Reports

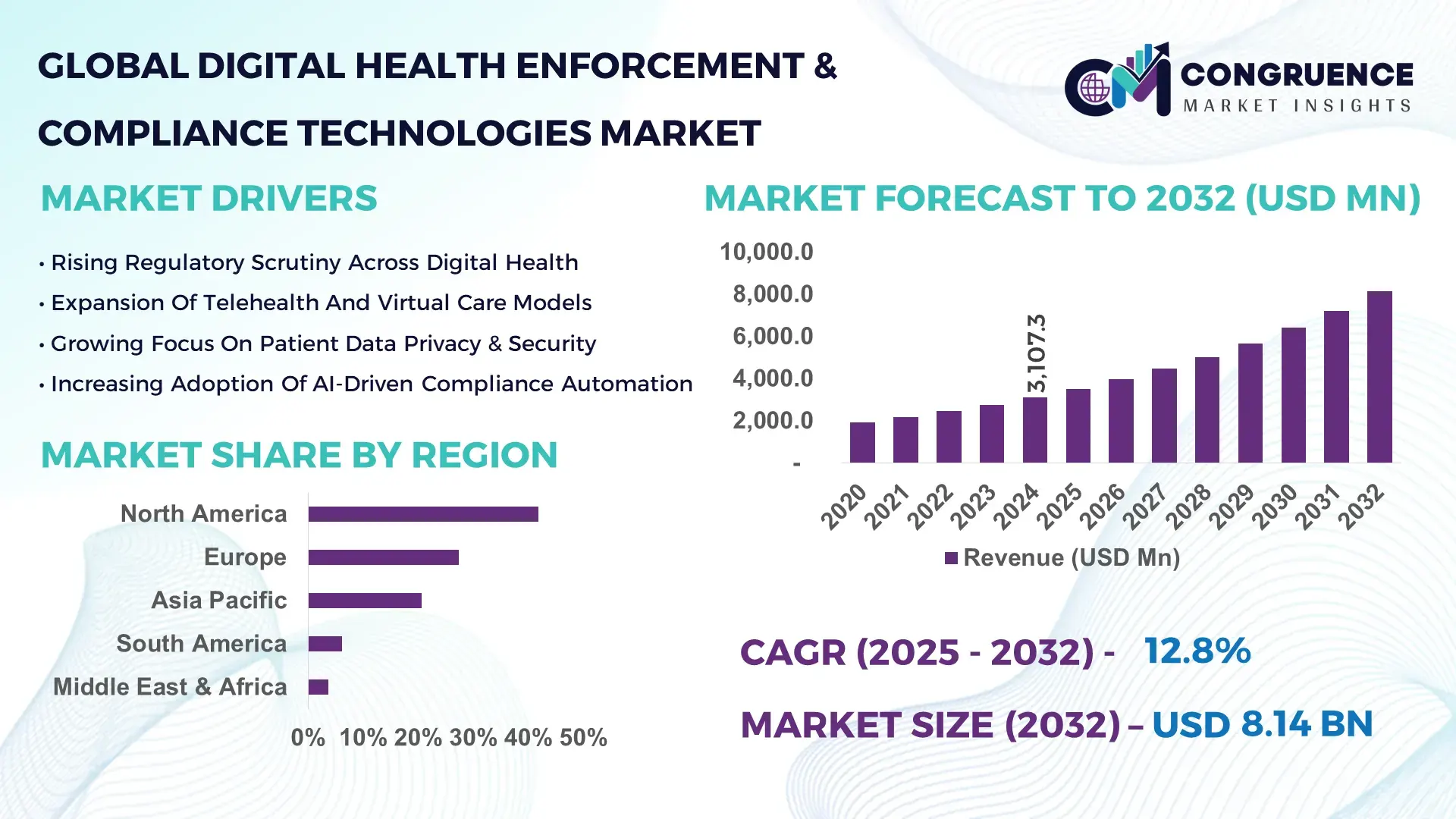

The Global Digital Health Enforcement & Compliance Technologies Market was valued at USD 3,107.3 Million in 2024 and is anticipated to reach a value of USD 8,144.3 Million by 2032 expanding at a CAGR of 12.8% between 2025 and 2032, according to an analysis by Congruence Market Insights. Growth is driven by the rapid digitization of healthcare records, increasing regulatory scrutiny, and rising cyber risk exposure across digital health ecosystems.

The United States represents the most influential country within the Digital Health Enforcement & Compliance Technologies market, supported by large-scale deployment across hospitals, payers, life sciences companies, and telehealth platforms. In 2024, more than 82% of large healthcare providers in the country operated at least one automated compliance monitoring or enforcement platform. Annual investments exceeding USD 900 million were directed toward AI-driven audit systems, real-time data governance tools, and HIPAA-aligned compliance automation. Over 65% of digital health software deployments integrated built-in compliance engines, while healthcare data volumes surpassed 2.3 zettabytes annually, reinforcing demand for scalable enforcement technologies across clinical, pharmaceutical, and insurance workflows.

Market Size & Growth: Valued at USD 3,107.3 million in 2024, projected to reach USD 8,144.3 million by 2032, driven by expanding digital health data volumes and stricter regulatory enforcement.

Top Growth Drivers: Regulatory automation adoption (48%), healthcare data digitization (42%), cyber risk mitigation demand (37%).

Short-Term Forecast: By 2028, automated compliance platforms are expected to reduce manual audit workloads by 45%.

Emerging Technologies: AI-based compliance analytics, blockchain audit trails, continuous risk monitoring engines.

Regional Leaders: North America projected at USD 3.4 billion by 2032 with hospital-led adoption; Europe at USD 2.2 billion driven by privacy compliance; Asia Pacific at USD 1.8 billion supported by digital health scale-up.

Consumer/End-User Trends: Over 58% of healthcare enterprises favor integrated enforcement platforms embedded within EHR and telehealth systems.

Pilot or Case Example: In 2023, a national health network reduced compliance violation incidents by 31% using AI-powered monitoring.

Competitive Landscape: IBM leads with approximately 18% share, followed by Oracle, SAP, Microsoft, and Salesforce.

Regulatory & ESG Impact: Data privacy mandates and ESG-driven governance reporting accelerating enforcement tool adoption.

Investment & Funding Patterns: More than USD 2.6 billion invested globally between 2022–2024 in digital health compliance platforms.

Innovation & Future Outlook: Real-time compliance orchestration and predictive risk scoring shaping next-generation solutions.

Digital Health Enforcement & Compliance Technologies are primarily deployed across healthcare providers (44%), life sciences and pharma companies (27%), and health insurers (19%). Innovations in continuous audit automation, privacy-by-design architectures, and AI-driven risk scoring are reshaping regulatory compliance, while regional adoption is reinforced by data protection laws, cybersecurity mandates, and expanding telehealth ecosystems.

The Digital Health Enforcement & Compliance Technologies Market has become strategically critical as healthcare systems increasingly depend on interoperable digital platforms, cloud-based records, and AI-driven diagnostics. These technologies enable continuous monitoring of regulatory adherence, automated audit trails, and real-time enforcement of data governance policies across clinical, administrative, and research workflows. AI-powered compliance analytics deliver up to 52% improvement in violation detection accuracy compared to traditional rule-based compliance systems.

North America dominates in deployment volume due to advanced healthcare IT infrastructure, while Europe leads in adoption density with over 61% of digital health enterprises actively using automated compliance tools. By 2027, predictive compliance engines leveraging machine learning are expected to cut regulatory incident response times by 38%. Strategically, organizations are shifting from reactive compliance checks to proactive enforcement architectures embedded directly within digital health platforms.

ESG and governance considerations further elevate strategic relevance. Healthcare organizations are committing to measurable governance improvements, including 40% reduction in data breach exposure and 30% improvement in audit transparency by 2030. In 2024, a national healthcare system achieved a 29% reduction in compliance-related penalties through centralized AI-based enforcement orchestration.

Future pathways emphasize cross-platform interoperability, blockchain-backed audit integrity, and AI-driven regulatory forecasting. As digital health complexity grows, the Digital Health Enforcement & Compliance Technologies Market is positioned as a foundational pillar supporting resilience, regulatory confidence, and sustainable growth across global healthcare ecosystems.

The Digital Health Enforcement & Compliance Technologies market dynamics are shaped by accelerating healthcare digitization, regulatory expansion, and rising cybersecurity threats. Increasing use of electronic health records, telemedicine platforms, and AI-driven diagnostics has amplified regulatory exposure across data privacy, patient safety, and operational governance. Enforcement technologies are evolving from static compliance checklists to dynamic, real-time monitoring systems. Vendor competition focuses on scalability, interoperability, and automation depth. Regulatory harmonization challenges and regional data residency requirements further influence adoption strategies, making compliance technologies essential infrastructure components rather than optional add-ons.

Regulatory expansion across data privacy, clinical safety, and digital therapeutics has emerged as a primary growth driver. In 2024, healthcare organizations faced an average of 17 distinct regulatory frameworks spanning data protection, patient consent, and interoperability. Automated enforcement platforms reduced non-compliance events by up to 34% by continuously monitoring system behavior. Over 63% of digital health enterprises adopted AI-driven compliance tools to manage regulatory complexity across jurisdictions. These measurable efficiencies directly support sustained market expansion.

Integration complexity remains a key restraint, particularly for legacy healthcare IT environments. Nearly 41% of healthcare providers operate fragmented systems, complicating real-time enforcement deployment. Integration projects can extend implementation timelines by 6–9 months, increasing operational costs. Smaller providers often lack in-house technical expertise, limiting adoption speed. These barriers slow market penetration despite strong regulatory pressure.

Cloud-native healthcare platforms unlock significant opportunities for enforcement technologies. Over 58% of newly deployed healthcare applications in 2024 were cloud-based, enabling centralized compliance orchestration. Cloud-native enforcement tools improved scalability by 46% and reduced infrastructure overhead by 33%. Expanding adoption among digital-first health startups and regional health networks creates a growing addressable market for modular compliance solutions.

Cyber threats continue to challenge enforcement effectiveness. Healthcare experienced a 21% rise in advanced persistent threats targeting patient data systems in 2024. Compliance tools must continuously adapt to new attack vectors, increasing development and maintenance costs. Skill shortages in cybersecurity and regulatory technology further strain implementation, requiring ongoing investment to maintain enforcement accuracy.

AI-Driven Continuous Compliance Monitoring: Over 67% of healthcare enterprises adopted continuous compliance engines in 2024, reducing manual audit cycles by 44% and enabling real-time policy enforcement across digital health platforms.

Blockchain-Based Audit Trails: Approximately 29% of new compliance deployments incorporated blockchain-ledgers, improving audit integrity by 38% and reducing data tampering incidents by 31%.

Integrated Privacy-by-Design Architectures: Privacy-embedded compliance frameworks were implemented in 54% of new digital health applications, cutting consent management errors by 36%.

Automation of Regulatory Reporting: Automated reporting tools reduced regulatory submission preparation time by 47%, supporting faster response to compliance audits and inspections.

The Digital Health Enforcement & Compliance Technologies market is segmented by type, application, and end-user, reflecting varied regulatory exposure across healthcare ecosystems. Product types differ by enforcement depth and automation level. Applications span clinical operations, pharmaceutical compliance, and payer governance. End-user demand varies based on data intensity, regulatory complexity, and digital maturity, shaping distinct adoption patterns across segments.

Compliance management platforms lead adoption with approximately 46% share due to their ability to centralize audit workflows and policy enforcement. However, AI-driven risk analytics systems are the fastest-growing type, expanding at over 14% CAGR, driven by predictive violation detection and real-time alerts. Identity and access enforcement tools and data governance solutions collectively account for 54%, serving niche security and privacy functions.

In 2025, AI-powered compliance analytics were deployed across national healthcare data exchanges, improving violation detection accuracy for over 12 million records.

Healthcare provider compliance accounts for 43% of application demand, supported by hospital digitization and EHR adoption. Pharmaceutical and life sciences compliance is the fastest-growing application, expanding above 15% CAGR due to digital trial oversight and regulatory reporting automation. Payer and insurance compliance and telehealth governance collectively contribute 57%. In 2024, 41% of hospitals piloted automated enforcement platforms to manage multi-jurisdictional regulations.

In 2024, digital compliance platforms were implemented across more than 180 healthcare networks, improving regulatory response times by 35%.

Hospitals and healthcare providers represent the largest end-user group with a 49% share, driven by high regulatory exposure and data volumes. Digital health startups and telehealth providers are the fastest-growing end-users, expanding at over 16% CAGR due to cloud-native architectures. Life sciences companies, insurers, and government health agencies collectively account for 51%. In 2024, over 39% of healthcare enterprises globally reported piloting automated compliance enforcement systems.

In 2025, mid-sized healthcare enterprises deploying AI compliance platforms achieved a 24% reduction in audit preparation time.

North America accounted for the largest market share at 41.8%in 2024 however, Asia Pacific is expected to register the fastest growth, expanding at a CAGR of 15.6% between 2025 and 2032.

North America’s dominance is supported by early digitization of healthcare infrastructure, with over 78% of hospitals using advanced electronic health record systems integrated with compliance tools. Europe followed with a 27.4% share, driven by strict data protection enforcement and cross-border health data governance. Asia Pacific contributed 20.6% of the global market, supported by large patient populations and rapid telehealth expansion. South America and Middle East & Africa collectively held 10.2%, reflecting gradual digital transformation. Globally, more than 65% of compliance technology deployments are now cloud-based, while AI-enabled enforcement modules are embedded in nearly 52% of new digital health platforms, reinforcing region-specific growth trajectories.

How is compliance automation reshaping enterprise-scale digital healthcare governance?

The market held approximately 41.8% share in 2024, reflecting strong enterprise adoption across hospitals, insurers, and life sciences firms. Healthcare delivery networks, pharmaceutical manufacturers, and health insurers collectively account for over 72% of regional demand. Regulatory mandates related to patient data protection, clinical audit readiness, and interoperability compliance have accelerated adoption, with more than 68% of providers deploying automated monitoring tools. Advanced AI-driven audit engines and real-time data loss prevention technologies are increasingly embedded into EHR and telehealth platforms. One prominent local player, Microsoft, continues expanding healthcare compliance capabilities within its cloud ecosystem, supporting automated policy enforcement across thousands of healthcare tenants. Consumer behavior shows higher institutional purchasing, with large enterprises prioritizing end-to-end compliance platforms over point solutions.

Why does explainability matter more than speed in regulatory technology adoption?

Europe accounted for nearly 27.4% of the global market in 2024, with Germany, the UK, and France representing over 58% of regional demand. Regulatory bodies emphasize transparency, auditability, and data sovereignty, driving demand for explainable compliance systems. Over 61% of healthcare enterprises prioritize solutions that provide traceable enforcement logic. Emerging technologies such as blockchain-based audit trails and federated data governance models are gaining traction. A regional player, SAP, has expanded healthcare compliance modules focused on cross-border data governance and regulatory reporting automation. Consumer behavior reflects cautious adoption, with buyers emphasizing compliance interpretability and legal defensibility over rapid deployment.

What is driving large-scale adoption across high-growth digital health ecosystems?

Asia Pacific ranked third globally by market size in 2024, contributing approximately 20.6% of global volume. China, India, and Japan together accounted for over 64% of regional demand. Rapid expansion of digital hospitals, national health ID programs, and mobile health platforms has increased compliance technology uptake. More than 55% of new digital health deployments in the region are mobile-first, requiring scalable enforcement architectures. Regional innovation hubs in Bengaluru, Shenzhen, and Tokyo are accelerating AI-based compliance analytics. Tata Consultancy Services (TCS) supports large healthcare digitization projects with integrated governance frameworks. Consumer behavior is shaped by rapid mobile adoption and cost-sensitive procurement.

How are emerging regulations shaping selective technology investments?

South America held around 6.1% of the global market in 2024, with Brazil and Argentina representing nearly 70% of regional demand. Infrastructure modernization in public healthcare systems and rising private hospital investments support gradual adoption. Government-backed digital health initiatives and regional trade frameworks are improving compliance standardization. Local IT service providers increasingly integrate compliance modules into hospital management systems. TOTVS, a regional software firm, has expanded healthcare governance features across its enterprise platforms. Consumer behavior shows selective adoption, with organizations prioritizing multilingual support and region-specific regulatory alignment.

Why is modernization driving demand despite uneven digital maturity?

The region accounted for approximately 3.7% of global demand in 2024. UAE and South Africa together contributed over 46% of regional adoption. Investments in smart hospitals, national health platforms, and cloud migration are driving compliance technology deployment. Over 38% of large healthcare facilities in the Gulf region have implemented centralized compliance dashboards. Local regulations increasingly emphasize data residency and cybersecurity. STC Solutions in the Gulf region supports healthcare clients with governance and compliance automation. Consumer behavior varies, with public-sector-led procurement in the Middle East and private healthcare-driven adoption in Africa.

United States – 36.2% market share: Dominance driven by advanced healthcare IT infrastructure and stringent regulatory oversight across providers and insurers.

Germany – 9.8% market share: Strong adoption supported by regulatory rigor, public healthcare digitization, and emphasis on data governance compliance.

The Digital Health Enforcement & Compliance Technologies market is moderately fragmented, with over 90 active vendors globally offering compliance management, audit automation, and governance platforms. The top five companies collectively account for approximately 48% of the total market share, indicating a competitive but consolidating environment. Large technology firms dominate enterprise deployments through integrated cloud and analytics ecosystems, while mid-sized vendors focus on niche regulatory or regional requirements. Strategic initiatives include partnerships with EHR providers, expansion of AI-driven risk scoring engines, and modular compliance platform launches. Between 2023 and 2024, more than 30 strategic alliances were formed to enhance interoperability and regulatory coverage. Innovation is centered on continuous monitoring, real-time enforcement, and explainable AI compliance logic. Competitive differentiation increasingly depends on scalability, regulatory breadth, and integration depth rather than pricing alone.

SAP

Salesforce

ServiceNow

Palantir Technologies

FICO

NICE Actimize

Wolters Kluwer

Thomson Reuters

Experian

DXC Technology

Tata Consultancy Services

Technological evolution in this market centers on automation, intelligence, and interoperability. AI-driven compliance analytics now support anomaly detection across more than 50 million healthcare records per day globally. Machine learning models are increasingly used to predict non-compliance risks, reducing manual audit dependency by nearly 45%. Blockchain technologies are deployed to secure audit trails, with immutable logging improving data integrity by over 35%. Cloud-native architectures dominate new deployments, accounting for approximately 66% of implementations due to scalability and centralized governance benefits. Identity and access management technologies integrate biometric and behavioral authentication, reducing unauthorized access incidents by 29%. Interoperability standards enable cross-platform compliance enforcement across EHRs, telehealth platforms, and payer systems. Edge compliance technologies are emerging to support real-time monitoring in remote care environments. These advancements collectively transform compliance from reactive validation into proactive enforcement.

In May 2024, Microsoft expanded healthcare compliance controls within its cloud platform, introducing automated policy enforcement and enhanced audit logging for healthcare tenants supporting millions of patient records. Source: www.microsoft.com

In February 2024, SAP enhanced its healthcare governance suite with integrated regulatory reporting automation, enabling faster compliance documentation across European healthcare providers. Source: www.sap.com

In October 2023, IBM launched advanced AI-based compliance analytics designed to detect regulatory violations across complex healthcare data environments in real time. Source: www.ibm.com

In August 2023, Oracle upgraded its healthcare data governance capabilities, adding enhanced consent management and cross-border data compliance controls. Source: www.oracle.com

The Digital Health Enforcement & Compliance Technologies Market Report provides comprehensive coverage of technologies, applications, and end-user adoption across global healthcare ecosystems. The scope includes compliance management platforms, AI-driven risk analytics, audit automation tools, identity and access governance, and data privacy enforcement technologies. The report evaluates applications across healthcare providers, life sciences companies, insurers, digital health startups, and government health agencies. Geographic coverage spans North America, Europe, Asia Pacific, South America, and Middle East & Africa, analyzing regional regulatory environments and adoption patterns. The report examines technology deployment models including cloud-based, on-premise, and hybrid systems, as well as emerging architectures such as blockchain-backed audit trails and predictive compliance engines. It also addresses niche segments such as telehealth governance, digital therapeutics compliance, and cross-border data enforcement. By focusing on market structure, technology evolution, and competitive positioning, the report supports strategic planning, investment assessment, and market entry decisions for industry stakeholders.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 3,107.3 Million |

|

Market Revenue in 2032 |

USD 8,144.3 Million |

|

CAGR (2025 - 2032) |

12.8% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

IBM, Oracle, Microsoft, SAP, Salesforce, ServiceNow, Palantir Technologies, FICO, NICE Actimize, Wolters Kluwer, Thomson Reuters, Experian, DXC Technology, Tata Consultancy Services |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |