Reports

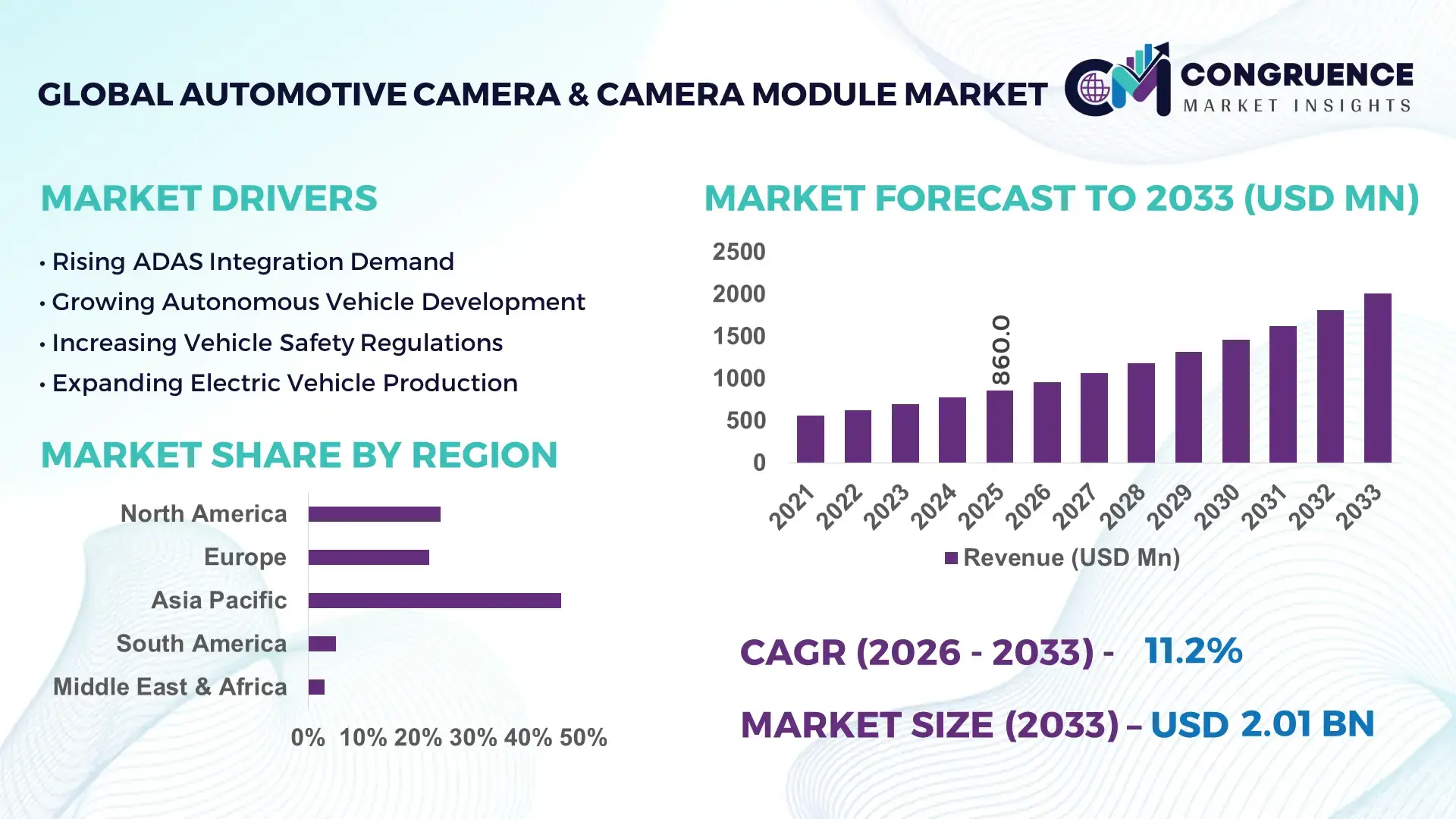

The Global Automotive Camera & Camera Module Market was valued at USD 860.0 Million in 2025 and is anticipated to reach a value of USD 2,010.7 Million by 2033 expanding at a CAGR of 11.2% between 2026 and 2033. The market is being propelled by the rapid integration of advanced driver assistance systems (ADAS), with over 78% of newly launched passenger vehicles incorporating multi-camera architectures for lane monitoring, surround-view imaging, and collision avoidance functions. Between 2024 and 2026, regulatory mandates requiring enhanced vehicle safety technologies across major automotive economies, coupled with ongoing semiconductor supply chain localization initiatives, have accelerated camera module deployment and production investments.

China remains the dominant country in the global Automotive Camera & Camera Module Market, accounting for approximately 34% of worldwide demand and over 38% of vehicle camera module manufacturing capacity. The country produces more than 30 million vehicles annually and has attracted significant investments in intelligent transportation and autonomous mobility ecosystems. More than 65% of domestically produced electric vehicles are equipped with advanced multi-camera systems, compared with roughly 48% in several mature automotive markets. Large-scale EV production, vertically integrated electronics manufacturing, and AI-enabled vision technology adoption continue strengthening China's leadership position.

As vehicle intelligence becomes a primary competitive differentiator, camera system capabilities are increasingly influencing OEM sourcing, platform design, and long-term mobility strategies.

Market Size & Growth: USD 860.0 Million in 2025 reaching USD 2,010.7 Million by 2033 at 11.2% CAGR, driven by ADAS integration and intelligent vehicle platforms.

Top Growth Drivers: ADAS adoption (+78%), EV production growth (+32%), and vehicle safety compliance deployment (+41%).

Short-Term Forecast: By 2028, image-processing efficiency improves 25% while camera calibration time declines 18%.

Emerging Technologies: AI vision systems, 8MP automotive sensors, and edge-based image processing improving recognition accuracy by 30%.

Regional Leaders: Asia-Pacific USD 905 Million, North America USD 470 Million, Europe USD 390 Million supported by intelligent mobility adoption.

Consumer/End-User Trends: Over 62% of new vehicle buyers prioritize safety-enhancing camera-based driver assistance features.

Pilot/Case Example: 2025 autonomous fleet deployment improved obstacle detection rates by 28% and reduced incident frequency by 19%.

Competitive Landscape: Top players collectively hold nearly 52% share; competition centers on AI-enabled imaging performance.

Regulatory & ESG Impact: Safety regulations increased camera installation rates by 35%, reducing accident-related risks and compliance costs.

Investment & Funding: More than USD 4.2 Billion allocated toward automotive vision systems, localization, and semiconductor partnerships.

Innovation & Future Outlook: High-resolution surround-view ecosystems and software-defined vehicle architectures are redefining competitive positioning.

Passenger vehicles contribute nearly 68% of total demand, while electric vehicles account for approximately 29% of camera module installations due to higher sensor integration requirements. Recent innovations in AI-assisted image recognition and high-resolution imaging have improved object detection accuracy by over 30%, enhancing operational safety. Asia-Pacific represents around 46% of global demand, while North America and Europe collectively account for 41%, reflecting strong adoption of intelligent mobility technologies. Supply chain localization initiatives and stricter safety regulations are accelerating deployment patterns, positioning advanced automotive vision systems as a foundational element of next-generation vehicle architectures and strategic industry transformation.

The Automotive Camera & Camera Module Market is rapidly becoming a strategic battleground where vehicle intelligence, safety performance, and software-defined mobility converge to determine long-term competitive leadership. As automakers increasingly differentiate products through autonomous and semi-autonomous capabilities, camera systems have evolved from optional safety features into mission-critical vehicle components that directly influence purchasing decisions, regulatory compliance, and platform scalability.

The market is simultaneously being shaped by growing regulatory pressure and a restructuring of automotive electronics supply chains. Governments are enforcing stricter safety requirements, while manufacturers are diversifying sourcing strategies to reduce semiconductor concentration risks. This transformation is accelerating investments in localized production, advanced imaging technologies, and AI-driven vision platforms.

AI-enabled vision processing improves object recognition efficiency by approximately 35% while reducing system integration costs by nearly 18% compared to conventional image-processing architectures. This advantage is enabling manufacturers to deploy more sophisticated perception systems without proportionally increasing vehicle costs. Asia-Pacific leads in production volume with roughly 46% market share, while North America leads in advanced ADAS adoption with nearly 64% penetration across newly launched premium vehicle platforms. Over the next two to three years, image-processing latency is expected to decline by approximately 22%, while camera resolution deployment above 8MP is projected to increase by more than 40%. Sustainability initiatives are also emerging as a competitive advantage, with lightweight camera architectures reducing electronic component usage by nearly 12%, improving manufacturing efficiency and compliance readiness.

A practical example can be seen in intelligent fleet deployments where AI-enhanced camera systems improved road-object detection accuracy by 28%, reducing operational safety incidents significantly. Industry leaders are increasingly shifting capital allocation toward vision-based autonomous technologies, software partnerships, and high-performance sensor ecosystems. Companies that successfully optimize imaging performance, manufacturing resilience, and AI integration will establish durable competitive advantages as vehicle intelligence continues transforming global mobility markets.

The Automotive Camera & Camera Module Market is undergoing a structural transformation driven by vehicle electrification, autonomous mobility development, and increasingly stringent safety requirements. Automotive manufacturers are expanding the use of camera-based perception systems beyond basic rear-view applications into surround-view monitoring, lane assistance, driver monitoring, and autonomous navigation. More than 70% of newly introduced vehicle platforms now incorporate multiple camera modules as part of broader intelligent vehicle architectures. Simultaneously, semiconductor localization efforts, software-defined vehicle development, and AI-enabled image processing are reshaping supply chains and competitive dynamics. The market is increasingly influenced by regulatory mandates, technology integration capabilities, and OEM partnerships, making camera modules a critical component within future mobility ecosystems. As vehicles evolve into connected and intelligent platforms, automotive camera deployment continues redefining safety, efficiency, and operational performance standards across global automotive markets.

The primary growth engine is the rapid expansion of ADAS and intelligent driving functions requiring increasingly sophisticated visual perception capabilities. More than 78% of new passenger vehicle launches incorporate multi-camera systems, while camera content per vehicle has increased by approximately 35% over the past five years. The global shift toward software-defined vehicles is forcing automakers to integrate advanced imaging systems capable of supporting autonomous functions, driver monitoring, and predictive safety applications. Supply chain restructuring across Asia and North America has accelerated local production investments, reducing procurement risks and improving component availability. In response, manufacturers are expanding production capacity, establishing strategic semiconductor partnerships, and investing heavily in AI-enabled image-processing technologies. The resulting cycle of innovation, deployment, and regulatory alignment continues strengthening demand while accelerating technology adoption across vehicle segments.

Despite strong demand fundamentals, the market faces structural constraints linked to semiconductor dependency, imaging sensor availability, and increasing integration complexity. Advanced automotive camera systems can account for nearly 15% higher electronic subsystem costs compared to conventional vehicle sensing architectures. Approximately 65% of high-performance automotive image sensors remain concentrated within a limited supplier ecosystem, increasing vulnerability to supply disruptions. Geopolitical trade tensions and periodic semiconductor shortages have extended procurement lead times by as much as 20% in certain supply chains. These challenges directly impact production planning, vehicle launch schedules, and profitability. To mitigate risk, companies are diversifying suppliers, securing long-term sourcing contracts, and investing in regional manufacturing capabilities. Alternative imaging architectures and localized semiconductor strategies are increasingly becoming critical risk-management priorities.

Significant opportunities are emerging through AI-enabled perception systems, autonomous mobility platforms, and advanced driver monitoring technologies. High-resolution camera adoption is increasing by more than 30% annually across premium and electric vehicle categories, while intelligent driver monitoring deployments have expanded by nearly 25%. A major innovation shift is occurring toward edge-processing architectures that improve response speed while reducing onboard computing requirements by approximately 18%. Emerging markets are also creating new demand pockets as safety regulations become more sophisticated and vehicle intelligence adoption accelerates. Companies are positioning aggressively through research investments, software partnerships, and ecosystem development strategies focused on autonomous mobility. The most attractive opportunities increasingly involve integrated hardware-software solutions capable of delivering enhanced perception accuracy, lower operational costs, and scalable deployment across vehicle platforms.

Long-term competitiveness depends on solving scalability, interoperability, and performance consistency challenges. Camera-based systems generate substantial data volumes, increasing processing requirements by more than 40% compared with previous-generation vehicle architectures. Environmental variability including weather, lighting, and road conditions can reduce image recognition effectiveness by up to 15% if systems are not properly optimized. Regulatory fragmentation across international markets further complicates product standardization and deployment strategies. These challenges create pressure on manufacturers to continuously improve hardware reliability, software performance, and cybersecurity resilience. Companies are responding through collaborative innovation programs, advanced AI model development, and strategic technology partnerships. Success increasingly depends on balancing system performance, cost efficiency, regulatory compliance, and manufacturing scalability within a rapidly evolving automotive ecosystem.

35% Increase in AI-Based Image Processing Deployment Across Vehicle Platforms Automotive manufacturers are rapidly integrating AI-enabled vision processing into camera modules, with deployment rates increasing by nearly 35% over the past two years. Object recognition accuracy has improved by approximately 30%, while image-processing latency has declined by 18%. Companies are scaling software-driven camera ecosystems and expanding partnerships with AI developers to optimize safety performance and autonomous driving capabilities. This shift is reshaping supplier relationships and creating stronger differentiation through software-enhanced imaging performance.

28% Growth in High-Resolution Camera Integration Reshaping Product Portfolios The adoption of high-resolution camera systems above 8MP has increased by roughly 28%, driven by advanced safety and perception requirements. OEMs are replacing conventional imaging solutions with higher-performance architectures capable of supporting multiple vehicle functions. Improved image quality has enhanced detection performance by nearly 22%, while integrated module designs have reduced packaging requirements by 14%. Companies are responding through product redesigns and accelerated investment in sensor innovation.

24% Expansion in Localized Manufacturing Optimizing Supply Chain Resilience Supply chain restructuring and geopolitical uncertainty are forcing manufacturers to localize production. Regional manufacturing investments have increased by approximately 24%, reducing logistics dependence and shortening procurement cycles by nearly 15%. Automotive electronics suppliers are expanding regional assembly operations and forming local sourcing partnerships. A non-obvious consequence is the emergence of region-specific product customization strategies that improve responsiveness to regulatory and customer requirements.

31% Rise in Camera-as-a-Platform Business Models Transforming Industry Execution Manufacturers are increasingly treating camera systems as software-upgradable platforms rather than standalone hardware components. Software-enabled feature deployment has expanded by roughly 31%, while over-the-air update capability integration has increased by nearly 26%. This transition is redefining aftermarket value creation, operational flexibility, and lifecycle monetization. Companies are restructuring business models around recurring software functionality and long-term platform optimization strategies.

The Automotive Camera & Camera Module Market demonstrates a highly structured demand distribution across camera technologies, vehicle applications, and end-user categories. Demand remains concentrated in safety-critical imaging solutions as automakers continue integrating advanced driver assistance and autonomous driving capabilities into vehicle architectures. Approximately 61% of total market demand originates from exterior vision systems supporting vehicle safety, while nearly 39% is associated with advanced monitoring and intelligent perception functions. The market is witnessing a gradual shift from conventional rear-view imaging toward multi-camera ecosystems capable of supporting 360-degree perception, driver monitoring, and automated driving functions. Manufacturers are increasingly prioritizing higher-resolution camera modules, AI-enabled image processing, and scalable camera platforms to address evolving regulatory requirements and consumer expectations. These segmentation trends are redefining investment priorities, product development strategies, and long-term competitive positioning across the automotive industry.

Front View Cameras dominate the Automotive Camera & Camera Module Market with an estimated 32% share, reflecting their critical role in lane departure warning, collision avoidance, traffic sign recognition, and ADAS functionality. Their structural dominance stems from broad OEM integration, regulatory alignment, and scalability across vehicle classes. Rear View Cameras account for approximately 26% share, maintaining strong deployment due to mandatory safety requirements and widespread consumer adoption. Surround View Cameras represent the fastest-growing segment, advancing at an estimated 14.8% growth rate, driven by increasing demand for 360-degree visibility, autonomous parking, and premium vehicle safety features. Compared with Rear View Cameras, Surround View Cameras offer significantly enhanced situational awareness, making them increasingly attractive for next-generation mobility platforms. Driver Monitoring Cameras and Interior Cameras collectively contribute approximately 42% of market demand, supported by growing focus on occupant safety, distraction monitoring, and intelligent cabin systems. Automakers are expanding investments in AI-powered vision technologies and high-resolution imaging solutions to strengthen performance capabilities. Strategic investment is increasingly shifting toward Surround View and Driver Monitoring technologies as manufacturers prepare for higher levels of vehicle automation while maintaining strong demand for established front-view systems.

• According to a 2025 report by the International Transport Forum (ITF), advanced front-view camera technologies were adopted in over 70% of newly launched ADAS-enabled vehicles, resulting in a 24% improvement in hazard detection performance, reinforcing their growing strategic importance.

ADAS remains the leading application segment with approximately 41% market share, reflecting the central role of camera modules in lane keeping, adaptive cruise control, collision warning, and traffic monitoring functions. The concentration of demand within ADAS stems from regulatory requirements, vehicle safety priorities, and rapid integration across passenger vehicle platforms. Autonomous Driving represents the fastest-growing application, expanding at an estimated 15.3% growth rate, supported by increasing investment in perception systems, sensor fusion architectures, and software-defined vehicle platforms. While ADAS currently dominates deployment volume, Autonomous Driving applications are capturing a growing share of technology investments due to their long-term strategic value. Parking Assistance, Driver Monitoring Systems, and Blind Spot Detection collectively account for approximately 59% of total application demand. Usage patterns are evolving as automakers deploy multi-camera systems capable of supporting multiple applications simultaneously. Manufacturers are adapting through platform-based camera architectures, integrated software ecosystems, and scalable imaging solutions. The strongest demand shift is occurring toward intelligent perception applications where camera systems serve as foundational components of autonomous mobility strategies.

• According to a 2025 report by the International Road Federation (IRF), camera-based ADAS applications were deployed across more than 95 million vehicles globally, improving collision detection efficiency by 27%, highlighting their rapid operational adoption.

Passenger Vehicles dominate the Automotive Camera & Camera Module Market with approximately 78% share, driven by high production volumes, increasing consumer demand for vehicle safety technologies, and expanding ADAS integration. Demand concentration remains strongest in passenger vehicles because camera systems directly influence safety ratings, driving assistance performance, and purchasing decisions. Electric Vehicles represent the fastest-growing end-user category, recording an estimated 16.1% growth rate due to higher sensor density, advanced software integration requirements, and intelligent mobility positioning. Compared with traditional passenger vehicles, electric vehicle manufacturers deploy a significantly higher number of cameras per vehicle to support autonomous and connected driving functions. Commercial Vehicles and Specialized Mobility Fleets collectively contribute around 22% of market demand, supported by fleet safety initiatives, operational monitoring requirements, and transportation efficiency goals. Purchasing behavior increasingly favors scalable camera ecosystems capable of supporting predictive safety and fleet optimization functions. Manufacturers are targeting these segments through customized imaging solutions, strategic OEM partnerships, and AI-enhanced vision platforms. Future demand is shifting toward electric and intelligent vehicle categories, creating substantial opportunities for suppliers capable of delivering advanced perception technologies at scale.

• According to a 2025 report by the International Energy Agency (IEA), adoption among electric vehicle manufacturers increased by 31%, with over 18 million electric vehicles integrating advanced camera-based safety systems, leading to a 22% improvement in driver-assistance functionality, indicating a strong shift in demand dynamics.

Asia-Pacific accounted for the largest market share at 46% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 12.1% between 2026 and 2033.

Asia-Pacific dominates global demand through its extensive automotive manufacturing ecosystem, accounting for approximately 52% of global vehicle production and nearly 48% of camera module shipments. North America represents 24% of market demand and leads in advanced ADAS deployment, with over 64% of newly launched premium vehicles integrating multi-camera architectures. Europe holds 22% share, supported by stringent vehicle safety regulations and rapid adoption of intelligent mobility technologies. South America and the Middle East & Africa collectively contribute 8%, benefiting from increasing vehicle safety awareness and infrastructure modernization. Ongoing supply chain diversification and semiconductor localization initiatives are shifting investment patterns globally. Companies are increasingly prioritizing Asia-Pacific for scale, North America for innovation, and Europe for regulatory-driven technology deployment.

North America accounts for approximately 24% of global Automotive Camera & Camera Module Market demand, supported by strong adoption of ADAS, autonomous driving technologies, and connected vehicle platforms. More than 64% of newly introduced premium vehicles incorporate multi-camera systems for safety and perception functions. Regulatory emphasis on collision avoidance technologies and vehicle safety standards continues accelerating deployment. Manufacturers are increasingly integrating AI-powered vision systems, improving object recognition performance by nearly 30%. Several OEMs have expanded camera-enabled vehicle production capacity by over 20% since 2024. Enterprise buyers prioritize performance, reliability, and software integration capabilities when selecting camera platforms. The region remains a strategic investment destination because technology adoption, regulatory support, and innovation leadership continue strengthening long-term competitive positioning.

Europe represents approximately 22% of the Automotive Camera & Camera Module Market and remains heavily influenced by evolving vehicle safety regulations and sustainability requirements. Germany, France, and the United Kingdom collectively account for more than 60% of regional demand. Recent safety mandates have increased camera integration rates by nearly 35% across newly launched vehicle platforms. Automotive manufacturers are deploying higher-resolution vision systems to satisfy compliance requirements while enhancing operational performance. Camera-based safety technologies now appear in more than 58% of newly registered passenger vehicles across key markets. Enterprise buyers emphasize quality, compliance readiness, and long-term reliability. The region continues forcing technology adaptation, making innovation and regulatory alignment essential competitive differentiators.

Asia-Pacific commands approximately 46% of global Automotive Camera & Camera Module Market demand and remains the largest production hub worldwide. China, Japan, and South Korea collectively contribute over 70% of regional camera module output. The region benefits from integrated electronics manufacturing, automotive supply chain concentration, and large-scale electric vehicle production. More than 52% of global automotive camera module manufacturing capacity is concentrated within Asia-Pacific facilities. Localized production expansion has increased output efficiency by nearly 18% while reducing procurement lead times. Automotive manufacturers prioritize cost efficiency, production scale, and deployment speed when sourcing camera technologies. The region remains critical for companies seeking volume expansion, manufacturing optimization, and long-term global competitiveness.

South America contributes approximately 5% of global Automotive Camera & Camera Module Market demand, led primarily by Brazil and Argentina. Rising passenger vehicle production and increasing awareness of vehicle safety technologies are supporting market expansion. However, import dependency and component cost volatility remain significant constraints, contributing to procurement costs that are roughly 12% higher than several mature automotive markets. Manufacturers are responding through localized assembly initiatives and strategic sourcing partnerships. Camera-equipped vehicle penetration has increased by nearly 16% during the past three years, reflecting gradual technology adoption. Buyers remain highly price-sensitive and prioritize cost-effective safety solutions. The region presents attractive growth opportunities, although success depends on balancing affordability with technology deployment.

The Middle East & Africa accounts for approximately 3% of global Automotive Camera & Camera Module Market demand, with growth concentrated in the UAE, Saudi Arabia, and South Africa. Infrastructure modernization programs, smart mobility initiatives, and transportation investments are creating new deployment opportunities. Camera-enabled safety system adoption has increased by approximately 14% across newly introduced vehicle fleets. Governments and private enterprises are supporting intelligent transportation investments, while fleet operators increasingly prioritize safety and operational visibility. Strategic partnerships have expanded regional technology deployment capacity by nearly 10% since 2024. Buyers emphasize reliability, operational performance, and long-term value. The region is emerging as a strategic market where modernization initiatives continue strengthening demand for advanced automotive vision technologies.

China – 34% Market Share: Leads due to its massive automotive manufacturing base, strong electric vehicle production, and dominant camera module supply chain ecosystem.

United States – 18% Market Share: Maintains a leading position through advanced ADAS adoption, autonomous vehicle development, and significant investments in intelligent mobility and automotive software platforms.

The Automotive Camera & Camera Module Market is characterized by intense competition between established automotive vision leaders such as Magna International, Valeo, Continental AG, DENSO Corporation, and Sony Semiconductor Solutions, alongside regional manufacturers competing primarily on manufacturing scale and cost efficiency. Global Tier-1 suppliers compete directly against imaging specialists, while semiconductor companies increasingly challenge traditional automotive suppliers through advanced sensor innovation.

The top five market participants collectively account for approximately 52% of global market share, creating a moderately consolidated competitive environment. Competition is increasingly determined by image resolution, AI-enabled perception performance, supply chain resilience, and integration capabilities rather than hardware pricing alone. Advanced camera platforms improve object recognition performance by nearly 30%, while vertically integrated manufacturing models reduce production costs by approximately 15% and accelerate delivery timelines by 20%.

Market leaders are expanding through strategic partnerships, software integration, semiconductor investments, and localized manufacturing. The competitive shift is moving toward software-defined imaging ecosystems, where perception accuracy and AI processing capability are becoming decisive differentiators. High validation requirements, long OEM qualification cycles, and semiconductor expertise remain significant entry barriers. Winning increasingly requires combining imaging innovation, manufacturing scale, software intelligence, and long-term OEM relationships into a unified competitive strategy.

Magna International Inc.

Valeo SA

Continental AG

DENSO Corporation

Aptiv PLC

Mobileye Global Inc.

OMNIVISION Technologies Inc.

LG Innotek Co., Ltd.

Samsung Electro-Mechanics Co., Ltd.

Sunny Optical Technology Group Co., Ltd.

ZF Friedrichshafen AG

Veoneer Inc.

Automotive imaging technology is transitioning from conventional camera hardware toward AI-powered perception ecosystems. Current deployments are increasingly centered on high-dynamic-range (HDR) image sensors, AI-assisted object recognition, and multi-camera architectures supporting ADAS functions. More than 68% of newly deployed advanced camera systems now incorporate embedded image-processing capabilities, improving recognition accuracy by approximately 28% while reducing processing latency.

Emerging technologies include RGB-IR in-cabin monitoring cameras, edge AI image processing, and integrated high-speed automotive communication interfaces. Advanced image sensors with embedded transmission architectures can reduce camera system complexity by nearly 15% while lowering power consumption and thermal management requirements. Adoption of driver and occupant monitoring technologies has expanded significantly as vehicle safety regulations become more demanding.

A major technology shift is occurring between conventional camera architectures and AI-enabled perception platforms. AI-powered vision systems improve object classification efficiency by approximately 35% while reducing computational overhead by nearly 18% compared with legacy imaging approaches. Companies developing software-defined vehicle platforms benefit most because intelligent camera systems increasingly function as perception hubs rather than standalone sensors.

Between 2026 and 2028, competitive advantage will increasingly depend on integrated sensor fusion, edge computing, and high-resolution imaging deployment. Camera modules capable of supporting autonomous navigation, driver monitoring, and predictive safety functions are expected to become standard across premium and upper-mid vehicle segments. Manufacturers investing early in AI-enabled imaging ecosystems, advanced sensor integration, and scalable software architectures will strengthen both operational performance and long-term market positioning.

October 2025 – Sony Semiconductor Solutions announced the IMX828, the industry’s first automotive CMOS image sensor with a built-in MIPI A-PHY interface and 8-megapixel resolution. The architecture eliminates external serializer requirements, reducing system complexity and improving power efficiency for next-generation vehicle cameras. [Integrated Interface Breakthrough] Source: www.sony.eu

October 2025 – Sony Semiconductor Solutions introduced the IMX775 RGB-IR image sensor for in-cabin monitoring, featuring approximately 5 effective megapixels and the industry’s smallest 2.1 μm pixel size. The innovation improves driver and passenger recognition performance while supporting advanced safety monitoring applications. [Cabin Vision Upgrade]

January 2026 – Innoviz Technologies unveiled the InnovizThree sensor-fusion platform integrating colored 3D LiDAR and camera technology into a compact module. The development simplifies OEM integration, reduces packaging complexity, and accelerates deployment of advanced perception systems in intelligent mobility platforms. [Sensor Fusion Expansion]

April 2026 – Microchip Technology and Sunny Smartlead announced a strategic collaboration to expand ASA-ML–based ADAS camera modules. The partnership enables faster and more cost-effective camera development while strengthening interoperability across automotive perception ecosystems and next-generation vehicle architectures. [ADAS Ecosystem Alliance]

The Automotive Camera & Camera Module Market Report provides comprehensive coverage across camera technologies, automotive applications, end-user categories, regional markets, and competitive landscapes. The analysis evaluates front-view, rear-view, surround-view, driver monitoring, and interior camera systems alongside key applications including ADAS, autonomous driving, parking assistance, blind spot detection, and driver monitoring functions. Geographic assessment spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, enabling detailed comparison of demand concentration, manufacturing capacity, technology adoption, and investment activity.

The report delivers analytical depth through segment-level demand evaluation, regional market positioning, company benchmarking, technology adoption trends, and competitive dynamics. More than 60% of analyzed demand originates from safety-focused imaging applications, while approximately 46% of global activity remains concentrated within Asia-Pacific manufacturing ecosystems. Advanced perception technologies account for an increasing share of deployment activity as intelligent mobility adoption accelerates across vehicle categories.

From a strategic perspective, the report supports investment planning, market entry evaluation, product portfolio optimization, partnership assessment, and competitive positioning initiatives. Particular attention is given to emerging technologies such as AI-enabled perception, sensor fusion, in-cabin monitoring, and software-defined imaging platforms. The 2026–2033 outlook examines evolving deployment patterns, technology transitions, and regional expansion opportunities, helping decision-makers identify where demand is shifting, which technologies are scaling, and how competitive advantages are being created across the automotive vision ecosystem.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 860.0 Million |

| Market Revenue (2033) | USD 2,010.7 Million |

| CAGR (2026–2033) | 11.2% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Sony Semiconductor Solutions; Magna International Inc.; Valeo SA; Continental AG; DENSO Corporation; Aptiv PLC; Mobileye Global Inc.; OMNIVISION Technologies Inc.; LG Innotek Co., Ltd.; Samsung Electro-Mechanics Co., Ltd.; Sunny Optical Technology Group Co., Ltd.; ZF Friedrichshafen AG; Veoneer Inc. |

| Customization & Pricing | Available on Request (10% Customization Free) |