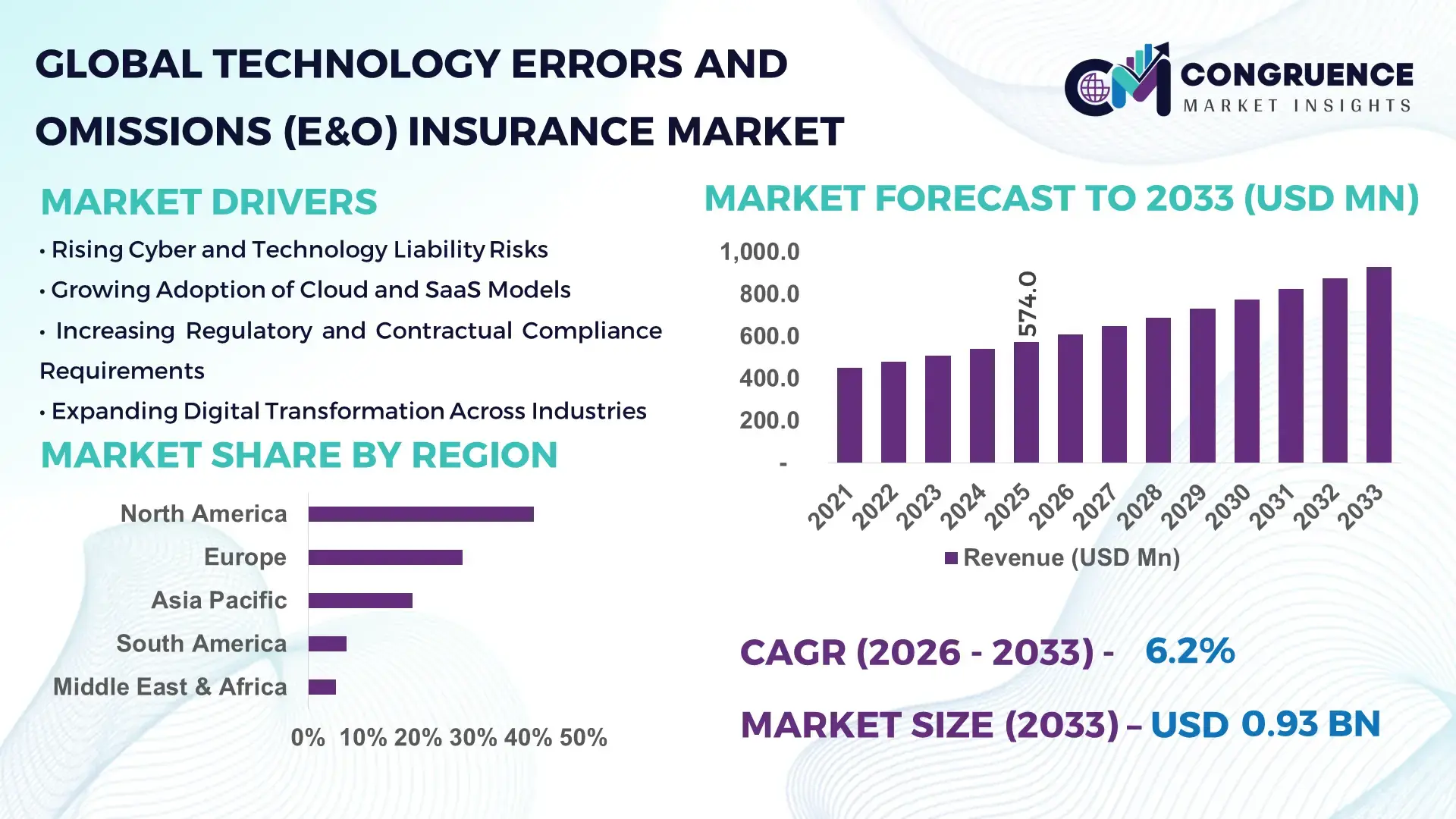

The Global Technology Errors and Omissions (E&O) Insurance Market was valued at USD 574.0 Million in 2025 and is anticipated to reach a value of USD 928.8 Million by 2033 expanding at a CAGR of 6.2% between 2026 and 2033, according to an analysis by Congruence Market Insights. The market expansion is primarily driven by rising cyber liability exposure, increasing SaaS adoption, and stricter contractual risk transfer requirements across global technology ecosystems.

The United States remains the dominant country in the Technology Errors and Omissions (E&O) Insurance Market, supported by a mature professional liability framework and strong underwriting capacity. The U.S. hosts over 33 million small businesses, with approximately 70% relying on digital infrastructure, increasing demand for technology liability coverage. More than 60% of venture-backed SaaS companies in North America purchase standalone E&O policies at early growth stages. Insurtech investment in the U.S. exceeded USD 4 billion in recent years, enhancing AI-driven underwriting, automated claims processing, and risk modeling capabilities. Additionally, large enterprise IT outsourcing contracts in the country increasingly mandate minimum E&O coverage limits ranging from USD 5 million to USD 25 million, strengthening policy uptake across cloud service providers, fintech firms, and managed IT service vendors.

Market Size & Growth: Valued at USD 574.0 Million in 2025, projected to reach USD 928.8 Million by 2033 at 6.2% CAGR, driven by a 48% rise in technology-related liability claims across cloud and SaaS providers.

Top Growth Drivers: 62% surge in SaaS adoption, 45% increase in third-party vendor risk exposure, 38% growth in cyber-regulatory compliance requirements.

Short-Term Forecast: By 2028, AI-enabled underwriting is expected to reduce claims processing time by 30% and improve risk assessment accuracy by 25%.

Emerging Technologies: AI-based risk scoring, blockchain-powered policy documentation, and parametric insurance triggers for downtime-related losses.

Regional Leaders: North America projected at USD 420 Million by 2033 with high SaaS density; Europe at USD 265 Million with GDPR-driven compliance adoption; Asia-Pacific at USD 180 Million supported by 52% growth in IT outsourcing.

Consumer/End-User Trends: IT service providers account for nearly 40% of policy purchases, followed by fintech firms (22%) and cloud infrastructure providers (18%).

Pilot or Case Example: In 2024, a U.S.-based insurtech pilot reduced underwriting turnaround by 35% using predictive analytics tools.

Competitive Landscape: Market leader holds approximately 18% share, followed by major insurers including multinational commercial liability providers and specialty underwriters.

Regulatory & ESG Impact: 54% of enterprise contracts now mandate professional liability coverage; ESG-linked governance standards are influencing policy structuring.

Investment & Funding Patterns: Over USD 4.5 Billion invested in global insurtech innovation over the past two years, with strong venture funding in AI-driven underwriting platforms.

Innovation & Future Outlook: Embedded insurance models and API-driven policy integration are expected to expand digital distribution channels by 40% by 2030.

Technology Errors and Omissions (E&O) Insurance Market demand is concentrated across IT services (40%), fintech (22%), healthcare technology (14%), and cloud infrastructure providers (18%). AI-based underwriting, automated claims analytics, and cyber-risk integration are reshaping policy design. Regulatory mandates, vendor liability clauses, and digital transformation initiatives accelerate adoption in North America and Europe, while Asia-Pacific benefits from rapid IT outsourcing growth. The market outlook remains strong, driven by contractual risk transfer and enterprise governance standards.

The Technology Errors and Omissions (E&O) Insurance Market holds strategic relevance as digital infrastructure becomes foundational to enterprise operations. With over 65% of global enterprises operating cloud-based workloads and 58% outsourcing critical IT functions, contractual liability transfer mechanisms have become mandatory across technology supply chains. Standalone E&O policies are increasingly embedded within broader cyber liability frameworks, enabling insurers to address both data breach and service failure exposures in integrated coverage models.

Artificial Intelligence–based underwriting platforms now deliver 28% improvement in risk-pricing accuracy compared to traditional actuarial assessment methods. Predictive claims analytics reduces manual processing by nearly 35% compared to legacy underwriting systems. North America dominates in policy volume, while Asia-Pacific leads in adoption momentum with over 52% of newly established IT firms opting for professional liability coverage within their first two operational years.

By 2028, AI-driven claims automation is expected to cut settlement cycle time by 30%, improving client retention and operational efficiency. Firms are committing to ESG-aligned governance frameworks, targeting 20% improvement in risk transparency metrics by 2027 through enhanced compliance reporting and digital audit trails.

In 2024, a U.S.-based commercial insurer achieved a 32% reduction in underwriting errors through machine-learning risk models integrated into SaaS onboarding workflows. Looking ahead, the Technology Errors and Omissions (E&O) Insurance Market is positioned as a pillar of enterprise resilience, regulatory compliance, and sustainable digital growth, reinforcing accountability across global technology ecosystems.

The Technology Errors and Omissions (E&O) Insurance Market is shaped by accelerating digital transformation, expanding third-party vendor ecosystems, and rising contractual liability standards across industries. With more than 70% of mid-to-large enterprises relying on external IT vendors, service-level agreement (SLA) enforcement has intensified, increasing professional liability exposure. Regulatory frameworks such as data protection mandates and financial compliance standards are integrating stricter indemnity requirements into vendor contracts. Claims frequency related to software malfunction, system downtime, and data transmission errors has increased by over 40% in recent years. Simultaneously, insurers are adopting AI-powered underwriting and advanced analytics to refine risk segmentation, improve policy customization, and enhance fraud detection. Competitive pricing pressures and increasing reinsurance costs also influence underwriting strategies, while embedded insurance distribution through digital platforms is expanding accessibility among startups and SMEs.

Global SaaS penetration has exceeded 60% among enterprises, with over 75% of workloads expected to run on cloud infrastructure environments. As service outages and coding errors directly impact business continuity, contractual indemnification clauses increasingly require minimum E&O coverage limits of USD 5–25 million. Nearly 68% of managed service providers report higher client-imposed liability standards compared to five years ago. The proliferation of API integrations, fintech platforms, and remote digital services has expanded exposure to professional negligence claims. Additionally, regulatory audits have increased by 30% across financial and healthcare IT sectors, further strengthening policy adoption among technology vendors and solution integrators.

Premium volatility remains a concern, particularly following a 35% increase in technology-related liability claims in recent underwriting cycles. Insurers face challenges in quantifying intangible software risks and emerging AI liabilities, leading to stricter policy exclusions and higher deductibles. Approximately 42% of SMEs report cost sensitivity as a barrier to standalone E&O adoption. Limited actuarial datasets for emerging technologies such as generative AI and decentralized finance platforms complicate accurate risk modeling. Reinsurance capacity constraints and evolving litigation standards further increase underwriting caution, slowing policy expansion among early-stage technology firms.

AI-enabled underwriting platforms can improve risk assessment efficiency by 28% and reduce onboarding time by nearly 40%. Embedded insurance models integrated into SaaS subscription workflows are expanding distribution reach, particularly among startups, where adoption rates exceed 50% during early funding rounds. Parametric triggers tied to system downtime metrics provide innovative claim settlement mechanisms, improving payout speed by 25%. Emerging markets in Asia-Pacific, with over 52% growth in IT outsourcing contracts, offer substantial untapped demand. Additionally, ESG-linked reporting requirements create opportunities for insurers to design governance-focused E&O packages tailored to regulated sectors.

Rapid regulatory evolution surrounding AI accountability, cross-border data flows, and digital financial services introduces legal ambiguity. Over 50% of multinational technology firms operate across jurisdictions with differing liability standards, complicating policy structuring. Emerging AI-related litigation cases have increased by 22%, prompting insurers to reassess coverage definitions. Compliance monitoring costs have risen by 18% as firms integrate data governance controls. Additionally, contractual disputes linked to system downtime and algorithmic bias create complex claim scenarios requiring specialized underwriting expertise and legal interpretation, increasing operational burdens for insurers.

AI-Powered Underwriting Enhancing Risk Precision by 28%: Insurers deploying machine-learning risk engines report 28% higher pricing accuracy and 35% reduction in manual underwriting interventions. Automated document analysis tools now process over 70% of policy applications digitally, improving turnaround time and reducing human error.

Embedded Insurance Adoption Rising Above 50% in SaaS Platforms: More than 50% of venture-backed SaaS firms integrate E&O coverage during onboarding workflows. API-driven distribution has increased policy issuance efficiency by 40%, particularly among SMEs seeking streamlined risk transfer solutions.

Expansion of Cyber-Integrated E&O Policies with 45% Uptake Growth: Approximately 45% of new policies now combine cyber liability and professional indemnity protections. Integrated coverage structures reduce coverage gaps and improve claims coordination efficiency by nearly 30%.

Regional Diversification with 52% Growth in Asia-Pacific IT Vendors: Asia-Pacific technology exporters report 52% growth in cross-border contracts requiring liability coverage. European enterprises show 48% compliance-driven policy adoption due to stringent data governance regulations, reinforcing structured indemnity frameworks.

The Technology Errors and Omissions (E&O) Insurance Market is segmented by type, application, and end-user, reflecting diverse risk exposures across the digital ecosystem. Coverage types vary from standalone E&O policies to integrated cyber-E&O packages and contractual liability endorsements, enabling tailored protection against software malfunction, data transmission errors, and service downtime. Application segmentation highlights strong demand from IT services, cloud computing, fintech platforms, and healthcare technology providers, where contractual indemnification clauses are increasingly mandatory. End-user insights indicate that managed service providers, SaaS vendors, fintech firms, and enterprise software developers represent the core policyholders. Over 65% of mid-to-large enterprises now require minimum professional liability coverage from third-party vendors, reinforcing segmentation growth. Additionally, startups and SMEs account for nearly 35% of new policy purchases, reflecting expanding awareness of technology liability risks. The segmentation landscape demonstrates risk-specific underwriting approaches, customized coverage limits, and evolving product bundling strategies designed to address emerging AI and cloud-related exposures.

The Technology Errors and Omissions (E&O) Insurance Market by type includes Standalone Technology E&O Policies, Cyber-Integrated E&O Policies, and Contractual Liability Endorsements. Standalone Technology E&O policies currently account for approximately 46% of adoption, as they provide focused coverage against coding errors, software negligence, and service-level failures. Cyber-integrated E&O policies hold around 34%, combining data breach liability and professional indemnity into unified frameworks. However, adoption of Cyber-Integrated E&O coverage is rising fastest, projected to expand at a CAGR of 8.1% through 2033, driven by the 45% increase in hybrid claims involving both cyber incidents and professional service disruptions. Contractual liability endorsements and customized policy riders collectively contribute nearly 20% of the market, serving niche requirements for enterprise IT outsourcing contracts and cross-border service agreements. These policies often align with indemnification clauses requiring coverage limits between USD 5–25 million.

Application-wise, the market spans IT & Managed Services, Cloud & SaaS Providers, Fintech Platforms, Healthcare IT, and E-commerce Technology Vendors. IT & Managed Services currently account for approximately 40% of adoption due to contractual obligations in outsourcing agreements. Cloud & SaaS providers hold about 27%, reflecting the surge in subscription-based enterprise platforms. However, fintech applications are expanding fastest, projected to grow at a CAGR of 9.4%, supported by rising digital payment penetration exceeding 65% in developed markets and growing regulatory oversight in financial technology ecosystems. Healthcare IT and e-commerce technology vendors collectively represent nearly 33% of total adoption, driven by electronic health record integration and online transaction ecosystems. In 2025, more than 38% of enterprises globally reported strengthening professional liability coverage for customer experience platforms. Additionally, 42% of U.S.-based digital health providers are expanding indemnity coverage to align with data interoperability standards.

End-user segmentation identifies Managed Service Providers (MSPs), SaaS Companies, Fintech Firms, Large Enterprises, and Small & Medium Enterprises (SMEs). Managed Service Providers represent the leading segment with nearly 36% share, as they manage third-party IT infrastructure and assume operational risk exposure across multiple clients. SaaS companies account for around 24%, while fintech firms hold 18%. However, SMEs represent the fastest-growing end-user category, projected to expand at a CAGR of 10.2%, driven by rising awareness and investor-mandated risk governance frameworks. Large enterprises and specialized software developers collectively contribute approximately 22% of adoption, reflecting structured compliance programs and enterprise-wide risk management strategies. In 2025, over 52% of venture-backed technology startups reported securing E&O coverage during early funding rounds. Additionally, 60% of enterprise procurement departments now include mandatory professional liability verification during vendor onboarding processes.

North America accounted for the largest market share at 41% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 9.1% between 2026 and 2033.

Europe held approximately 28% of the global Technology Errors and Omissions (E&O) Insurance Market in 2025, followed by Asia-Pacific at 19%, South America at 7%, and Middle East & Africa at 5%. Over 68% of enterprise IT outsourcing contracts in North America include mandatory professional liability clauses, compared to 54% in Europe and 47% in Asia-Pacific. Digital services exports from Asia-Pacific increased by 22% year-over-year, intensifying cross-border liability exposure. Meanwhile, more than 60% of regulated industries in Europe require formal vendor indemnity documentation, reinforcing structured E&O adoption. The regional distribution reflects maturity in underwriting frameworks in developed markets and accelerating demand from emerging digital economies.

North America represents 41% of the global Technology Errors and Omissions (E&O) Insurance Market share, supported by high enterprise digitalization and structured vendor risk governance. Key industries driving demand include fintech, healthcare IT, cloud computing, and managed services, where over 72% of vendor contracts require minimum E&O coverage thresholds. Regulatory developments such as strengthened data protection enforcement and financial compliance standards have increased professional liability scrutiny across digital service providers. Digital transformation remains advanced, with more than 75% of enterprises operating hybrid cloud infrastructure. AI-driven underwriting platforms are widely implemented, reducing policy issuance time by nearly 30%. A prominent U.S.-based insurer has deployed predictive analytics tools that improved underwriting accuracy by 28%, supporting scalable risk modeling. Consumer behavior in this region shows higher enterprise adoption in healthcare and financial services, where nearly 65% of institutions mandate formal liability verification before vendor onboarding.

Europe accounts for approximately 28% of the Technology Errors and Omissions (E&O) Insurance Market, led by Germany, the United Kingdom, and France, which collectively represent over 60% of regional demand. Strong regulatory frameworks, including data governance mandates and cross-border compliance rules, require enhanced vendor indemnity standards across financial services and healthcare technology. Nearly 58% of enterprises in regulated sectors conduct formal third-party risk audits annually. Adoption of AI-driven compliance monitoring tools has increased by 35% across enterprise IT environments. Regional insurers are introducing modular cyber-E&O packages to address hybrid risk exposures. A leading European specialty insurer recently expanded digital underwriting platforms across 15+ countries, streamlining cross-border policy issuance. Consumer behavior reflects regulatory pressure, with approximately 62% of enterprises prioritizing explainable risk documentation within procurement processes.

Asia-Pacific holds around 19% of the global market and ranks as the fastest-growing region by policy adoption. China, India, and Japan collectively contribute nearly 70% of regional demand. Cross-border IT outsourcing contracts increased by 24%, elevating professional liability exposure among service exporters. Rapid expansion of fintech ecosystems, with digital payment penetration exceeding 65% in key markets, further accelerates policy uptake. Infrastructure investments in cloud data centers rose by 18%, supporting SaaS and managed service providers. Regional insurtech firms are deploying automated underwriting platforms, improving application processing efficiency by 32%. In this region, growth is strongly driven by e-commerce and mobile AI applications, with over 55% of digital startups securing liability coverage during early-stage funding rounds.

South America represents approximately 7% of the Technology Errors and Omissions (E&O) Insurance Market, with Brazil and Argentina accounting for nearly 65% of regional demand. Growth is closely tied to expanding digital media platforms, fintech adoption, and cross-border IT services. Over 48% of mid-sized enterprises in Brazil report increasing reliance on outsourced software vendors. Government-led digital transformation programs and trade agreements have strengthened data governance requirements, influencing contractual indemnity standards. A regional commercial insurer recently introduced SME-focused technology liability packages, improving policy accessibility for businesses with under 250 employees. Consumer behavior variations show demand closely linked to media localization services and language-based digital platforms, particularly in Portuguese and Spanish markets.

Middle East & Africa accounts for roughly 5% of the global Technology Errors and Omissions (E&O) Insurance Market. Major growth countries include the United Arab Emirates and South Africa, contributing over 60% of regional adoption. Demand is influenced by oil & gas digitalization projects, smart infrastructure initiatives, and fintech modernization programs. Technology-enabled government services have expanded by 40% across selected Gulf economies, increasing vendor liability requirements. Local insurers are collaborating with international reinsurers to enhance underwriting capacity for high-limit technology contracts. Consumer behavior trends indicate growing enterprise awareness, with approximately 45% of technology startups in the UAE securing professional liability coverage within their first two years of operation.

United States – 36% Market Share: It is driven by high SaaS density, advanced enterprise IT outsourcing, and stringent vendor liability standards across regulated industries.

Germany – 11% Market Share: It is supported by strong industrial digitalization, strict compliance mandates, and structured third-party risk governance frameworks.

The Technology Errors and Omissions (E&O) Insurance Market is moderately fragmented, with more than 120 active global and regional insurers offering professional liability coverage tailored to technology-driven enterprises. The top five companies collectively account for approximately 48% of the global market share, indicating a semi-consolidated competitive structure led by multinational commercial insurers and specialty underwriters. Competition is primarily based on underwriting expertise, global policy servicing capabilities, digital claims processing efficiency, and integrated cyber-E&O offerings.

Strategic initiatives such as partnerships with insurtech platforms, AI-driven underwriting deployment, and embedded insurance distribution models are reshaping competitive positioning. Over 35% of leading insurers have integrated predictive analytics engines to enhance pricing accuracy and reduce underwriting turnaround time by nearly 30%. In addition, more than 25 merger and acquisition activities were recorded across professional liability and cyber insurance segments during 2024–2025, reflecting consolidation aimed at strengthening reinsurance capacity and expanding geographic reach.

Product innovation remains central to competition, with approximately 45% of new policy filings incorporating hybrid cyber-professional liability structures. Leading players are also investing in automated claims systems that improve settlement efficiency by up to 32%. The competitive landscape increasingly favors insurers with cross-border servicing capabilities, high-limit underwriting expertise exceeding USD 25 million per policy, and scalable digital distribution frameworks targeting SMEs and venture-backed technology firms.

Allianz SE

Zurich Insurance Group

Tokio Marine HCC

The Hartford

CNA Financial Corporation

Travelers Companies, Inc.

Beazley plc

Hiscox Ltd

Markel Corporation

Liberty Mutual Insurance

Sompo International

Technology advancements are fundamentally reshaping underwriting, claims processing, and risk modeling within the Technology Errors and Omissions (E&O) Insurance Market. Artificial intelligence–powered underwriting engines now analyze over 70% of policy applications through automated data extraction and risk scoring algorithms, improving pricing precision by nearly 28% compared to traditional actuarial methods. Predictive analytics platforms leverage historical claims datasets exceeding 10 years to identify high-risk sectors such as fintech and cloud infrastructure, where claim frequency has increased by 40%.

Blockchain-based policy documentation is gaining traction, with nearly 18% of large insurers piloting distributed ledger systems to enhance contract transparency and reduce documentation disputes. API-driven insurance integration enables real-time policy issuance within SaaS onboarding workflows, cutting issuance time by 35%.

Advanced claims analytics tools using natural language processing can assess litigation exposure within minutes, reducing manual review workloads by 30%. Additionally, cyber risk monitoring platforms integrated with E&O policies provide continuous risk scoring, alerting insured enterprises to operational vulnerabilities.

Emerging parametric triggers tied to measurable service downtime metrics allow automated claim settlements when uptime falls below predefined thresholds, reducing settlement delays by approximately 25%. Cloud-based underwriting ecosystems also support cross-border policy management across more than 50 jurisdictions, strengthening scalability. These technological integrations are positioning insurers to manage increasingly complex AI-related liabilities and globalized technology service risks with higher precision and operational efficiency.

• In October 2025, Resilience expanded its Technology Errors & Omissions (Tech E&O) insurance offering to include clients with more than $25 million in annual revenue in the United States, GBP 50 million in the UK, and EUR 25 million in the EU, increasing available limits up to $10 million and streamlining integrated cyber + tech E&O protection for technology companies’ operational risk exposures. Source: www.cyberresilience.com

• In November 2025, Chubb launched an AI-powered embedded insurance optimization engine within its Chubb Studio technology platform, using proprietary AI to analyze customer data and deliver personalized insurance offerings through digital channels, improving partner engagement and tailored insurance distribution. Source: www.news.chubb.com

• In April 2025, Resilience announced the launch of Tech E&O coverage for UK and EU enterprises with revenue thresholds above £50 million / €25 million, addressing growing technology liability risk across hardware, software, and services with limits up to £10 million / €10 million and integrating liability protection with cyber risk solutions. Source: www.cyberresilience.com

• In early 2025, Chubb also introduced a new Premier Life Science insurance package in APAC, which includes expanded professional indemnity and cyber insurance components tailored to technology-enabled healthcare and life sciences companies, reflecting insurers’ evolving risk coverage for technology products and services in specialized sectors. Source: www.chubb.mediaroom.com

The Technology Errors and Omissions (E&O) Insurance Market Report provides comprehensive coverage of product types, applications, end-user industries, regional markets, and evolving risk categories. The report evaluates standalone E&O policies, cyber-integrated liability structures, and contractual endorsements, analyzing their adoption across IT services, fintech, SaaS, healthcare technology, and e-commerce ecosystems. It assesses policy limit structures commonly ranging from USD 1 million to over USD 25 million, reflecting varying enterprise risk exposure levels.

Geographically, the scope spans North America, Europe, Asia-Pacific, South America, and Middle East & Africa, examining regulatory environments across more than 50 jurisdictions. The report incorporates analysis of enterprise vendor risk governance trends, where over 60% of regulated industries mandate formal indemnity clauses. It further evaluates SME participation, which accounts for nearly 35% of new policy purchases, and venture-backed technology startups integrating liability coverage during early funding stages.

Technological scope includes AI-driven underwriting systems, blockchain-based policy management, predictive claims analytics, and parametric downtime triggers. The report also explores cross-border IT outsourcing growth exceeding 20% annually in selected emerging markets and digital transformation initiatives influencing contractual liability requirements. Overall, the report delivers strategic insights into risk mitigation frameworks, innovation trends, competitive positioning, and sector-specific liability exposure shaping the Technology Errors and Omissions (E&O) Insurance Market globally.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 574.0 Million |

| Market Revenue (2033) | USD 928.8 Million |

| CAGR (2026–2033) | 6.2% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Chubb Limited; AIG (American International Group); AXA XL; Allianz SE; Zurich Insurance Group; Tokio Marine HCC; The Hartford; CNA Financial Corporation; Travelers Companies, Inc.; Beazley plc; Hiscox Ltd; Markel Corporation; Liberty Mutual Insurance; Sompo International |

| Customization & Pricing | Available on Request (10% Customization Free) |