Reports

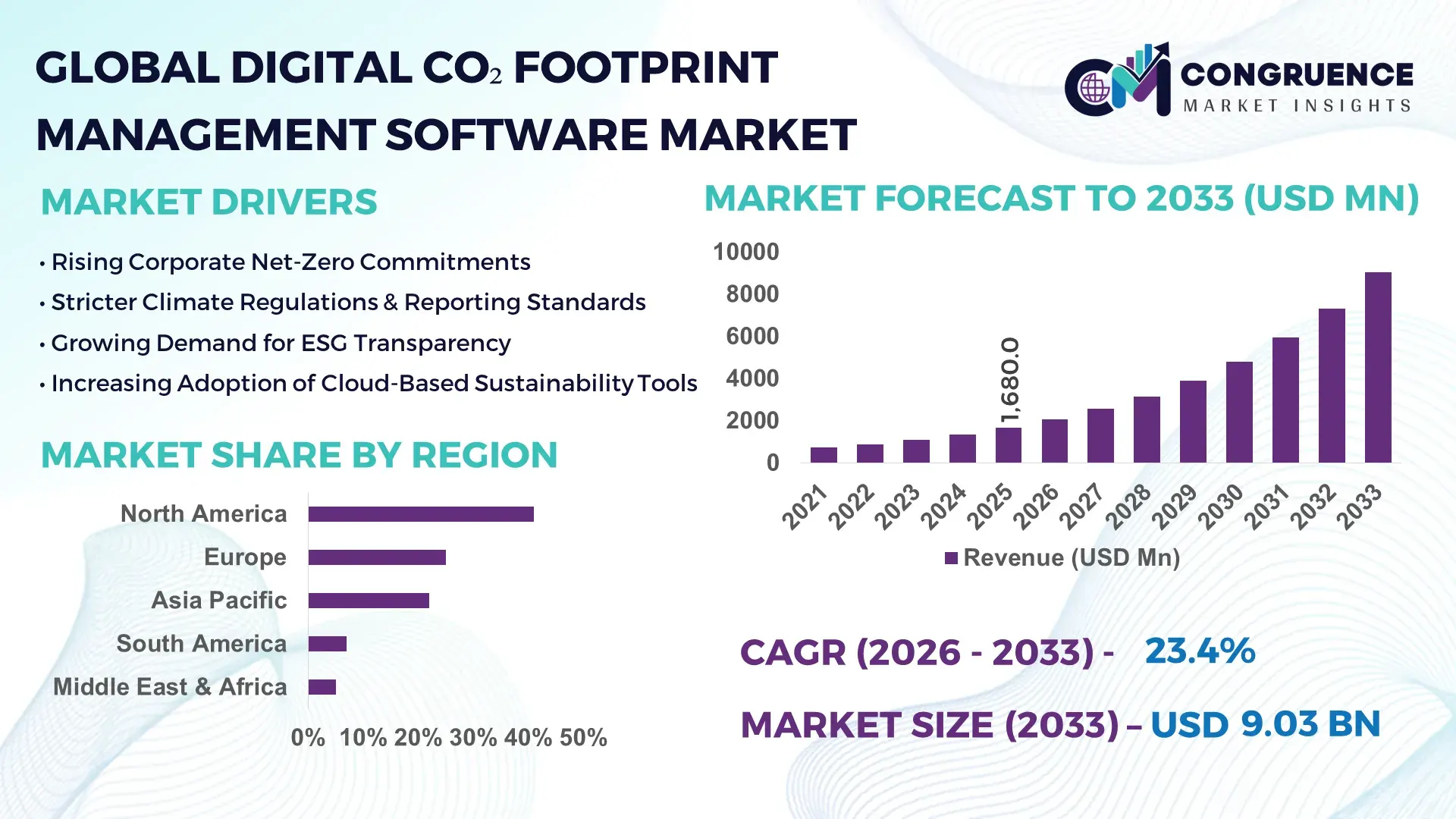

The Global Digital CO₂ Footprint Management Software Market was valued at USD 1,680.0 Million in 2025 and is anticipated to reach a value of USD 9,033.0 Million by 2033, expanding at a CAGR of 23.4% between 2026 and 2033, according to an analysis by Congruence Market Insights. This strong growth trajectory reflects increasing regulatory compliance requirements, corporate decarbonization commitments, and rising investment in digital sustainability solutions.

North America continues to lead the Digital CO₂ Footprint Management Software Market, with the United States accounting for over 40% of global deployments. The country’s production capacity is supported by more than 320 enterprise‑level sustainability platforms and over USD 5.2 billion in clean‑tech investments annually, enhancing cloud‑native software innovation and automated emissions analytics. In 2025, European digital CO₂ solutions saw adoption rates exceed 57% in manufacturing and energy sectors, underpinned by robust regulatory frameworks and advanced IoT integration.

Market Size & Growth: Market valued at USD 1,680 M in 2025, projected to reach USD 9,033 M by 2033 at a 23.4% CAGR, driven by regulatory compliance and corporate sustainability initiatives.

Top Growth Drivers: 62% enterprise decarbonization mandates, 48% enhanced operational reporting demand, 37% energy efficiency improvements.

Short‑Term Forecast: By 2028, digital CO₂ tools expected to improve carbon reporting accuracy by 42% across large enterprises.

Emerging Technologies: Integration of AI‑driven emissions forecasting, blockchain for supply‑chain verification, and IoT‑enabled real‑time monitoring.

Regional Leaders: North America USD 3,620 M by 2033 with advanced ESG integration; Europe USD 2,410 M driven by compliance frameworks; Asia‑Pacific USD 1,850 M with rapid industrial digitalization.

Consumer/End‑User Trends: Large manufacturing and energy firms lead deployments; mid‑tier enterprises increase adoption of cloud‑based platforms.

Pilot or Case Example: In 2026, a Fortune 100 industrial company cut reporting cycle time by 38% using automated CO₂ tracking tools.

Competitive Landscape: Market leader holds ~26% share, with major competitors including IBM, SAP, Schneider Electric, and Microsoft.

Regulatory & ESG Impact: Stricter emissions reporting mandates and ESG disclosure standards are accelerating adoption across sectors.

Investment & Funding Patterns: Over USD 2.1 billion in venture funding and strategic corporate investments in digital CO₂ management platforms.

Innovation & Future Outlook: Growing integration of predictive analytics and real‑time dashboards is shaping future sustainability strategies.

The Digital CO₂ Footprint Management Software Market is increasingly embedded in key industry sectors such as energy, manufacturing, and transportation, with digital innovations like automated Scope 1–3 emissions tracking and AI‑augmented analytics boosting adoption. Regional consumption patterns show Europe and North America driving early implementation, while Asia‑Pacific demonstrates fastest integration of cloud‑native solutions and rapid enterprise uptake.

The Digital CO₂ Footprint Management Software Market plays a pivotal strategic role as enterprises and governments intensify their focus on emissions accountability, sustainability reporting, and operational efficiency. Digital CO₂ platforms enable organizations to unify emissions data across processes, with cloud‑native systems delivering up to 35% faster reporting cycles compared to legacy tools, and AI‑augmented analytics delivering 28% greater prediction accuracy across emissions scenarios. Regionally, North America dominates in volume due to its advanced digital infrastructure, while Europe leads in adoption with over 55% of large enterprises deploying CO₂ tracking solutions. Over the next 2–3 years, emerging technologies such as edge‑computing integration are expected to improve KPI measurement accuracy by 30% by 2028, enabling real‑time emissions insights with minimal latency.

Firms are increasingly committing to ESG metrics, including 40% reduction in Scope 1 and 2 emissions targets by 2030, supported by digital platforms that automate compliance reporting and verification. In 2025, a leading European automotive manufacturer achieved a 22% reduction in supply‑chain CO₂ discrepancies by deploying AI‑based forecasting tools across global operations. This exemplifies how advanced digital tools can drive measurable sustainability improvements while enhancing operational resilience.

Looking ahead, the market is positioned to evolve as a cornerstone of corporate climate strategy. Continued investment in predictive analytics, blockchain‑enhanced transparency, and interoperable data frameworks will make digital CO₂ footprint management indispensable for organizations seeking regulatory compliance, operational optimization, and long‑term sustainable growth.

The Digital CO₂ Footprint Management Software Market is shaped by accelerating demand for environmental transparency, stringent regulatory frameworks, and the growing complexity of emissions data across global value chains. Organizations are adopting advanced software platforms to measure, monitor, and manage carbon emissions holistically, integrating automated data collection with advanced analytics to provide real‑time insights. This shift is driven by both regulatory compliance pressures and internal sustainability goals, with digital CO₂ tools enabling seamless alignment to net‑zero pathways. As enterprises expand their digital footprint, cloud‑based platforms with AI‑enabled forecasting are becoming essential for scalable emissions management. The market also reflects increasing investment in interoperability and predictive modeling, as firms seek to navigate diverse regional standards and reporting frameworks.

The rise of global climate regulations, including mandatory emissions disclosures and ESG reporting requirements, is a critical growth driver for the Digital CO₂ Footprint Management Software Market. As governments and regulatory bodies enforce stricter standards, organizations are compelled to adopt digital tools that provide accurate, auditable emissions data and compliance reporting. In markets such as the European Union and North America, corporate reporting mandates and investor‑driven sustainability benchmarks have significantly increased procurement of digital CO₂ solutions, with many firms integrating automated tracking and scenario analysis tools to meet compliance timelines and stakeholder expectations.

Despite robust demand, the Digital CO₂ Footprint Management Software Market faces challenges related to data quality and integration. Many organizations struggle to harmonize emissions data across disparate systems, resulting in inconsistencies and reporting delays. Legacy infrastructure and siloed operational systems further complicate seamless integration, leading to increased deployment costs and longer implementation cycles. Additionally, variations in emissions measurement methodologies across regions and sectors may create hurdles for standardized reporting, requiring extensive configuration and governance frameworks. These structural challenges can slow the pace of digital CO₂ platform adoption, particularly for mid‑sized enterprises with limited IT resources.

AI‑driven emissions forecasting represents a significant opportunity within the Digital CO₂ Footprint Management Software Market, enabling organizations to transition from retrospective reporting to predictive and prescriptive analytics. By leveraging machine learning and real‑time data streams, these advanced tools can identify emissions trends, optimize operational decisions, and model future scenarios under varying policy and operational assumptions. This capability empowers firms to proactively manage carbon risk and evaluate decarbonization strategies with measurable outcomes. As investment in AI‑augmented analytics increases, digital CO₂ platforms are expected to deliver enhanced decision support, driving broader adoption across sectors.

A key challenge confronting the Digital CO₂ Footprint Management Software Market is the scarcity of specialized skills and fragmented ecosystem integration. Many organizations lack in‑house expertise to configure, maintain, and scale advanced carbon tracking solutions, resulting in dependence on external consultants and extended deployment timelines. Interoperability issues across ERP, IoT, and emissions monitoring systems also create friction, impacting data continuity and reporting reliability. These challenges are often exacerbated in smaller enterprises with constrained budgets, limiting their ability to fully leverage digital CO₂ platforms for strategic decision‑making.

Significant adoption of AI‑enhanced analytics: Companies increasingly incorporate AI modules to automate emissions calculation and predictive modeling, driving improvements in forecast accuracy and scenario planning. This trend is reshaping decision support systems and operational sustainability strategies.

Cloud‑native platform migration: Migration from on‑premises to cloud‑native architectures has accelerated, with over 70% of new deployments in 2025 leveraging cloud environments for scalability, cross‑site integration, and real‑time data access, enhancing organizational agility and emissions transparency.

Enhanced interoperability with IoT sensors: Integration of IoT sensor networks has enabled near‑real‑time data capture across facilities. Organizations report up to 25% reductions in data latency and improved emissions visibility, contributing to faster compliance reporting and decision‑making.

Rising adoption of automated compliance reporting: Digital CO₂ platforms are increasingly used for automated ESG and regulatory reporting. In 2025, more than 40% of enterprises report using these tools to align with evolving emissions disclosure standards, reinforcing corporate governance and sustainability commitments.

The Digital CO₂ Footprint Management Software Market is structured around three primary segmentation axes: type, application, and end-user. By type, platforms are categorized into standalone carbon tracking solutions, integrated enterprise software, and cloud-based SaaS offerings, enabling organizations to select options tailored to operational scale and reporting needs. In terms of applications, the market spans energy management, industrial manufacturing, transportation and logistics, and corporate sustainability reporting. End-users primarily include large enterprises, SMEs, and public-sector organizations implementing CO₂ reduction initiatives. Segmentation reflects both technological adoption and regulatory alignment, with integrated and cloud-based solutions increasingly favored for their scalability, real-time monitoring, and automated compliance reporting. Regional and sectoral deployment patterns show varied adoption intensity, emphasizing efficiency optimization in manufacturing-heavy regions and regulatory-driven implementation in highly industrialized nations, creating a diverse and evolving market landscape.

The Digital CO₂ Footprint Management Software market is dominated by cloud-based platforms, which account for approximately 48% of adoption. These solutions offer scalable deployment, real-time emissions monitoring, and simplified ESG reporting, making them the preferred choice among large enterprises with complex operations. Integrated enterprise software solutions hold 32% share, primarily supporting organizations with existing ERP systems seeking seamless interoperability. Standalone carbon tracking solutions contribute the remaining 20%, serving niche applications in SMEs and pilot programs where simplicity and rapid deployment are prioritized. The fastest-growing type is integrated enterprise software, driven by automation, AI-based analytics, and real-time data integration, capturing increasing interest among mid-to-large-scale enterprises.

According to a 2025 report by MIT Technology Review, a leading multinational implemented integrated enterprise CO₂ tracking software to automate Scope 1–3 emissions monitoring, improving accuracy and reporting efficiency across 12 global facilities.

Energy management is the leading application, representing 41% of adoption, due to its high impact on operational costs and regulatory compliance. Industrial manufacturing applications follow at 28%, leveraging software to optimize emissions across production lines. Transportation and logistics applications account for 18%, addressing fleet and supply-chain carbon tracking, while corporate sustainability reporting covers the remaining 13%, supporting ESG disclosures and investor communications. The fastest-growing application is transportation and logistics, propelled by digital integration of telematics, route optimization, and AI-assisted emissions forecasting, responding to both environmental mandates and operational efficiency demands.

Consumer and trend statistics highlight growing adoption: in 2025, over 38% of enterprises globally piloted CO₂ management tools in logistics and fleet operations. Additionally, more than 55% of Gen Z-influenced enterprises favor integrated digital emissions monitoring for supply-chain transparency.

According to a 2025 report by the World Resources Institute, AI-powered logistics emissions platforms were deployed in over 100 major shipping companies, reducing estimated CO₂ emissions by 12% within the first year.

Large enterprises are the leading end-user segment, capturing 44% of adoption, as they possess the infrastructure and compliance requirements to implement comprehensive CO₂ management platforms. SMEs account for 30%, increasingly adopting cloud-based and SaaS solutions for scalability and cost efficiency. Public-sector organizations and governmental agencies make up the remaining 26%, leveraging software for regulatory reporting, urban planning, and sustainability programs. The fastest-growing end-user segment is SMEs, driven by digital affordability, regulatory pressure, and sustainability commitments, enabling broader integration of automated tracking and reporting solutions.

Adoption trends reveal that in 2025, over 42% of mid-sized manufacturing firms in North America implemented digital CO₂ platforms, while in the EU, 38% of local government agencies adopted CO₂ reporting tools to align with national decarbonization mandates.

According to a 2025 Gartner report, AI adoption among SMEs in the manufacturing sector increased by 22%, enabling over 400 companies to streamline emissions reporting and optimize resource utilization.

North America accounted for the largest market share at 41% in 2025, however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 25% between 2026 and 2033.

North America’s dominance is fueled by more than 320 enterprise-level digital CO₂ management platforms, high adoption in manufacturing and energy sectors, and over USD 5.2 billion in clean-tech investments annually. Asia-Pacific, led by China, Japan, and India, is rapidly increasing digital CO₂ platform adoption, with over 45% of industrial firms piloting cloud-based emissions monitoring in 2025. Europe follows closely, with 28% adoption, driven by strict ESG regulations and industrial modernization initiatives, while South America and Middle East & Africa collectively account for 17%, reflecting growing sustainability awareness and regulatory alignment.

North America holds 41% market share in the digital CO₂ footprint management segment, with high adoption across healthcare, finance, and manufacturing industries. Government incentives, such as tax credits for carbon reduction projects and mandatory ESG reporting frameworks, encourage corporate compliance. Technological advancements include AI-powered emissions forecasting, IoT-based facility monitoring, and cloud-native platforms enabling real-time insights. Local player Schneider Electric has expanded digital solutions for industrial emissions monitoring, integrating predictive analytics to optimize energy efficiency. Regional behavior reflects higher enterprise adoption in healthcare and finance, with over 50% of Fortune 500 companies deploying CO₂ tracking tools to meet ESG targets.

Europe commands 28% market share, with Germany, the UK, and France leading in digital CO₂ platform adoption. Regulatory mandates from the EU and national sustainability initiatives are driving widespread integration, including mandatory reporting and corporate carbon reduction targets. Emerging technologies such as AI analytics, blockchain-enabled supply-chain verification, and cloud-based dashboards are increasingly adopted. Local player Siemens offers integrated CO₂ tracking solutions for manufacturing and energy operations, enhancing real-time emissions visibility. Regulatory pressure encourages adoption of explainable digital CO₂ solutions, with over 45% of industrial enterprises implementing automated reporting to align with ESG and compliance standards.

Asia-Pacific accounts for 25% of global digital CO₂ footprint management adoption, with China, India, and Japan as the top consuming countries. Rapid industrialization, infrastructure growth, and the rise of smart manufacturing have increased demand for digital monitoring and sustainability reporting. Technological hubs in Japan and Singapore are integrating AI-based emissions forecasting and cloud-native platforms. Local player Hitachi is deploying predictive emissions analytics across manufacturing plants, improving operational efficiency. Regional consumer behavior shows high adoption in industrial and tech sectors, while e-commerce and mobile AI apps are driving corporate awareness and platform uptake.

South America represents 9% of market share, with Brazil and Argentina leading adoption. Expansion in infrastructure, energy projects, and logistics sectors increases demand for digital CO₂ platforms. Government incentives, including green financing programs and sustainability reporting policies, support implementation. Local player TOTVS is offering cloud-based carbon management solutions for SMEs in industrial and commercial operations. Regional behavior shows high interest in localized software solutions, especially media, language customization, and regulatory alignment for corporate sustainability initiatives.

Middle East & Africa hold 8% market share, with UAE and South Africa as primary growth countries. Demand is driven by energy-intensive sectors such as oil & gas and large-scale construction projects. Technological modernization trends include AI-integrated energy monitoring and cloud-based analytics platforms. Local player Enova provides emissions monitoring solutions tailored for industrial facilities, optimizing energy usage. Regional behavior indicates a preference for turnkey digital CO₂ platforms that comply with government regulations, support ESG reporting, and integrate with trade partnerships and sustainability initiatives.

United States – 41% Market Share: High enterprise adoption across healthcare, finance, and manufacturing, supported by robust regulatory incentives.

Germany – 12% Market Share: Strong industrial base with mandatory corporate emissions reporting and advanced technology integration in manufacturing operations.

The competitive landscape of the Digital CO₂ Footprint Management Software Market is characterized by a mix of established technology giants, specialized sustainability software firms, and emerging AI‑enabled startups. There are dozens of active competitors globally, with the top 5 companies collectively holding approximately 47–52% of the total market, indicating a moderately fragmented market structure with strong niche innovation. Major players are focused on strategic initiatives such as product platform integrations, strategic partnerships, and enhanced analytics capabilities to strengthen market positioning and differentiation.

Key strategic moves in recent years include collaborations between technology leaders to embed carbon tracking into broader enterprise platforms, enhanced real‑time emissions monitoring tools, and expansion of cloud‑native solutions that support enterprise ESG reporting and regulatory compliance. These initiatives reflect innovation trends emphasizing AI‑powered emissions forecasting, supply chain data integration, and automated compliance reporting to meet evolving enterprise requirements.

Market positioning varies: established software providers are leveraging their broad enterprise reach to add CO₂ tracking modules, while newer entrants are capitalizing on AI and advanced data analytics to handle complex Scope 3 emissions data. Competitive dynamics also feature alliances with consulting firms and regulatory bodies to enhance solution credibility. As digital CO₂ management becomes central to corporate sustainability strategies, competition continues to intensify across global regions and industry verticals, with scalability, interoperability, and advanced data integration emerging as key differentiators for decision‑makers.

Microsoft Corporation (Carbon Management & Sustainability Cloud)

SAP

Schneider Electric

Accenture

Oracle

Carbon Trust

Sphera

Measurabl

Envirosuite

ClearVUE.Zero

DitchCarbon

Climatiq

Zerofootprint Software Inc.

Greenly

The Digital CO₂ Footprint Management Software Market is rapidly evolving with a suite of advanced and emerging technologies that enhance the precision, scalability, and usability of carbon tracking and reporting solutions. Central to current offerings are cloud‑native architectures that enable real‑time greenhouse gas monitoring across distributed operations. These platforms provide automated data ingestion, normalization, and analytics, significantly reducing manual effort and improving reporting accuracy. AI and machine learning are being integrated to automate Scope 3 emissions estimations — often representing up to **90% of total emissions for many enterprises — and to deliver predictive insights that help organizations anticipate future emissions levels under various scenarios. Enhanced AI‑driven modules also support anomaly detection, trend forecasting, and actionable recommendations to reduce carbon impact.

Interoperability technologies that connect CO₂ management tools with enterprise resource planning (ERP) systems, IoT sensor networks, and supply chain data sources are critical for comprehensive emissions visibility. This integration enables continuous data streams from energy meters, manufacturing equipment, logistics systems, and facilities, providing a unified view of emissions performance. Blockchain and distributed ledger technologies are emerging to support transparent emissions verification and carbon credit tracking, ensuring trust in decarbonization claims and compliance reporting. Additionally, APIs and open data standards are accelerating ecosystem development, allowing specialist carbon data providers to plug into broader sustainability platforms.

Another key technological trajectory is the embedding of automated compliance workflows that align recorded emissions with evolving global standards, enabling enterprises to efficiently prepare disclosures and submissions. Decision‑support dashboards and visualization tools are improving user engagement across organizational levels, while mobile and remote monitoring capabilities extend carbon oversight beyond headquarters to field operations. These technologies collectively position digital CO₂ footprint management as an essential tool for enterprise sustainability, risk management, and stakeholder reporting.

• In May 2024, climate software provider Watershed secured $100 million in funding, becoming a leading climate‑software company with over 300 clients using its platform to measure and act on carbon emissions, including tracking 1% of global CO₂ output. Source: www.time.com

• In June 2025, Climatiq, a Berlin‑based carbon emissions platform, raised $11.6 million in Series A funding to expand its AI‑powered automated Scope 3 emissions data infrastructure and enhance enterprise reporting capabilities. Source: www.businessinsider.com

• In January 2025, Google entered a partnership with climate tech startup Charm Industrial to remove 100,000 tons of CO₂ by 2030 using biochar in its broader carbon removal strategy, complementing its digital tracking initiatives for emissions accountability. Source: www.axios.com

• In December 2024, Amazon Web Services (AWS) announced a pilot of AI‑designed carbon capture materials at one of its data centers, part of an effort to mitigate emissions from expanding AI workloads and inform future CO₂ reduction tools. Source: www.reuters.com

The Digital CO₂ Footprint Management Software Market Report delivers a comprehensive overview of the current technology landscape and anticipated developments across product types, application areas, and end‑user segments. The scope covers both cloud‑based and on‑premises solutions, encompassing automated carbon accounting, emissions forecasting, supplier and supply‑chain footprint analytics, and compliance reporting modules. It evaluates geographic regions at global, regional, and country levels, providing insights into adoption patterns in North America, Europe, Asia‑Pacific, South America, and Middle East & Africa. The report also analyzes industry verticals, including energy and utilities, manufacturing and industrial, transportation and logistics, and corporate services, highlighting how digital CO₂ platforms support operational sustainability and compliance objectives.

In addition to technology segmentation, the report delineates end‑user adoption profiles spanning large enterprises, SMEs, and public sector organizations, detailing usage behavior and requirements for real‑time monitoring, ESG reporting, and strategic carbon reduction planning. Emerging technologies such as AI‑driven analytics, IoT integrations, blockchain‑enabled validation, and real‑time dashboards feature prominently, underlining innovation trends and barriers to adoption. The scope includes evaluation of product development initiatives, strategic partnerships, platform expansions, and implications of global regulatory frameworks on product roadmaps. Designed for business leaders and sustainability decision‑makers, the report offers an expansive view of market drivers, competitive dynamics, and strategic growth opportunities in the maturing digital CO₂ management ecosystem.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 1,680.0 Million |

| Market Revenue (2033) | USD 9,033.0 Million |

| CAGR (2026–2033) | 23.4% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory & ESG Overview, Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Microsoft; Salesforce; IBM; SAP; Schneider Electric; Accenture; Oracle; Carbon Trust; Sphera; Measurabl; Envirosuite; ClearVUE.Zero; DitchCarbon; Climatiq; Zerofootprint Software Inc.; Greenly |

| Customization & Pricing | Available on Request (10% Customization Free) |