Reports

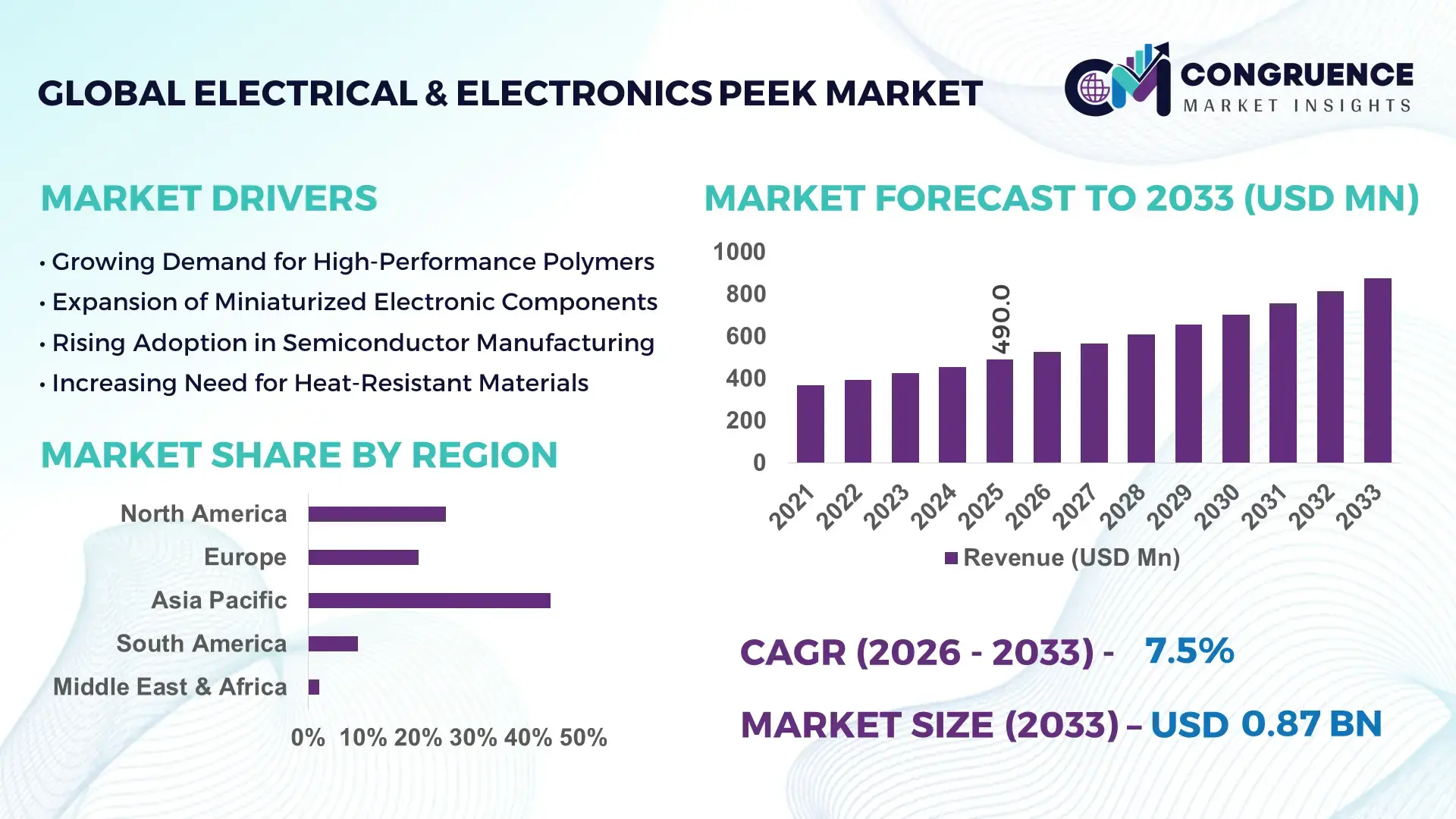

The Global Electrical & Electronics PEEK Market was valued at USD 490 Million in 2025 and is anticipated to reach a value of USD 873.9 Million by 2033 expanding at a CAGR of 7.5% between 2026 and 2033. The expansion is supported by the increasing deployment of high-temperature resistant polymer components in advanced semiconductor devices and compact electronic systems.

In China, the electrical and electronics PEEK industry is supported by extensive advanced polymer processing capacity and large electronics manufacturing ecosystems. The country operates more than 30 high-performance thermoplastic processing facilities dedicated to precision connectors, electronic housings, and insulation components. Annual production output of electronic assemblies exceeds 3.8 billion units, with high-performance polymers increasingly integrated into semiconductor testing fixtures and circuit protection systems. Investments in advanced materials production have surpassed USD 2.5 billion across several industrial manufacturing zones specializing in engineering plastics. In addition, adoption of PEEK in high-temperature electrical insulation components within electronics manufacturing lines has crossed an estimated 40% in specialized production environments focused on next-generation devices.

Market Size & Growth: Valued at USD 490 Million in 2025 and projected to reach USD 873.9 Million by 2033, growing at a CAGR of 7.5%, driven by increasing demand for durable, high-performance polymer materials in semiconductor equipment and next-generation electronic systems.

Top Growth Drivers: High-temperature electronics adoption 38%, demand for miniaturized connectors 34%, and reliability improvement in circuit protection components 29%.

Short-Term Forecast: By 2028, manufacturers anticipate up to 18% improvement in component durability and approximately 14% reduction in maintenance cycles using advanced PEEK materials in electrical assemblies.

Emerging Technologies: Advanced polymer compounding technologies, micro-precision injection molding for electronic connectors, and high-frequency compatible dielectric materials for modern electronics infrastructure.

Regional Leaders: Asia-Pacific expected to surpass USD 410 Million by 2033 due to strong electronics manufacturing clusters; North America projected near USD 220 Million supported by aerospace electronics integration; Europe estimated around USD 165 Million driven by industrial automation and smart factory adoption.

Consumer / End-User Trends: Semiconductor equipment manufacturers, telecom hardware developers, and industrial electronics OEMs are increasingly adopting PEEK for connectors, insulation, and high-load electronic components.

Pilot or Case Example: In 2024, a high-reliability electronics production initiative reported a 21% efficiency improvement and reduced operational downtime by 16% after integrating reinforced PEEK components in equipment systems.

Competitive Landscape: Market leader Victrex holds approximately 32% share, followed by Solvay, Evonik Industries, Arkema, and Panjin Zhongrun High Performance Polymers.

Regulatory & ESG Impact: Compliance with strict electronic safety standards, sustainable polymer recycling initiatives, and policies encouraging lightweight energy-efficient electronic materials are shaping procurement decisions.

Investment & Funding Patterns: More than USD 1.1 Billion has recently been invested globally in advanced polymer processing facilities, electronics materials innovation, and high-performance manufacturing infrastructure.

Innovation & Future Outlook: Expanding use of PEEK in high-frequency communication systems, electric mobility electronics, and advanced semiconductor packaging is expected to influence next-generation materials adoption.

The Electrical & Electronics PEEK market continues to expand across semiconductor fabrication equipment, telecommunications infrastructure, consumer electronics hardware, and industrial automation technologies. Semiconductor manufacturing equipment accounts for roughly 35% of advanced material utilization, while telecom and connectivity infrastructure contributes nearly 25% of demand for high-performance polymers. Recent innovations include glass-fiber reinforced PEEK grades offering improved dielectric strength and carbon-filled variants designed for electrostatic discharge protection in sensitive electronic systems. Environmental regulations promoting energy-efficient electronic components and durable materials are encouraging manufacturers to integrate high-temperature polymers into modern electronics design. Regionally, Asia-Pacific maintains strong consumption due to large-scale electronics production, while North America and Europe are accelerating adoption in aerospace electronics and advanced control systems. Future growth is closely tied to next-generation computing devices, high-speed communication technologies, and compact electronic architecture requiring durable, thermally stable engineering materials.

The Electrical & Electronics PEEK Market has become strategically relevant as manufacturers seek high-performance materials capable of withstanding extreme thermal, electrical, and mechanical stress in next-generation electronics production. PEEK polymers are increasingly specified for semiconductor processing equipment, connectors, and insulating components due to their thermal stability above 250°C and superior dielectric performance. In advanced electronics manufacturing environments, micro-precision molded PEEK components reduce system wear and improve operational stability in high-density circuit assemblies. Advanced polymer compounding technology delivers 28% improvement in electrical insulation durability compared to conventional high-temperature nylon standards used in legacy electronic housings.

Regionally, Asia-Pacific dominates in volume manufacturing due to large-scale electronics production clusters, while North America leads in adoption with nearly 46% of semiconductor equipment manufacturers integrating high-performance polymers into critical assemblies. By 2028, AI-driven smart manufacturing and automated quality inspection systems are expected to improve defect detection efficiency by approximately 22% in facilities producing precision electrical components using advanced PEEK materials. Firms are committing to sustainability targets such as 30% recyclable engineering plastics integration by 2030 to meet environmental and regulatory expectations across electronics supply chains. In 2024, Japan achieved a 19% improvement in semiconductor equipment reliability through advanced high-temperature polymer component upgrades in electronics production lines. The Electrical & Electronics PEEK Market is therefore evolving into a critical pillar of resilience, compliance, and sustainable growth within the global electronics manufacturing ecosystem.

The rapid expansion of semiconductor manufacturing facilities worldwide is significantly driving the demand for high-performance polymers such as PEEK in electrical and electronic applications. Semiconductor fabrication equipment operates under extreme temperatures and requires materials that maintain structural integrity and electrical insulation during continuous production cycles. PEEK components are widely used in wafer processing equipment, chip testing fixtures, and electrical connectors due to their ability to withstand temperatures exceeding 250°C and resist chemical exposure during manufacturing processes. Globally, more than 80 advanced semiconductor fabrication projects have been announced or developed in recent years, increasing demand for specialized materials used in precision electronic equipment. Additionally, miniaturized semiconductor packaging technologies require materials with high dimensional stability, which PEEK provides in micro-engineered components. The growing complexity of integrated circuits and electronic modules further strengthens the role of advanced engineering polymers in maintaining operational reliability and improving production efficiency within semiconductor manufacturing ecosystems.

Despite its superior performance characteristics, the Electrical & Electronics PEEK Market faces restraints associated with high production costs and complex processing requirements. Manufacturing PEEK involves advanced polymerization processes requiring specialized equipment capable of handling high temperatures and strict quality control standards. Processing temperatures often exceed 350°C, which increases energy consumption and limits the number of facilities capable of producing high-quality PEEK components for electronics applications. Compared to standard engineering plastics such as polyamide or polycarbonate, PEEK materials can cost several times more per kilogram, making adoption challenging for cost-sensitive electronics manufacturers. In addition, precision molding of micro-electronic components requires advanced tooling and specialized manufacturing expertise. Supply chain limitations in high-performance polymers also affect material availability during periods of high demand from aerospace and semiconductor sectors. These economic and technical constraints can slow broader adoption of PEEK in certain electronic product categories, particularly in mass-market consumer electronics manufacturing.

The rapid development of next-generation electronics, including high-frequency communication systems, electric mobility electronics, and advanced computing hardware, is creating significant opportunities for the Electrical & Electronics PEEK Market. Modern communication infrastructure such as 5G and emerging 6G research requires materials with stable dielectric properties and resistance to thermal deformation under continuous operation. PEEK materials provide consistent performance in high-frequency environments, making them suitable for connectors, antenna components, and insulation elements in advanced communication equipment. Additionally, electric vehicles increasingly integrate complex power electronics and battery management systems that require durable insulation materials capable of operating in harsh electrical environments. Global production of electric vehicles surpassed 14 million units annually, contributing to increased demand for reliable electronic components and associated materials. Emerging technologies such as miniaturized sensors, high-performance computing modules, and smart industrial electronics further expand the application scope of PEEK polymers across advanced electronics manufacturing sectors.

Regulatory compliance and stringent qualification standards present ongoing challenges for the Electrical & Electronics PEEK Market, particularly in high-reliability electronic applications such as aerospace electronics, medical electronics, and semiconductor manufacturing systems. Electrical insulation materials must comply with strict safety certifications, flammability standards, and long-term durability testing before integration into electronic products. Qualification processes for new materials in semiconductor equipment and industrial electronics can take several years due to reliability testing under extreme temperature, voltage, and environmental conditions. Additionally, international environmental regulations related to sustainable manufacturing and recycling of engineering plastics require manufacturers to redesign materials and production methods. Electronics companies increasingly demand traceability and lifecycle performance verification for materials used in critical components. These requirements increase development timelines and operational costs for manufacturers producing specialized PEEK materials for electronics applications, creating barriers for new entrants while raising compliance responsibilities across the industry.

• Rapid Growth in High-Temperature Electronic Components Adoption:

The demand for high-temperature resistant materials in advanced electronics manufacturing has increased significantly, with nearly 48% of new semiconductor equipment designs incorporating high-performance polymers such as PEEK. Electronics manufacturers report up to 32% improvement in component reliability when replacing conventional engineering plastics with advanced thermoplastics in high-load electrical assemblies. Additionally, more than 60% of precision connector manufacturers are integrating thermally stable polymer materials into next-generation electronic connectors used in industrial automation and telecommunications systems.

• Expansion of Semiconductor Fabrication Facilities:

Global semiconductor infrastructure expansion is reshaping material demand patterns, with over 80 advanced fabrication projects underway across Asia-Pacific, North America, and Europe. Approximately 44% of semiconductor equipment suppliers now utilize high-performance polymers in wafer processing and chip testing components. Precision polymer-based fixtures have demonstrated up to 27% improvement in equipment lifespan and nearly 20% reduction in thermal deformation issues during continuous high-temperature operations in electronics manufacturing facilities.

• Increasing Integration in Electric Mobility and Power Electronics:

The rapid adoption of electric mobility technologies is influencing the Electrical & Electronics PEEK market, as nearly 36% of new electric power control modules now incorporate high-performance polymer insulation components. Electric vehicle power electronics systems require materials capable of withstanding temperatures exceeding 200°C, and advanced polymer integration has improved operational efficiency of power modules by approximately 22%. Additionally, battery management systems and onboard electronic connectors show a 31% increase in usage of thermally stable engineering plastics.

• Rise in Precision Micro-Molding for Compact Electronics:

Miniaturization trends in consumer electronics and industrial devices are driving demand for micro-molded polymer components. Around 41% of electronic connector production lines have transitioned to high-precision micro-injection molding technologies designed for advanced thermoplastics. These manufacturing methods have improved dimensional accuracy by nearly 25% and reduced component failure rates by approximately 18% in high-density circuit assemblies used in modern communication hardware and compact computing devices.

The Electrical & Electronics PEEK Market is segmented based on type, application, and end-user industries, reflecting diverse adoption patterns across advanced electronics manufacturing ecosystems. Product types primarily include unfilled PEEK, carbon-filled PEEK, glass-filled PEEK, and other modified polymer variants designed for specialized electrical performance. Each type serves distinct roles in semiconductor processing equipment, electrical connectors, insulation systems, and precision electronic housings. From an application perspective, the market spans semiconductor manufacturing equipment, telecommunications infrastructure, consumer electronics, and industrial electronic systems. Adoption is strongly influenced by demand for materials that provide thermal stability, chemical resistance, and long-term electrical insulation. End-user segments include semiconductor manufacturers, telecom equipment providers, automotive electronics producers, and industrial automation companies. Industry data indicates that advanced electronics manufacturing clusters account for over 60% of material utilization, highlighting the importance of high-performance polymers in next-generation electronic device production and system reliability improvements.

The Electrical & Electronics PEEK market includes several product categories such as unfilled PEEK, glass-filled PEEK, carbon-filled PEEK, and other specialty-modified PEEK materials developed for advanced electrical applications. Unfilled PEEK currently accounts for approximately 38% of adoption due to its excellent dielectric strength, thermal resistance above 250°C, and stable performance in high-precision electronic components such as connectors, semiconductor fixtures, and insulation elements. Glass-filled PEEK represents nearly 27% of usage, widely adopted in structural electronic housings where improved stiffness and dimensional stability are required for high-performance electronics manufacturing systems. Carbon-filled PEEK is the fastest-growing product type, expanding at an estimated CAGR of around 9.2%, driven by increasing demand for electrostatic discharge protection and enhanced mechanical strength in semiconductor processing environments. These materials are widely utilized in electronic assemblies requiring conductivity control and improved wear resistance. Other specialized variants, including mineral-filled and reinforced PEEK materials, collectively account for nearly 35% of the market, supporting niche applications such as high-frequency electronics and aerospace electronic systems.

Applications within the Electrical & Electronics PEEK market span semiconductor equipment, telecommunications infrastructure, consumer electronics, and industrial electronics systems. Semiconductor manufacturing equipment remains the leading application segment, accounting for nearly 42% of overall adoption due to the need for materials capable of maintaining stability in high-temperature and chemically intensive fabrication processes. Telecommunications hardware represents approximately 26% of usage, driven by increasing deployment of high-frequency communication systems and advanced network infrastructure components. Industrial electronics applications are emerging as the fastest-growing segment, expanding at an estimated CAGR of 8.7% as automation systems, robotics controllers, and smart factory equipment increasingly require durable insulating materials capable of long operational cycles. Consumer electronics applications account for the remaining 32% combined share, particularly in compact device connectors, microelectronic housings, and precision circuit assembly components.

The Electrical & Electronics PEEK market serves multiple end-user industries including semiconductor manufacturers, telecommunications equipment providers, automotive electronics producers, and industrial automation companies. Semiconductor manufacturing companies represent the leading end-user group, accounting for approximately 44% of material demand due to the intensive use of high-performance polymers in wafer processing tools, chip testing systems, and high-precision electronic fixtures. Telecommunications equipment manufacturers hold around 24% of adoption as network infrastructure modernization increases demand for thermally stable connector materials and insulating components. Automotive electronics is the fastest-growing end-user segment, expanding at an estimated CAGR of 9.5%, driven by the rapid increase in electric vehicle production and advanced electronic control systems integration. Power electronics modules, battery management systems, and onboard electronic connectors increasingly require durable materials capable of operating in high-temperature electrical environments. Industrial automation, aerospace electronics, and advanced computing hardware manufacturers collectively contribute nearly 32% of the remaining market usage, reflecting expanding demand for reliable electronic component materials across multiple sectors.

Asia-Pacific accounted for the largest market share at 46% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 8.3% between 2026 and 2033.

Asia-Pacific’s leadership is supported by strong electronics manufacturing output, with more than 70% of global semiconductor assembly and testing facilities located in countries such as China, Japan, South Korea, and Taiwan. The region produces over 60% of global consumer electronics devices, which significantly increases demand for high-performance thermoplastics such as PEEK in connectors, insulation components, and semiconductor fixtures. North America accounted for nearly 24% of the global Electrical & Electronics PEEK market, supported by the development of more than 15 advanced semiconductor fabrication projects and increased adoption of high-performance materials in aerospace and defense electronics. Europe held approximately 20% share, driven by industrial automation growth and strict electronic material standards across Germany, France, and the United Kingdom. South America represented around 6% share, while the Middle East & Africa collectively accounted for nearly 4%, primarily supported by expanding electronics assembly operations and industrial modernization programs in emerging markets.

How are advanced electronics manufacturing upgrades shaping high-performance polymer adoption?

North America holds approximately 24% share of the global Electrical & Electronics PEEK market, supported by strong semiconductor equipment manufacturing and aerospace electronics industries. The region has more than 40 advanced electronics research and development facilities developing high-performance materials for next-generation electronic systems. Government initiatives aimed at strengthening semiconductor supply chains and electronics manufacturing have led to increased adoption of durable polymer components used in wafer processing equipment and electrical insulation systems. Digital transformation in electronics manufacturing has resulted in nearly 35% of production facilities implementing automated precision molding technologies for high-performance thermoplastics. A notable industry example includes Victrex collaborating with electronics manufacturers to supply specialized polymer grades for semiconductor equipment components. Consumer behavior trends show higher enterprise adoption in aerospace electronics, telecommunications infrastructure, and financial data center hardware requiring reliable and thermally stable electronic materials.

What factors are accelerating advanced material demand across highly regulated electronics industries?

Europe represents approximately 20% of the global Electrical & Electronics PEEK market, driven by strong industrial electronics production and advanced manufacturing sectors in Germany, the United Kingdom, and France. The region hosts more than 25 specialized facilities producing high-performance engineering polymers for use in electrical systems and semiconductor equipment. Strict sustainability and electronic safety standards implemented by regulatory authorities across Europe are encouraging manufacturers to adopt durable and recyclable polymer materials in electronics production. Nearly 30% of electronics manufacturing companies in the region are transitioning toward advanced thermoplastic materials to improve system longevity and environmental compliance. A regional industry example includes Solvay developing specialized polymer materials for electrical insulation and high-frequency electronic applications. Consumer behavior variations indicate that regulatory pressure and sustainability requirements are significantly influencing procurement strategies among European electronics manufacturers.

Why is large-scale electronics manufacturing accelerating high-performance material consumption?

Asia-Pacific leads the Electrical & Electronics PEEK market in volume consumption, accounting for approximately 46% of global demand. The region includes major electronics manufacturing economies such as China, India, Japan, and South Korea, collectively operating over 100 semiconductor fabrication and advanced electronics assembly facilities. Rapid expansion in consumer electronics production and telecommunications infrastructure has resulted in nearly 58% of new electronic component manufacturing lines integrating high-performance thermoplastics for insulation and connector systems. Innovation hubs in countries like Japan and South Korea continue investing in advanced materials research for semiconductor processing equipment and high-frequency electronics. A key regional player, Panjin Zhongrun High Performance Polymers, is expanding production capacity to support the growing demand for engineering plastics used in electrical components. Consumer behavior trends show strong demand for compact electronic devices and advanced connectivity technologies driving material adoption across the region.

How are industrial electronics modernization and trade incentives influencing advanced material demand?

South America accounts for roughly 6% of the global Electrical & Electronics PEEK market, with Brazil and Argentina serving as the primary markets for electronics manufacturing and industrial automation systems. The region has seen the development of more than 15 electronics assembly facilities focused on telecommunications hardware, consumer electronics, and industrial electronic equipment. Infrastructure modernization initiatives and government trade incentives supporting electronics production have encouraged manufacturers to adopt durable polymer materials for connectors and electrical insulation systems. Increasing deployment of telecommunications networks and smart energy infrastructure is also contributing to higher demand for high-performance electronic components. Regional consumer behavior indicates growing demand for localized electronics manufacturing and improved device reliability. Additionally, import substitution policies in several countries are encouraging the adoption of advanced materials that enhance durability and performance of locally produced electronic devices.

What role do industrial diversification and technology upgrades play in shaping advanced material adoption?

The Middle East & Africa region represents approximately 4% of the global Electrical & Electronics PEEK market, supported by increasing investments in industrial electronics, energy infrastructure, and technology modernization. Countries such as the United Arab Emirates and South Africa are expanding electronics assembly operations and integrating advanced materials in industrial equipment. The region has introduced several initiatives to promote technology-driven manufacturing, resulting in nearly 20% growth in electronics assembly capacity in selected industrial zones. Demand for durable electrical components is also influenced by oil and gas automation systems and energy infrastructure requiring reliable insulation materials capable of withstanding harsh operating conditions. Trade partnerships and regulatory modernization programs are improving access to advanced materials used in electrical equipment manufacturing. Consumer behavior trends indicate increasing adoption of smart devices and industrial monitoring systems, which further supports demand for high-performance polymers in electronic applications.

China – 32% share in the Electrical & Electronics PEEK market due to extensive electronics manufacturing capacity and strong semiconductor assembly infrastructure.

United States – 18% share in the Electrical & Electronics PEEK market supported by advanced semiconductor equipment production and high adoption of specialized electronic materials across aerospace and data center industries.

The Electrical & Electronics PEEK market is characterized by a moderately consolidated competitive structure, with approximately 20–25 active global and regional manufacturers supplying high-performance PEEK materials specifically engineered for electronic and electrical applications. The top five companies collectively account for nearly 58% of the total market presence, reflecting strong technological capabilities, proprietary polymer processing expertise, and long-term supply agreements with semiconductor and electronics manufacturers. Leading participants compete primarily on advanced material performance, thermal resistance above 250°C, dielectric stability, and precision polymer compounding technologies designed for microelectronic components.

Competition has intensified as electronics miniaturization accelerates, prompting companies to expand specialized production capacity. Over the past three years, more than 12 new product variants of reinforced or conductive PEEK grades have been introduced to address semiconductor fabrication equipment, 5G infrastructure hardware, and high-frequency electronics assemblies. Strategic initiatives include joint development programs with electronics OEMs, technology partnerships with semiconductor equipment manufacturers, and expansion of polymer processing facilities in Asia-Pacific and North America. Several producers have also increased research spending by an estimated 18% to enhance advanced polymer formulations suitable for next-generation electronic systems. Innovation trends such as carbon-filled conductive materials, glass-fiber reinforced PEEK, and electrostatic discharge protection polymers are shaping competitive differentiation. Additionally, supply chain integration strategies and long-term contracts with electronics manufacturing clusters are becoming key factors influencing market positioning and industry competition.

Victrex plc

Solvay

Evonik Industries AG

Arkema Group

Ensinger GmbH

RTP Company

SABIC

Zeus Industrial Products

Advanced material engineering and precision polymer processing technologies are significantly shaping the Electrical & Electronics PEEK market. High-performance thermoplastics such as PEEK are increasingly integrated into semiconductor fabrication equipment, high-frequency connectors, and advanced insulation systems because they can withstand continuous temperatures above 250°C while maintaining electrical stability. Recent developments in micro-injection molding allow manufacturers to produce components with dimensional tolerances below 20 microns, enabling the production of compact electronic connectors and microelectronic housings used in high-density circuit assemblies. Approximately 40% of advanced semiconductor tool components now utilize reinforced PEEK grades due to their resistance to aggressive chemicals used in wafer processing environments.

Additive manufacturing has also emerged as a transformative technology, with industrial 3D printing systems capable of processing PEEK materials at temperatures exceeding 400°C. Around 18% of specialized electronic prototyping applications now rely on high-temperature additive manufacturing to accelerate component testing cycles and reduce development timelines by nearly 25%. Conductive and carbon-filled PEEK formulations are gaining traction in electrostatic discharge-sensitive environments such as semiconductor cleanrooms, where static control is critical for device reliability. Additionally, digital simulation tools and AI-assisted material design platforms are helping polymer manufacturers develop new grades optimized for electrical insulation strength and long-term durability. Continuous innovation in polymer compounding, precision molding automation, and semiconductor equipment integration is strengthening the technological foundation of the Electrical & Electronics PEEK market.

• In March 2025, Victrex expanded its high-performance polymer solutions for semiconductor and electronics applications, focusing on advanced PEEK grades designed for miniaturized electronic components and wafer processing systems, supporting improved thermal resistance and durability in next-generation electronics manufacturing. Source: www.victrex.com

• In September 2024, Solvay announced advancements in specialty polymers used in high-performance electrical systems, including materials supporting electrification and electronics reliability, with enhanced insulation properties and improved resistance to extreme processing environments used in advanced manufacturing sectors. Source: www.solvay.com

• In May 2025, Evonik Industries AG reported progress in high-performance polymer solutions for electronics and semiconductor manufacturing equipment, highlighting innovations that improve component stability in high-temperature environments and support the expansion of advanced electronics production infrastructure. Source: www.evonik.com

• In November 2024, Arkema introduced developments in specialty materials for advanced electronics manufacturing, including high-temperature resistant polymers used in precision electronic assemblies and next-generation electrical insulation components for industrial and telecommunications hardware. Source: www.arkema.com

The Electrical & Electronics PEEK Market Report provides a comprehensive assessment of industry developments across key segments, applications, and geographic regions influencing demand for high-performance thermoplastics in advanced electronics manufacturing. The report evaluates multiple product categories including unfilled PEEK, glass-filled PEEK, carbon-filled PEEK, and specialized reinforced variants used in semiconductor equipment, connectors, insulation components, and high-frequency electronic assemblies. These product types collectively support a wide range of electronics manufacturing environments where operating temperatures often exceed 200°C and reliability requirements are critical.

Geographically, the report examines market activity across Asia-Pacific, North America, Europe, South America, and the Middle East & Africa, covering more than 25 key manufacturing economies involved in electronics production and semiconductor development. The analysis highlights adoption trends in over 100 semiconductor fabrication facilities and numerous electronics assembly clusters globally. Application coverage includes semiconductor processing systems, telecommunications infrastructure, industrial automation electronics, electric mobility power electronics, and consumer electronic devices. Additionally, the report reviews emerging technologies such as advanced polymer compounding, conductive thermoplastics, precision micro-molding, and high-temperature additive manufacturing techniques used in electronic component production. The scope also includes evaluation of supply chain dynamics, innovation pipelines, and technology integration strategies influencing the development of the Electrical & Electronics PEEK market across global electronics manufacturing ecosystems.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

7.5% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Victrex plc , Solvay, Evonik Industries AG, Arkema Group, Ensinger GmbH, RTP Company , SABIC, Zeus Industrial Products |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |