Reports

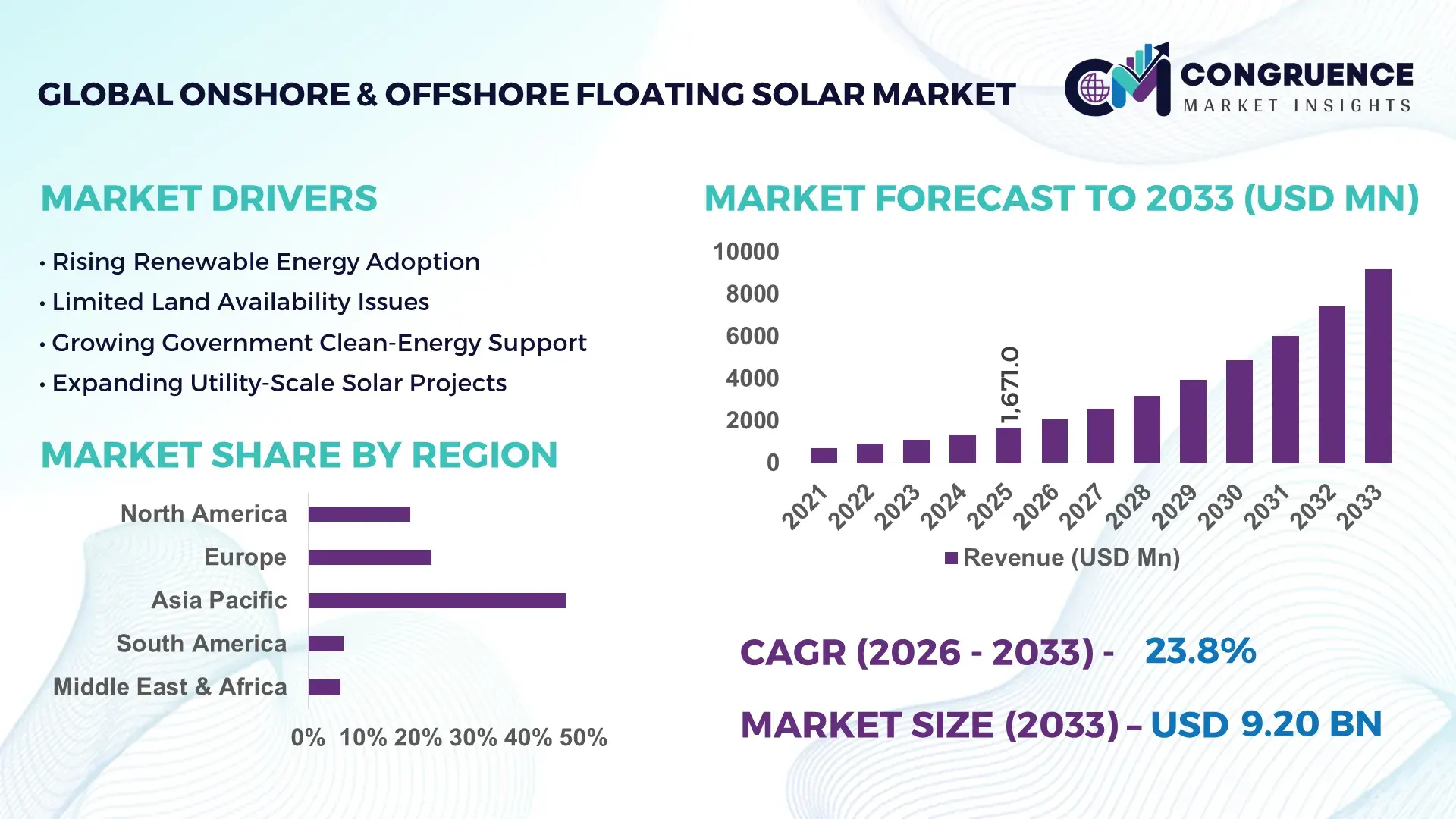

The Global Onshore & Offshore Floating Solar Market was valued at USD 1,671.0 Million in 2025 and is anticipated to reach a value of USD 9,196.4 Million by 2033 expanding at a CAGR of 23.76% between 2026 and 2033. Growth is being propelled by large-scale reservoir solar deployments, grid-constrained land optimization strategies, and government-backed renewable infrastructure programs across Asia and Europe.

China remains the dominant market, accounting for more than 38% of global floating solar installed capacity, supported by multi-gigawatt projects on former coal mining lakes and industrial reservoirs. The country added over 216 GW of solar capacity in 2025, significantly outpacing Japan, which leads floating solar density with over 5,000 operational water-based installations. India is accelerating deployment through reservoir-based projects exceeding 600 MW, highlighting a widening capacity gap and technology adoption advantage among leading Asian economies.

Strategically, companies securing access to water-based infrastructure and utility partnerships are strengthening long-term competitive positioning in the high-efficiency renewable energy ecosystem.

Market Size & Growth: Valued at USD 1,671.0 Million in 2025 and projected to reach USD 9,196.4 Million by 2033, supported by a 23.76% growth trajectory driven by reservoir-based renewable infrastructure expansion and land-use optimization.

Top Growth Drivers: Utility-scale renewable deployment (+42%), reservoir utilization projects (+35%), and grid modernization investments (+28%) are accelerating market penetration.

Short-Term Forecast: By 2028, floating solar installation costs are expected to decline by nearly 18% while energy yield improves by approximately 10% through advanced cooling effects.

Emerging Technologies: AI-powered performance monitoring, digital twin asset management, and corrosion-resistant floating platforms are improving operational efficiency by over 15%.

Regional Leaders: Asia Pacific exceeds USD 4.5 Billion potential, Europe surpasses USD 1.8 Billion, and North America approaches USD 1.2 Billion, driven by utility-scale reservoir projects and energy diversification.

Consumer/End-User Trends: More than 40% of new utility renewable projects are evaluating hybrid water-based solar integration to maximize infrastructure utilization.

Pilot/Case Example: A 2025 reservoir floating solar deployment demonstrated over 12% higher electricity generation compared with adjacent land-based systems due to lower module temperatures.

Competitive Landscape: China-based developers collectively control nearly 30% of global installed capacity, with key participants including Sungrow, Ciel & Terre, Trina Solar, JA Solar, and LONGi.

Regulatory & ESG Impact: Water-surface solar installations can reduce reservoir evaporation by up to 30%, supporting national water-security and decarbonization objectives.

Investment & Funding: More than USD 3 Billion in recent project commitments reflects strong utility partnerships, infrastructure financing, and regional expansion strategies.

Innovation & Future Outlook: Offshore floating solar, hybrid solar-storage systems, and integrated hydrogen production platforms are redefining next-generation renewable energy deployment.

The Onshore & Offshore Floating Solar Market is increasingly shaped by demand from utilities, water authorities, mining operators, and industrial energy users seeking higher land-use efficiency. Advanced anchoring systems, bifacial photovoltaic modules, and AI-enabled asset monitoring are enhancing operational performance, while floating installations generate up to 10–15% higher output through natural cooling effects. Regulatory support for reservoir utilization and localized supply-chain development is accelerating project pipelines, setting the stage for deeper strategic market evaluation.

The Onshore & Offshore Floating Solar Market has emerged as a strategic investment priority because it addresses two critical infrastructure challenges simultaneously: renewable energy expansion and land scarcity. Utilities, industrial operators, and governments are increasingly utilizing reservoirs, mining lakes, and coastal zones to deploy solar assets without competing for agricultural or urban land. Regulatory reforms supporting water-based renewable installations and grid modernization initiatives are accelerating project approvals across key markets.

Technology improvements are strengthening commercial viability. Floating solar systems typically operate at module temperatures 5–10°C lower than comparable land-based installations, enabling energy output gains of up to 15% while reducing land acquisition costs. China and India continue to scale large reservoir projects exceeding hundreds of megawatts, while Japan focuses on high-density deployment across limited water resources. Europe is advancing offshore pilot projects that integrate renewable generation with coastal energy infrastructure and storage systems.

Over the next two to three years, hybrid floating solar-storage projects are expected to become a primary deployment model. Developers are expanding partnerships with utilities, water authorities, and infrastructure investors to secure long-term project pipelines. Organizations that establish strong engineering capabilities, localized supply networks, and advanced asset management platforms will achieve superior operational efficiency and strengthen competitive positioning in the evolving renewable energy landscape.

The strongest growth catalyst is the rapid utilization of reservoirs, hydropower assets, and industrial water bodies for renewable generation. Floating solar installations can improve power output by 10–15% due to lower operating temperatures while reducing water evaporation by as much as 30%. China continues deploying large-scale projects on former mining lakes, while India has prioritized floating solar across major reservoirs under renewable capacity expansion programs. This infrastructure-focused approach eliminates land acquisition constraints that account for nearly 20–25% of conventional project development costs. As a result, utilities and independent power producers are increasing investments in floating platforms, advanced anchoring technologies, and hybrid solar-storage systems. Companies that secure reservoir access rights and utility partnerships are creating durable competitive advantages while accelerating project deployment timelines.

Despite strong adoption momentum, floating solar projects face higher engineering requirements than conventional ground-mounted systems. Floating structures, mooring systems, and corrosion-resistant components can increase upfront installation costs by 15–25%. Offshore deployments face additional challenges from wave action, salinity exposure, and specialized maintenance requirements. Several developers remain dependent on imported floating platform materials and marine-grade components, creating procurement risks during supply-chain disruptions. In countries with fragmented water-use regulations, permitting timelines can extend beyond 12–18 months, delaying project execution. To mitigate these constraints, companies are localizing component manufacturing, negotiating long-term supplier agreements, and investing in standardized floating platform architectures that improve scalability and reduce lifecycle costs.

Significant opportunity exists in combining floating solar with battery storage, hydropower infrastructure, and green hydrogen production. Hybrid renewable facilities can improve grid utilization rates by more than 20% while increasing overall asset productivity. Japan and South Korea are actively evaluating offshore floating solar concepts that leverage existing coastal infrastructure and transmission networks. AI-driven predictive maintenance platforms are reducing operational downtime by approximately 15%, creating new value beyond electricity generation. Developers are also exploring bifacial photovoltaic modules capable of capturing reflected light from water surfaces, improving energy yields by 5–10%. Forward-looking companies are strengthening R&D programs, forming technology partnerships, and expanding into underpenetrated water-rich markets where infrastructure utilization remains relatively low.

The primary long-term challenge is ensuring operational consistency as projects move from sheltered reservoirs to more demanding offshore environments. Offshore floating structures must withstand higher wind loads, wave dynamics, and corrosive marine conditions that can shorten equipment lifecycles by 20–30% without proper engineering controls. Integration with transmission infrastructure also remains complex, particularly in emerging markets where grid modernization is still underway. Workforce shortages in marine engineering and specialized renewable construction are increasing project execution pressures. Companies must invest in advanced materials, digital monitoring systems, and predictive asset management platforms to maintain reliability. Organizations that successfully solve offshore durability and grid integration challenges will establish a substantial strategic advantage as large-scale coastal deployments become commercially viable.

Utility-Scale Reservoir Integration Large energy developers are increasingly integrating floating solar with existing reservoir and hydropower infrastructure, reducing transmission development requirements by nearly 25% and improving grid utilization rates by over 18%. China and India continue prioritizing reservoir-based deployments exceeding 100 MW capacity, while utilities are accelerating hybrid project pipelines. This shift shortens project timelines, lowers land acquisition costs, and enables faster renewable integration through shared infrastructure and operational synergies.

Advanced Floating Platform Engineering Demand for high-durability floating structures has increased significantly as developers target larger and deeper water bodies. New-generation modular platforms have reduced installation time by approximately 20% while lowering maintenance requirements by nearly 15%. Marine-grade polymers, corrosion-resistant anchoring systems, and digital structural monitoring are becoming standard specifications. Companies are expanding manufacturing partnerships and localized production networks to improve supply-chain resilience and support large-scale deployment requirements.

AI-Driven Asset Optimization Digital asset management adoption has accelerated, with AI-enabled monitoring platforms improving fault detection accuracy by nearly 30% and reducing unplanned downtime by more than 12%. Operators are integrating drone inspections, predictive maintenance software, and real-time performance analytics into floating solar operations. Rising labor costs and increasing asset complexity are driving this transition, allowing developers to improve energy yields while optimizing maintenance schedules and operational efficiency.

Hybrid Renewable Energy Deployment Floating solar projects are increasingly paired with battery storage and hydropower assets, improving renewable dispatchability and enhancing infrastructure utilization by up to 22%. More than 35% of newly announced large-scale projects incorporate hybrid configurations designed to stabilize grid performance. Developers are forming strategic partnerships with storage providers and grid operators, creating integrated energy platforms that deliver greater operational flexibility while strengthening long-term project economics.

Onshore Floating Solar remains the leading segment, accounting for approximately 72% of total installed capacity due to easier deployment, lower engineering complexity, and widespread availability of reservoirs, mining lakes, irrigation ponds, and water treatment facilities. Utility operators continue prioritizing onshore installations because project development timelines are typically 20–30% shorter than offshore alternatives. Large-scale reservoir projects in China, India, and Southeast Asia have strengthened this segment’s dominance by enabling rapid capacity additions without competing for agricultural or industrial land. Developers are expanding floating platform manufacturing and standardizing deployment processes to further improve scalability. Offshore Floating Solar represents the fastest-growing segment as technological advancements improve platform stability, mooring systems, and marine durability. Offshore projects can access significantly larger deployment areas and complement coastal energy infrastructure. Although offshore installations currently represent less than 30% of market capacity, pilot deployments have demonstrated energy yield improvements of up to 10–15% through enhanced cooling effects. Companies are increasing investments in marine engineering partnerships, advanced materials, and hybrid offshore energy platforms to establish early leadership positions. The market is increasingly balancing mature reservoir deployments with emerging offshore opportunities, driving diversified investment strategies.

Reservoir applications represent the largest segment, accounting for nearly 60% of floating solar deployment activity. Utilities and government agencies increasingly utilize reservoirs because existing grid connections and water infrastructure reduce project complexity while improving development economics. Reservoir-based projects also provide operational benefits through evaporation reduction of up to 30% and improved land-use efficiency. Large-scale installations exceeding 100 MW are becoming more common as operators seek to maximize renewable generation without expanding land footprints. Companies continue scaling reservoir-focused project portfolios through utility partnerships and long-term infrastructure agreements. Mining lakes are emerging as the fastest-growing application due to the growing repurposing of abandoned industrial sites for renewable energy generation. Deployment activity across former mining regions has increased by more than 25%, driven by sustainability mandates and brownfield redevelopment initiatives. Irrigation ponds and water treatment facilities remain strategically important for distributed generation and municipal energy optimization, while offshore water applications are attracting growing investment for long-term capacity expansion. Developers are tailoring platform designs to application-specific requirements, strengthening operational performance across diverse water environments.

Utilities remain the dominant end-user segment, representing approximately 65% of installed floating solar capacity due to their control over large water assets, transmission infrastructure, and utility-scale procurement programs. Energy providers continue deploying floating solar to strengthen renewable portfolios while improving grid stability and infrastructure utilization. Utility-led projects typically exceed the scale of commercial installations by more than 40%, allowing operators to benefit from procurement efficiencies and optimized asset management. Companies are prioritizing strategic utility partnerships and long-term power supply agreements to secure market share. Industrial users are the fastest-growing end-user group as manufacturers, mining companies, and heavy industrial facilities pursue energy cost optimization and sustainability objectives. Industrial adoption has increased by nearly 20% annually through deployment on industrial reservoirs, wastewater facilities, and mining lakes. Government and municipal entities continue expanding investments in water infrastructure-based renewable projects, while commercial users increasingly adopt floating solar to offset rising electricity expenses. Suppliers are responding with customized financing models, modular platform designs, and integrated energy management solutions tailored to diverse operational requirements.

Asia-Pacific accounted for the largest market share at 46.8% in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 26.4% between 2026 and 2033.

North America represented approximately 18.5% of the global market in 2025, supported by increasing deployment across reservoirs, water treatment facilities, and utility-owned water infrastructure. The region is witnessing a shift toward floating solar integration with battery storage and hydropower assets to improve grid flexibility and infrastructure utilization. Several states are prioritizing water-surface solar projects as land-use constraints and transmission bottlenecks intensify. More than 35% of newly proposed floating solar projects in the region incorporate energy storage systems. Utilities are actively partnering with technology providers to deploy modular floating platforms and digital monitoring solutions, improving project efficiency while accelerating renewable capacity additions across strategic infrastructure assets.

United States Market Outlook: The United States remains the largest market in North America due to its extensive reservoir network, strong utility investment activity, and growing emphasis on grid modernization. More than 24,000 man-made reservoirs provide significant deployment potential, while utility-scale developers are expanding floating solar feasibility programs across California, Texas, and Florida. Increasing adoption of hybrid renewable systems and digital asset management platforms is strengthening operational performance. Public-private partnerships are also accelerating pilot deployments designed to optimize water infrastructure while supporting long-term renewable energy targets.

Europe accounted for nearly 22.4% of global market activity in 2025, driven by renewable energy mandates, water resource optimization initiatives, and advanced offshore engineering capabilities. The region is emerging as a leader in offshore floating solar innovation, with several pilot projects being integrated into existing coastal energy networks. Reservoir and quarry-based floating solar installations continue expanding, while utility operators increasingly prioritize multi-use energy infrastructure. More than 40% of newly announced projects involve advanced anchoring systems and digital performance monitoring. Energy developers are leveraging cross-border partnerships and infrastructure modernization programs to improve deployment efficiency and strengthen renewable generation capacity.

Netherlands Market Outlook: The Netherlands continues to play a strategic role through its expertise in water engineering, offshore infrastructure, and renewable energy integration. The country has developed several large-scale floating solar installations on lakes, sand extraction sites, and water storage facilities. Floating solar projects are increasingly combined with biodiversity enhancement and water management objectives. Dutch developers are also exporting engineering expertise and platform technologies to international markets, strengthening the country's influence across the global floating solar value chain while supporting continued innovation in offshore deployment models.

Asia-Pacific dominated the market with approximately 46.8% share in 2025, supported by extensive manufacturing capacity, large reservoir infrastructure, and aggressive renewable deployment programs. China, India, Japan, and South Korea continue driving large-scale project development through utility investments and energy security initiatives. The region accounts for more than 70% of global floating solar module and component production, creating substantial supply-chain advantages. Reservoir-based projects exceeding 100 MW are becoming increasingly common, while governments continue prioritizing water-surface renewable generation. Companies are expanding domestic manufacturing, improving project standardization, and accelerating deployment through integrated engineering and procurement capabilities.

China Market Outlook: China remains the global market leader, supported by extensive reservoir resources, strong photovoltaic manufacturing capabilities, and utility-scale deployment expertise. The country accounts for more than one-third of global floating solar capacity and continues expanding installations on former mining lakes, hydropower reservoirs, and industrial water bodies. Domestic manufacturers are investing heavily in advanced floating structures, bifacial module technologies, and AI-enabled asset management systems. Strong infrastructure planning and vertically integrated supply chains provide a significant operational advantage, enabling rapid project execution and cost-efficient scaling across multiple provinces.

South America accounted for approximately 6.4% of global market activity in 2025, with development concentrated around hydropower reservoirs and industrial water infrastructure. Countries across the region are exploring floating solar as a means of enhancing energy diversification while maximizing existing transmission assets. Integration with hydropower facilities has emerged as a key operational trend, improving energy balancing and reservoir utilization. Several projects have demonstrated the ability to increase infrastructure productivity without requiring additional land acquisition. However, financing availability and grid limitations continue influencing deployment speed. Developers are increasingly pursuing strategic partnerships and phased project execution models to improve investment viability.

Brazil Market Outlook: Brazil leads the South American market through its extensive hydropower network and large reservoir footprint. Floating solar deployment is increasingly focused on complementing hydroelectric generation and improving energy reliability during seasonal fluctuations. Utility operators are evaluating hybrid renewable configurations capable of leveraging existing transmission infrastructure while reducing operational costs. The country's strong renewable energy ecosystem, combined with increasing private-sector participation, continues to create favorable conditions for project expansion. Growing investment in distributed renewable infrastructure is further strengthening long-term deployment prospects.

Middle East & Africa represented nearly 5.9% of the market in 2025 but is rapidly gaining strategic importance through large-scale renewable investments and water infrastructure modernization initiatives. Countries across the region are utilizing reservoirs, desalination facilities, and industrial water assets to support floating solar deployment. Energy diversification programs and sustainability targets are encouraging utility-scale project development, particularly in water-stressed environments. More than 30% of recently announced renewable infrastructure initiatives include assessments for floating solar integration. Developers are prioritizing partnerships, localized engineering expertise, and advanced platform technologies capable of operating under challenging environmental conditions.

Saudi Arabia Market Outlook: Saudi Arabia is emerging as the region's most influential market due to its large renewable energy investment pipeline, ambitious energy diversification strategy, and expanding water infrastructure network. Floating solar is increasingly being evaluated for integration with reservoirs, water treatment facilities, and industrial complexes. Government-backed infrastructure modernization programs are accelerating feasibility assessments and pilot deployments. The country’s focus on large-scale renewable development, combined with growing interest in hybrid solar-storage systems, positions it as a key future deployment hub within the Middle East and Africa market landscape.

The competitive landscape is led by technology-focused floating platform specialists such as Ciel & Terre competing against vertically integrated solar manufacturers including Sungrow, LONGi, and Trina Solar, while EPC-focused firms such as Tata Power Renewable Energy and Sterling and Wilson Renewable Energy compete on project execution speed and infrastructure scale. The top five players collectively control approximately 42–48% of global floating solar deployment activity. Competition is increasingly centered on platform durability, engineering efficiency, supply-chain control, and utility-scale project delivery. Advanced anchoring and floating technologies can improve operational performance by 10–15%, while localized manufacturing reduces logistics costs by nearly 12%. Project execution timelines have become a critical differentiator, with leading developers reducing installation schedules by approximately 20% through modular deployment systems. Market leaders are expanding through strategic partnerships, reservoir access agreements, technology licensing, and vertical integration across design, manufacturing, EPC, and operations. The competitive shift is moving toward offshore-capable platforms and AI-enabled asset management. High engineering requirements, waterbody access rights, and utility relationships remain key entry barriers. Winning requires superior deployment expertise, resilient supply chains, and differentiated floating infrastructure technology.

Sungrow Power Supply Co., Ltd.

LONGi Green Energy Technology Co., Ltd.

Trina Solar Co., Ltd.

JA Solar Technology Co., Ltd.

Tata Power Renewable Energy Limited

Sterling and Wilson Renewable Energy Limited

Scatec ASA

Noria Energy

BayWa r.e.

Hanwha Qcells

First Solar, Inc.

Canadian Solar Inc.

Sharp Energy Solutions Corporation

Floating solar technology is evolving from basic pontoon-supported photovoltaic systems toward highly engineered energy infrastructure. Current deployments increasingly utilize bifacial solar modules, high-density polyethylene floating platforms, and intelligent anchoring systems. Bifacial modules improve energy generation by approximately 5–12% through reflected light capture from water surfaces, while advanced floating structures reduce maintenance requirements by nearly 15%. More than 60% of recently announced utility-scale projects incorporate digital monitoring and remote asset management capabilities to optimize operational performance.

Emerging technologies are centered on AI-enabled predictive maintenance, digital twin modeling, and corrosion-resistant offshore platform architectures. Compared with conventional floating systems, AI-driven monitoring solutions improve fault detection accuracy by approximately 30% and reduce unplanned downtime by over 12%. Offshore-capable floating platforms designed for wave and wind resilience are gaining traction, particularly among developers targeting coastal deployment opportunities. Technology providers and integrated EPC firms benefit most because advanced engineering capabilities increasingly influence project selection and long-term asset performance.

Between 2026 and 2028, hybrid floating solar-storage systems and offshore floating solar installations will reshape competitive positioning. Autonomous inspection drones, smart mooring systems, and floating inverter platforms are expected to become mainstream deployment standards. Companies investing early in marine engineering expertise, digital optimization tools, and integrated renewable infrastructure platforms will secure stronger operational efficiency, faster deployment execution, and greater access to utility-scale project opportunities.

May 2025 – Ciel & Terre completed a 120 MWp floating solar project at Omkareshwar, India, introducing rock-bolt anchoring technology and reinforced fiberglass inverter barges. The deployment strengthened large-scale reservoir solar engineering capabilities and improved project stability for utility-scale installations. Source: www.pv-magazine.com

February 2025 – Welspun New Energy signed an agreement to develop a 1 GW floating solar project alongside a 1.2 GW pumped storage facility in Odisha. The initiative accelerated hybrid renewable infrastructure development and strengthened long-term energy storage integration strategies.

March 2026 – Oriana Power secured an EPC order for a 234 MW floating solar project at the Maithon Dam Reservoir. The project expanded utility-scale floating solar deployment and reinforced demand for integrated engineering, procurement, construction, and long-term operations services.

August 2025 – Noria Energy began construction of a floating solar project utilizing its AquaPhi® tracking technology, designed to increase energy output compared with fixed floating systems. The innovation demonstrated the growing role of intelligent tracking solutions in improving water-based solar performance.

This report provides a comprehensive assessment of the global Onshore & Offshore Floating Solar Market across technology platforms, deployment environments, applications, and end-user industries. The analysis covers onshore and offshore floating solar systems, reservoir-based installations, mining lakes, irrigation infrastructure, and emerging coastal deployment models. More than 70% of current deployment activity remains concentrated within utility-scale projects, while industrial and municipal applications continue expanding through infrastructure modernization initiatives.

The report evaluates market performance across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting deployment trends, competitive positioning, technology adoption patterns, and strategic investment priorities. It examines floating platform innovations, bifacial photovoltaic modules, AI-enabled asset management, hybrid storage integration, and offshore engineering advancements. The study supports investment planning, market entry decisions, partnership strategies, capacity expansion programs, and competitive benchmarking while identifying high-potential growth areas and operational trends expected to influence industry direction between 2026 and 2033.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 1,671.0 Million |

| Market Revenue (2033) | USD 9,196.4 Million |

| CAGR (2026–2033) | 23.76% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Ciel & Terre International; Sungrow Power Supply Co., Ltd.; LONGi Green Energy Technology Co., Ltd.; Trina Solar Co., Ltd.; JA Solar Technology Co., Ltd.; Tata Power Renewable Energy Limited; Sterling and Wilson Renewable Energy Limited; Scatec ASA; Noria Energy; BayWa r.e.; Hanwha Qcells; First Solar, Inc.; Canadian Solar Inc.; Sharp Energy Solutions Corporation |

| Customization & Pricing | Available on Request (10% Customization Free) |