Reports

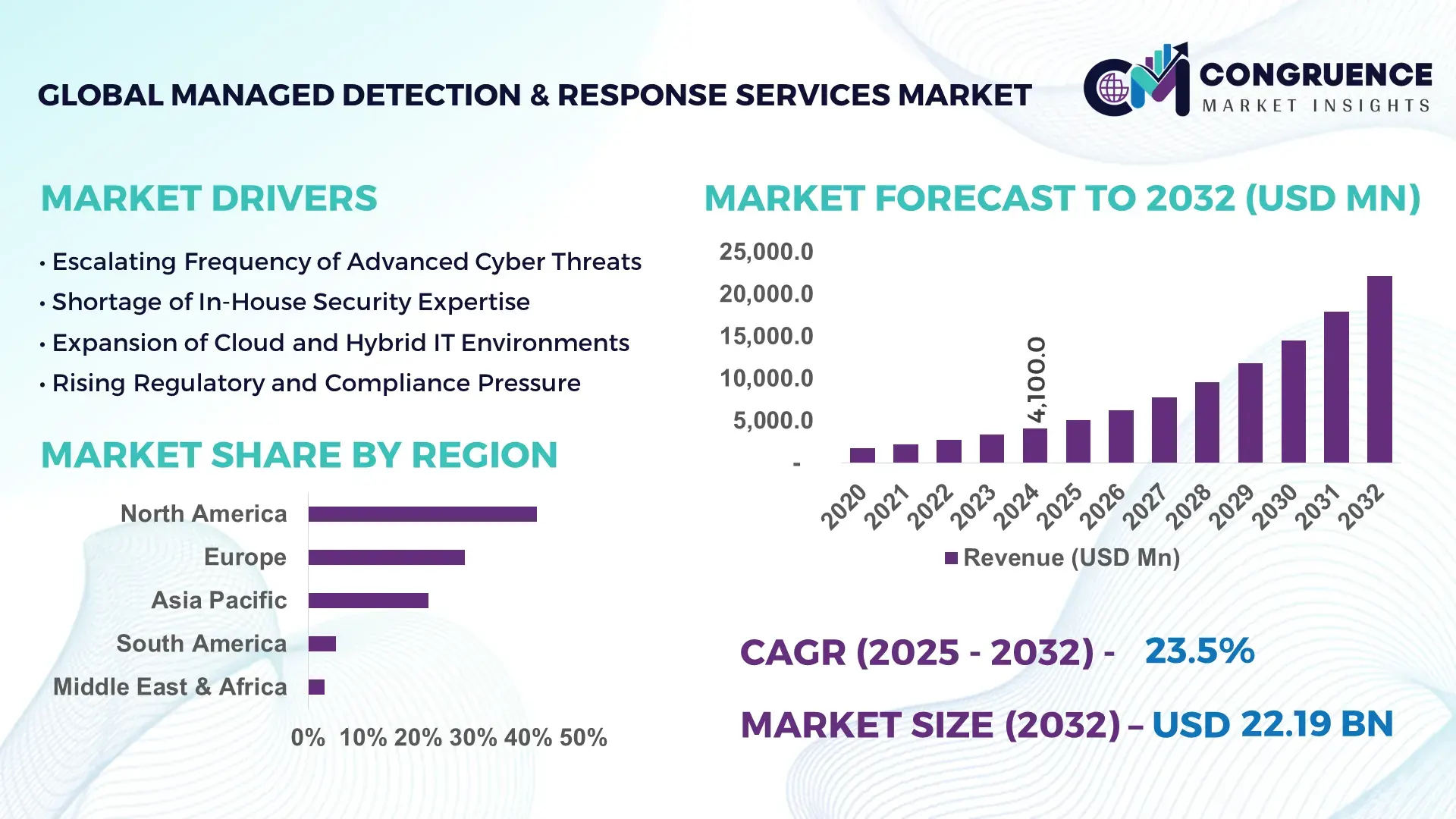

The Global Managed Detection & Response Services Market was valued at USD 4,100.0 Million in 2024 and is anticipated to reach a value of USD 22,188.1 Million by 2032 expanding at a CAGR of 23.5% between 2025 and 2032, according to an analysis by Congruence Market Insights. This growth is primarily driven by rising enterprise exposure to sophisticated cyber threats and the increasing need for continuous, intelligence-led security monitoring across hybrid IT environments.

The United States dominates the Managed Detection & Response Services Market in terms of deployment scale, technology depth, and enterprise adoption. Over 68% of Fortune 1000 organizations in the U.S. actively use MDR or co-managed SOC models to supplement internal security teams. Annual cybersecurity investments in the country exceeded USD 90 billion in 2024, with a growing share allocated to outsourced detection and response capabilities. The U.S. hosts more than 45% of global MDR service providers, supporting high-volume monitoring operations exceeding 30 trillion security events per year. Key industry applications span BFSI, healthcare, defense, cloud service providers, and critical infrastructure. Advanced AI-driven threat analytics, SOAR integration, and XDR-based telemetry correlation are widely deployed, with over 60% of U.S.-based MDR platforms now using machine learning–based behavioral analytics for threat prioritization.

Market Size & Growth: Valued at USD 4,100.0 million in 2024, projected to reach USD 22,188.1 million by 2032, growing at a CAGR of 23.5%, supported by rising cyberattack frequency and skills shortages in internal SOC teams.

Top Growth Drivers: Cloud workload protection adoption at 62%, ransomware incident growth at 41%, and SOC automation efficiency gains of 35%.

Short-Term Forecast: By 2028, MDR adoption is expected to reduce mean time to detect (MTTD) by 48% across large enterprises.

Emerging Technologies: AI-based behavioral analytics, extended detection and response (XDR), and automated SOAR orchestration platforms.

Regional Leaders: North America projected at USD 8.9 billion by 2032 with enterprise SOC outsourcing; Europe at USD 6.2 billion driven by regulatory compliance; Asia Pacific at USD 4.7 billion led by cloud-native MDR adoption.

Consumer/End-User Trends: BFSI and healthcare together account for over 44% of MDR deployments due to regulatory pressure and data sensitivity.

Pilot or Case Example: In 2023, a U.S. financial institution reduced incident response time by 52% through AI-enabled MDR integration.

Competitive Landscape: Arctic Wolf leads with ~18% share, followed by CrowdStrike, Secureworks, Rapid7, and Red Canary.

Regulatory & ESG Impact: Data protection mandates and cyber resilience regulations are accelerating MDR procurement in regulated sectors.

Investment & Funding Patterns: Over USD 3.4 billion invested globally in MDR-focused cybersecurity firms between 2022–2024.

Innovation & Future Outlook: Increased convergence of MDR with cloud security posture management and identity threat detection is reshaping service models.

Global adoption of Managed Detection & Response Services is concentrated across BFSI (24%), healthcare (20%), IT & telecom (18%), manufacturing (15%), and government (11%). Recent innovations include AI-powered threat scoring engines, cloud-native MDR platforms, and zero-trust-aligned response frameworks. Regulatory mandates, rising digitalization, and regional cloud adoption patterns are accelerating demand, while future outlook points toward unified MDR–XDR ecosystems and predictive threat containment models.

The Managed Detection & Response Services Market holds strong strategic relevance as organizations transition from reactive cybersecurity models to proactive, intelligence-driven defense architectures. MDR services enable enterprises to offset cybersecurity talent shortages while maintaining 24/7 monitoring, advanced threat hunting, and rapid incident response across complex hybrid infrastructures. AI-driven MDR platforms deliver up to 45% improvement in threat detection accuracy compared to traditional SIEM-based monitoring systems, enabling faster containment and reduced breach impact.

Comparatively, XDR-integrated MDR delivers a 38% improvement in cross-domain threat correlation compared to legacy endpoint-only detection standards. North America dominates in deployment volume, while Europe leads in regulated-sector adoption with over 57% of financial institutions using MDR services to meet compliance requirements. By 2027, AI-driven behavioral analytics is expected to cut false-positive security alerts by 50%, improving SOC productivity and reducing analyst fatigue.

From a compliance and ESG perspective, firms are committing to improved cyber resilience metrics, including a targeted 40% reduction in breach-related operational downtime by 2028. In 2024, a U.S.-based healthcare network achieved a 47% reduction in ransomware recovery time through MDR-led automation and threat intelligence sharing. Looking forward, the Managed Detection & Response Services Market is positioned as a foundational pillar supporting enterprise resilience, regulatory compliance, and sustainable digital growth amid escalating global cyber risks.

The Managed Detection & Response Services Market is shaped by escalating cyberattack sophistication, rapid cloud migration, and increasing regulatory scrutiny. Enterprises are shifting from tool-centric security approaches to outcome-driven MDR models that prioritize threat visibility and response speed. The integration of AI, automation, and threat intelligence is enhancing operational efficiency, while demand is rising across regulated industries and mid-sized enterprises. Vendor differentiation increasingly centers on response depth, automation maturity, and integration with enterprise security stacks.

Cyberattacks now involve multi-stage tactics, including lateral movement, credential abuse, and ransomware-as-a-service models. Over 72% of breaches involve advanced persistent threats that bypass traditional perimeter defenses. MDR services address this by delivering continuous monitoring across endpoints, networks, and cloud environments. Enterprises using MDR report up to 46% faster incident containment and a 39% reduction in breach impact severity, making MDR a critical growth driver for modern cybersecurity strategies.

Concerns over sensitive data handling and cross-border data flows limit MDR adoption in certain regions. Approximately 34% of enterprises cite regulatory uncertainty and integration challenges with legacy systems as barriers. Complex IT environments require extensive customization, increasing onboarding timelines and operational friction, particularly for highly regulated organizations.

Cloud workload growth has surpassed 60% across enterprises, creating demand for cloud-native MDR platforms. Organizations adopting cloud-optimized MDR experience a 42% improvement in visibility across SaaS, IaaS, and containerized environments. This creates significant opportunities for providers offering scalable, API-driven MDR solutions.

Despite MDR’s outsourcing benefits, provider-side talent shortages persist. Nearly 3.5 million cybersecurity positions remain unfilled globally. This constrains service scalability and increases analyst workload, challenging providers to invest heavily in automation and AI to maintain service quality and response consistency.

AI-Driven Threat Correlation and Automation: Over 64% of MDR platforms now deploy machine-learning-based analytics to correlate telemetry across endpoints, networks, and cloud assets. Automated response workflows have reduced manual intervention requirements by 41%, improving consistency and lowering response latency across large enterprise environments.

Expansion of XDR-Integrated MDR Models: XDR-enabled MDR deployments increased by 58% between 2022 and 2024, enabling unified visibility across security layers. Enterprises adopting XDR-based MDR report a 36% reduction in alert fatigue and a 44% improvement in threat prioritization accuracy.

Sector-Specific MDR Customization: Healthcare and BFSI-focused MDR offerings now account for 39% of new deployments. Customized compliance reporting and sector-aligned threat models have improved regulatory audit readiness by 33% and reduced investigation time by 29%.

Growth in Mid-Market and Co-Managed SOC Adoption: Mid-sized enterprises represent 46% of new MDR customers, driven by co-managed SOC models. These organizations report a 51% reduction in security operations costs while maintaining enterprise-grade detection and response capabilities.

The Global Managed Detection & Response Services Market is segmented based on type, application, and end-user groups, reflecting how organizations deploy MDR capabilities across diverse security environments. By type, segmentation highlights variations in service depth, ranging from endpoint-centric monitoring to fully integrated, cloud-native MDR platforms. Application-based segmentation illustrates how MDR is tailored to protect endpoints, networks, cloud workloads, and identities, aligning security operations with evolving attack surfaces. End-user segmentation underscores differing risk profiles and compliance needs across industries such as BFSI, healthcare, IT & telecom, manufacturing, and government. Across all segments, demand is shaped by threat complexity, regulatory obligations, digital transformation intensity, and internal security maturity. Decision-makers increasingly evaluate MDR offerings not only on detection coverage, but also on response automation, integration flexibility, and sector-specific threat intelligence, making segmentation analysis critical for understanding adoption behavior and competitive positioning.

The Managed Detection & Response Services Market by type is primarily categorized into Endpoint Detection & Response (EDR)-based MDR, Network Detection & Response (NDR)-based MDR, Cloud & Identity-focused MDR, and Fully Integrated MDR platforms. Endpoint-based MDR currently represents the leading segment, accounting for approximately 41% of total adoption, as endpoints remain the most frequently targeted attack vector. Organizations prioritize endpoint visibility due to high volumes of phishing, malware, and credential-based attacks, with enterprises monitoring an average of 2.5 endpoints per employee. Fully Integrated MDR platforms, combining endpoint, network, cloud, and identity telemetry, are the fastest-growing type, expanding at an estimated 26.8% CAGR, driven by the shift toward hybrid IT environments and unified security operations. These platforms reduce investigation time by over 40% through centralized threat correlation and automated response playbooks. Network-focused MDR and cloud & identity MDR services together account for a combined 34% share, addressing east–west traffic visibility and cloud workload protection, particularly in regulated and cloud-native enterprises.

By application, the Managed Detection & Response Services Market is segmented into endpoint security monitoring, network security monitoring, cloud workload protection, identity threat detection, and application-layer security. Endpoint security monitoring remains the dominant application, accounting for approximately 38% of total deployments, due to persistent endpoint-based attack vectors and the rise of remote and hybrid workforces. In comparison, network security monitoring accounts for about 24%, while cloud workload protection represents 21% of adoption. Cloud workload protection is the fastest-growing application, advancing at an estimated 27.4% CAGR, supported by rapid enterprise migration to multi-cloud architectures and containerized environments. Organizations leveraging cloud-focused MDR report up to 44% improvement in visibility across SaaS and IaaS platforms. The remaining applications, including identity and application-layer monitoring, collectively contribute around 17%, playing a critical role in zero-trust and identity-first security strategies. From an adoption perspective, in 2024, over 46% of global enterprises reported piloting MDR solutions specifically for cloud and identity protection use cases. Additionally, more than 40% of organizations indicated higher trust in security providers offering application-aware threat detection.

End-user segmentation of the Managed Detection & Response Services Market includes BFSI, healthcare, IT & telecom, manufacturing, government, and other commercial enterprises. The BFSI sector is the leading end-user, accounting for approximately 26% of total MDR adoption, driven by high-value data assets, strict compliance requirements, and continuous exposure to fraud and ransomware threats. Healthcare follows closely at 21%, reflecting the sector’s vulnerability to data breaches and operational disruptions. Manufacturing is the fastest-growing end-user segment, expanding at an estimated 25.9% CAGR, fueled by increased digitalization of industrial systems and rising attacks on operational technology environments. IT & telecom and government sectors together contribute a combined 33% share, leveraging MDR to secure large-scale networks, cloud platforms, and national digital infrastructure. In terms of adoption trends, in 2024, more than 49% of enterprises with over 1,000 employees reported using MDR services as part of a co-managed SOC model. Additionally, 43% of healthcare organizations indicated active testing of MDR solutions integrated with electronic health record systems.

North America accounted for the largest market share at 41.6% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 26.9% between 2025 and 2032.

North America’s leadership is supported by high enterprise cybersecurity spending, mature SOC outsourcing models, and strong adoption across BFSI, healthcare, and government sectors. Europe followed with an estimated 28.4% share in 2024, driven by regulatory compliance mandates and cross-border digital infrastructure. Asia-Pacific represented approximately 21.9% of the global market, with rapid enterprise digitalization and cloud migration accelerating MDR uptake across emerging economies. South America and the Middle East & Africa together accounted for the remaining 8.1%, reflecting early-stage adoption but increasing demand due to rising cyber incidents, national digital transformation programs, and sector-specific security requirements. Regional disparities are primarily influenced by regulatory maturity, cloud penetration rates, enterprise IT complexity, and availability of skilled cybersecurity professionals.

North America holds the dominant regional position with an estimated 41.6% market share, reflecting widespread adoption of outsourced and co-managed SOC models. Key demand-driving industries include BFSI, healthcare, defense, cloud service providers, and retail, collectively accounting for over 68% of regional MDR deployments. Regulatory frameworks emphasizing breach disclosure timelines and data protection have accelerated MDR adoption, particularly among financial institutions and hospitals. Technological advancements such as AI-driven threat hunting, SOAR-enabled automation, and XDR integration are now used by more than 62% of large enterprises in the region. Local players are expanding 24/7 monitoring capacity and vertical-specific MDR offerings to address compliance-heavy sectors. Consumer behavior shows higher enterprise adoption in healthcare and finance, where over 54% of organizations rely on external MDR partners for continuous monitoring and rapid incident response.

Europe accounts for approximately 28.4% of the global Managed Detection & Response Services Market, with strong adoption across Germany, the UK, and France. Regulatory bodies enforcing data protection, operational resilience, and cyber incident reporting have made MDR services a critical component of enterprise security strategies. Financial services, energy, and public-sector organizations together contribute nearly 60% of regional demand. Adoption of emerging technologies such as privacy-preserving analytics and explainable AI is increasing, with over 47% of enterprises prioritizing transparent threat detection models. Local MDR providers are investing in multilingual SOC operations and regional threat intelligence hubs to address cross-border cyber risks. Regional consumer behavior reflects heightened sensitivity to regulatory compliance, driving demand for auditable, explainable MDR solutions.

Asia-Pacific ranks as the fastest-growing regional market, contributing around 21.9% of global demand and rapidly closing the gap with mature regions. China, India, and Japan are the top consuming countries, together accounting for over 65% of regional MDR adoption. Expansion of cloud infrastructure, e-commerce platforms, and digital banking has increased attack surfaces across enterprises. Technology hubs in Singapore, Bengaluru, and Tokyo are driving innovation in cloud-native MDR and AI-based threat detection. Local providers are scaling managed SOC services for mid-sized enterprises, which represent nearly 52% of new regional customers. Consumer behavior shows growth driven by e-commerce platforms and mobile-first digital ecosystems, where rapid threat response is critical to maintaining service continuity.

South America accounts for an estimated 5.1% of the global market, with Brazil and Argentina leading regional adoption. Financial services, telecommunications, and energy sectors are primary drivers, together contributing over 58% of MDR usage. Infrastructure modernization and digital payment expansion have increased exposure to cyber threats, prompting enterprises to adopt managed security services. Government-backed digital inclusion initiatives and cross-border trade agreements are encouraging investment in cybersecurity capabilities. Local providers are focusing on cost-optimized MDR solutions for mid-market enterprises. Consumer behavior indicates demand tied to media platforms, financial applications, and language-localized security support models.

The Middle East & Africa region represents approximately 3.0% of global MDR demand, with the UAE and South Africa emerging as key growth markets. Demand is driven by oil & gas, utilities, government, and large construction projects, which account for nearly 63% of regional deployments. National digital transformation agendas and smart city initiatives are accelerating adoption of managed security services. Technological modernization includes increased use of cloud SOCs and AI-assisted threat monitoring. Local players are forming partnerships with global MDR vendors to expand regional coverage. Consumer behavior varies by sector, with government and critical infrastructure operators prioritizing resilience and continuous monitoring.

United States – 34.8% Market Share: Strong enterprise demand, high cybersecurity spending, and widespread adoption of co-managed SOC and MDR models.

Germany – 9.6% Market Share: High regulatory compliance requirements and advanced industrial digitalization driving consistent MDR adoption across enterprises.

The Managed Detection & Response Services Market exhibits a moderately consolidated competitive structure, characterized by the presence of a limited number of global leaders alongside a large base of regional and niche providers. Globally, over 120 active MDR providers operate across North America, Europe, and Asia-Pacific, offering services that range from endpoint-focused monitoring to fully integrated, AI-driven SOC operations. The top five companies collectively account for approximately 55% of total deployments, reflecting strong brand trust, global SOC coverage, and deep threat-intelligence capabilities, while the remaining market remains fragmented among specialized vendors and regional managed security service providers.

Competition is primarily driven by service depth, automation maturity, response time guarantees, and integration breadth rather than pricing alone. Strategic initiatives are accelerating consolidation, with more than 18 mergers, acquisitions, or strategic partnerships recorded between 2023 and 2024, aimed at expanding SOC capacity, enhancing AI-driven threat analytics, and strengthening cloud-native MDR capabilities. Product innovation is heavily focused on XDR-integrated MDR platforms, SOAR automation, and identity-centric threat detection, with over 60% of leading vendors now offering unified endpoint, network, cloud, and identity telemetry. Market positioning increasingly favors providers that deliver vertical-specific MDR solutions for BFSI, healthcare, and government sectors, where compliance alignment and rapid incident response are decisive factors.

Arctic Wolf

Sophos

Palo Alto Networks

Trustwave

eSentire

Red Canary

Technology evolution is fundamentally reshaping the Managed Detection & Response Services Market, with a strong shift toward automation, AI-driven analytics, and unified security telemetry. Artificial intelligence and machine learning are now embedded across detection pipelines, enabling behavioral analysis, anomaly detection, and predictive threat scoring. Approximately 67% of MDR providers deploy machine-learning models to reduce false positives, achieving alert noise reduction rates exceeding 45% in enterprise environments.

The convergence of MDR with Extended Detection and Response (XDR) is a major technological inflection point. XDR-enabled MDR platforms correlate data across endpoints, networks, cloud workloads, email, and identity layers, reducing investigation cycles by 40–50% compared to siloed security tools. Additionally, SOAR (Security Orchestration, Automation, and Response) technologies are increasingly embedded into MDR offerings, with automated playbooks now handling over 55% of tier-1 security incidents without human intervention.

Cloud-native MDR architectures are gaining traction, particularly in multi-cloud and hybrid IT environments. More than 70% of newly deployed MDR platforms in 2024 were cloud-delivered, enabling scalability across thousands of endpoints and real-time global threat intelligence sharing. Identity threat detection and zero-trust alignment are emerging as critical capabilities, with identity-based attacks accounting for over 30% of detected incidents handled by MDR providers. Collectively, these technologies are transforming MDR from reactive monitoring services into proactive, intelligence-led cyber defense platforms.

In January 2025, Sophos MDR expanded its global footprint with a 37% increase in customers during 2024, now protecting more than 26,000 organisations worldwide and introducing enhanced AI-assisted workflows and integrations to strengthen threat detection and incident response. Source: www.sophos.com

In 2024, CrowdStrike was named a Leader in the IDC MarketScape: Worldwide Managed Detection and Response 2024 Vendor Assessment, highlighting its 24/7 MDR service powered by the Falcon® platform and elite threat intelligence for proactive defence operations. Source: www.crowdstrike.com

In December 2024, SonicWall and CrowdStrike launched a new collaborative Managed Detection and Response (MDR) offering designed to provide scalable, AI-powered security solutions tailored for managed service providers (MSPs) serving SMBs, combining advanced endpoint protection with 24/7 SOC support. Source: www.prnewswire.com

In 2024, Rapid7 enhanced its MDR services by strengthening endpoint prevention and real-time detection capabilities, enabling enterprises to address increasingly sophisticated cyber threats more effectively.

The Managed Detection & Response Services Market Report provides a comprehensive assessment of the global MDR ecosystem, covering service types, deployment models, applications, end-user industries, and geographic regions. The scope includes analysis of MDR service types such as endpoint-focused MDR, network-based MDR, cloud and identity-centric MDR, and fully integrated XDR-enabled MDR platforms. Application coverage spans endpoint security monitoring, network traffic analysis, cloud workload protection, identity threat detection, and application-layer security monitoring across hybrid IT environments.

Geographically, the report evaluates market dynamics across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, with country-level insights for key markets including the United States, Germany, the United Kingdom, China, India, Japan, Brazil, and the UAE. Industry focus areas include BFSI, healthcare, IT & telecom, manufacturing, government, retail, and energy, which together represent more than 85% of MDR deployments globally.

The report also examines technology adoption trends, including AI-driven threat analytics, SOAR automation, XDR convergence, zero-trust integration, and cloud-native SOC architectures. Emerging and niche segments such as MDR for operational technology environments, managed identity detection, and co-managed SOC models for mid-sized enterprises are also within scope. Overall, the report is designed to support strategic planning, vendor evaluation, investment assessment, and long-term cybersecurity decision-making for enterprise leaders and industry stakeholders.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 4,100.0 Million |

| Market Revenue (2032) | USD 22,188.1 Million |

| CAGR (2025–2032) | 23.5% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory Overview, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | CrowdStrike; IBM Security; Rapid7; Secureworks; Arctic Wolf; Sophos; Palo Alto Networks; Trustwave; eSentire; Red Canary |

| Customization & Pricing | Available on Request (10% Customization Free) |